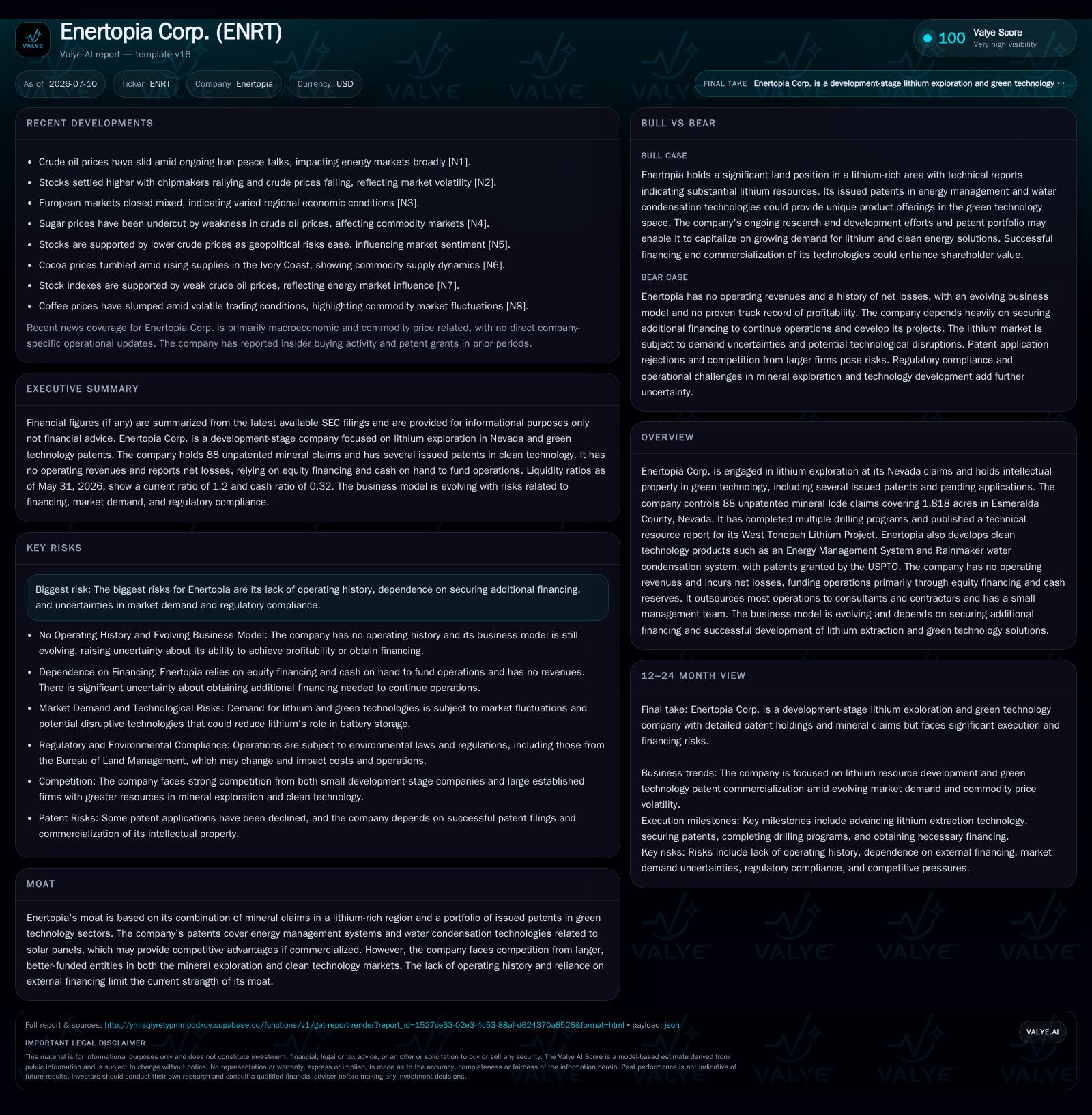

Enertopia Corp. Advances Lithium Exploration and Green Tech Patents Amid Capital Constraints

Enertopia's latest quarter highlights a strategic pivot with asset sales fueling liquidity but underscores reliance on equity financing to advance its dual lithium and clean technology business model.

Enertopia Corp. reported no operating revenues but recognized a substantial gain from selling its West Tonopah lithium claims, improving cash flows and working capital in the latest quarterly period. The company operates at the intersection of lithium mineral exploration—holding 1,818 acres in Nevada—and clean technology innovation with a portfolio of issued patents related to energy management and water condensation systems. Enertopia’s business remains capital intensive and early stage, relying on external equity financing and cost containment amid a net loss position. Key risks include continued dependence on raising funds, regulatory hurdles in mineral claims, and successful commercialization of patented green technologies.

Recent Operating Update

Enertopia Corp.'s latest quarterly filing dated July 10, 2026, reveals a significant shift in near-term operations primarily driven by the sale of its West Tonopah lithium property for $505,596, which resulted in positive net income despite an absence of operating revenues [S2], [S8]. This transaction materially improved the company's cash flows from investing activities and strengthened working capital from a deficit of $210,100 as of August 31, 2025 to a positive $57,115 as of May 31, 2026 [S2], [F1]. Importantly, the firm continues to report zero revenue streams from its core activities reflecting the early developmental stage of both its exploration efforts and technology commercialization. Operating expenditures declined notably through strategic cost containment reducing consulting fees roughly by half compared to prior periods and trimming research and development expenses significantly during the nine months ended May 31, 2026 [$33,807 vs. prior period] [S2], [S8]. The company maintains a lean internal team supplemented by outsourced contractors without plans for headcount expansion over the next year [S2]. While these developments provide some operational runway extension, the need for additional financing remains acute.

Business Model Analysis

Enertopia is positioned upstream in the lithium exploration value chain with mineral claims covering approximately 1,818 acres across Esmeralda County in Nevada under Bureau of Land Management (BLM) administration; these are unpatented mineral lode claims that require ongoing holding fees estimated at $17,600 annually plus county fees [S2]. The company completed multiple drilling programs culminating in a NI-43-101 technical report filed in November 2023 prior to divesting the West Tonopah project earlier this calendar year [S1], indicating a tactical reallocation or monetization strategy within its land position. Revenue generation is nascent since mining extraction has not commenced and licensing or sales of mineral assets drive proceeds.

Complementing mineral exploration is Enertopia’s intellectual property initiative focused on patented technologies within green energy domains. As of recent filings, the company holds three issued patents alongside one pending application concerning an Energy Management System (EMS) designed to optimize battery pack health and a water condensation invention branded "Rainmaker," which condenses atmospheric moisture using photovoltaic panel cooling techniques [S18]. Such patents represent potential future licensing or product development pathways but currently generate no direct revenue.

Given the absence of operational revenues, Enertopia relies largely on periodic equity financings alongside proceeds from strategic asset sales to fund ongoing exploration expenses—reported as $13,779 during the recent nine-month period—and research & development outlays [$33,807 over nine months] encompassing both patent prosecution and prototype development costs [S2], [S8]. Consulting fees remain significant but declining (down from ~$44k to ~$23k sequentially), indicative of externally sourced expertise balancing cost efficiency against capacity needs. The firm's monetization mechanics hinge on successfully converting geological assets into extractable reserves or generating royalties/license fees from patented technologies.

Industry Structure and Competitive Position

Operating within the lithium exploration sector situates Enertopia amid an intensely capital-intensive industry characterized by long lead times between initial claim staking and commercial production. Peer companies managing similar Nevada-based claims often boast larger acreage permits or advanced resource estimates with associated feasibility studies backed by institutional capital partners (e.g., Lithium Americas Corp., Ioneer Ltd.). By comparison, Enertopia’s acreage footprint—while substantive—is modest in scale without proven reserves reported post-sale of its premier project.

On the green tech front, patent-holding clean energy firms typically achieve differentiation via proprietary innovation enabling licensing revenue or joint ventures with established manufacturers. Enertopia’s EMS technology aligns with broader trends for battery lifecycle management critical for electric vehicles (EVs) fleet longevity but must surmount competitive challenges posed by incumbents possessing stronger R&D pipelines or integration channels (e.g., Johnson Controls International’s battery systems). Similarly, water harvesting via PV panel condensation intersects emerging sustainability markets yet demands validation through commercialization milestones.

The company’s reliance on outsourcing reflects standard practice among early-stage resource firms without mining operations while exposing it to risks associated with contractor availability and cost control—a factor compounded by limited internal personnel capacity [S2]. Regulatory compliance presents an ongoing hurdle for mineral claims held on public lands subject to environmental reviews overseen by federal agencies like BLM; failure to maintain permits or meet environmental standards could suspend exploration activities. Furthermore, absence of active mining means Enertopia cannot leverage commodity price-upside directly beyond speculative valuation linked to lithium market fundamentals.

Growth Drivers

Fundamental industry growth drivers center on explosive global demand for lithium fueled chiefly by electrification trends spanning EV manufacturing growth projections globally alongside energy storage infrastructure build-outs supporting renewable intermittency mitigation. These macro tailwinds increase speculative interest in upstream lithium deposits including those located in established mining jurisdictions such as Nevada known for regulatory stability relative to other global sources.

Concurrent innovation advances underpin potential commercial traction for Enertopia’s intellectual property portfolio focused on energy management systems designed to extend battery pack lifetimes—a critical factor influencing total cost-of-ownership economics for EVs which remains an adoption barrier globally. The Rainmaker system taps into growing water scarcity issues synergistic with solar panel deployment strategies promoting resource-efficient dual-use technologies.

Government incentives fostering clean energy development may bolster funding opportunities either via grants or cooperative agreements accelerating R&D progress or piloting initiatives. Should Enertopia secure strategic partnerships or joint ventures with mining operators or technology manufacturers leveraging its IP assets or claim holdings post-sale activity could expand commercial avenues beyond organic exploration appreciation.

Risks and Watchpoints

Core risks confronting Enertopia revolve around early-stage operational status underscored by lack of historical profitability coupled with steep capital demands inherent in mineral claim maintenance plus technology development cycles without assured commercialization timelines or returns [S1]. The company's going concern statement flags substantial doubt given cumulative operating losses exceeding half a million dollars per annum supported mainly by episodic equity fundraising—not sustainable cash flow generated internally.

Lithium market volatility driven by shifting supply-demand balances tied to macroeconomic cycles or disruptive battery chemistry breakthroughs pose uncertainties potentially undermining valuation assumptions tied to exploration assets. Regulatory risks encompass environmental compliance for mineral claims administered federally alongside jurisdictional fee obligations increasing cost burdens absent realized extraction revenues.

On technology commercialization fronts patent portfolios entail risks around enforceability limitations or competition introducing superior alternatives restricting licensing potential or requiring further extensive R&D investment diluting near-term financial resources. Management’s part-time status with possible conflict-of-interest scenarios intimates governance concerns affecting execution focus necessary during critical development inflection points.

Operationally dependence on external consultants raises execution risk especially if scaled deliverables underperform planned milestones forcing expensive remediation steps or scope reduction. Financing constraints remain paramount watchpoints given current cash positions ($340k current assets vs $283k liabilities as at May 31, 2026) avoid solvent distress only temporarily assisted by asset sales receipts rather than sustained cash flow generation capability [F1]

What To Watch Next

Key milestones include updates on any new financing rounds critical to funding property payments estimated at roughly $19k per year plus continued patent-related R&D targeted at $10k annually per management plans laid out previously [S1]. Tracking changes in acreage holdings post-West Tonopah sale will indicate whether portfolio repositioning occurs towards higher-value lithium claims or shifts focus exclusively onto green tech developments.

Progress toward licensing agreements involving EMS or Rainmaker technologies would signal proof points validating patent monetization strategies essential for long-term viability contrasting pure mineral speculation models. Any new drilling campaigns releasing updated resource volume estimates substantiated by NI-43-101 protocol would materially enhance project economics recognition if executed sustainably within available capital limits.

Additional indicators encompass changes in consulting fee trends implying adjustments in operational intensity alongside disclosures regarding regulatory permit renewals demonstrating compliance continuity. Finally monitoring engagement terms around joint ventures potentially diversifying operational risk while providing access to complementary technical capabilities may be decisive catalysts redefining business trajectories.

Financial Profile Discussion

As of May 31, 2026, Enertopia reported current assets totaling approximately $340,185 against current liabilities of about $283,070 producing a modest working capital surplus near $57,115 compared with a material deficit reported less than a year prior ($210K deficit at August-end 2025) reflecting principally proceeds from disposed mineral claim assets rather than recurring cash-generating operations [S2], [F1]. No debt is recorded on balance sheet consistent with limited financing activity aside from past equity raises inferred from operating expense coverage patterns.

Operating cash burn remains elevated with net cash used in operating activities approximating $265K over last nine months offset materially by investing cash inflow bolstered exclusively by asset disposition receipts [$505K inflows] rather than capital investment outflows underlining limited growth capex deployments currently prioritized towards sustaining R&D effort approvals rather than production ramp-up stages typical downstream mining companies [S13]

The firm notes no off-balance-sheet arrangements simplifying financial risk assessments while emphasizing GAAP compliance protocols ensuring transparency albeit constrained data availability due to small scale. The path forward hinges critically upon securing additional funding sources sufficient to cover annualized operating budgets estimated near $254K reflecting continued corporate overheads plus technology testing expenditures highlighted previously indicating fragile liquidity cushion vulnerable if asset sales revenues do not recur frequently enough to bridge gaps between R&D advancements leading eventually towards commercialization generating positive free cash flows sustainably meeting liabilities service requirements internally without detrimental dilution impact via fresh equity issuances dominating potential future funding routes [S1]

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data without making investment research views or endorsements regarding Enertopia Corp.

Financial position in context

Current assets of $340185 and current liabilities of $283070 imply a current ratio near 1.2x for 2026-05-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments