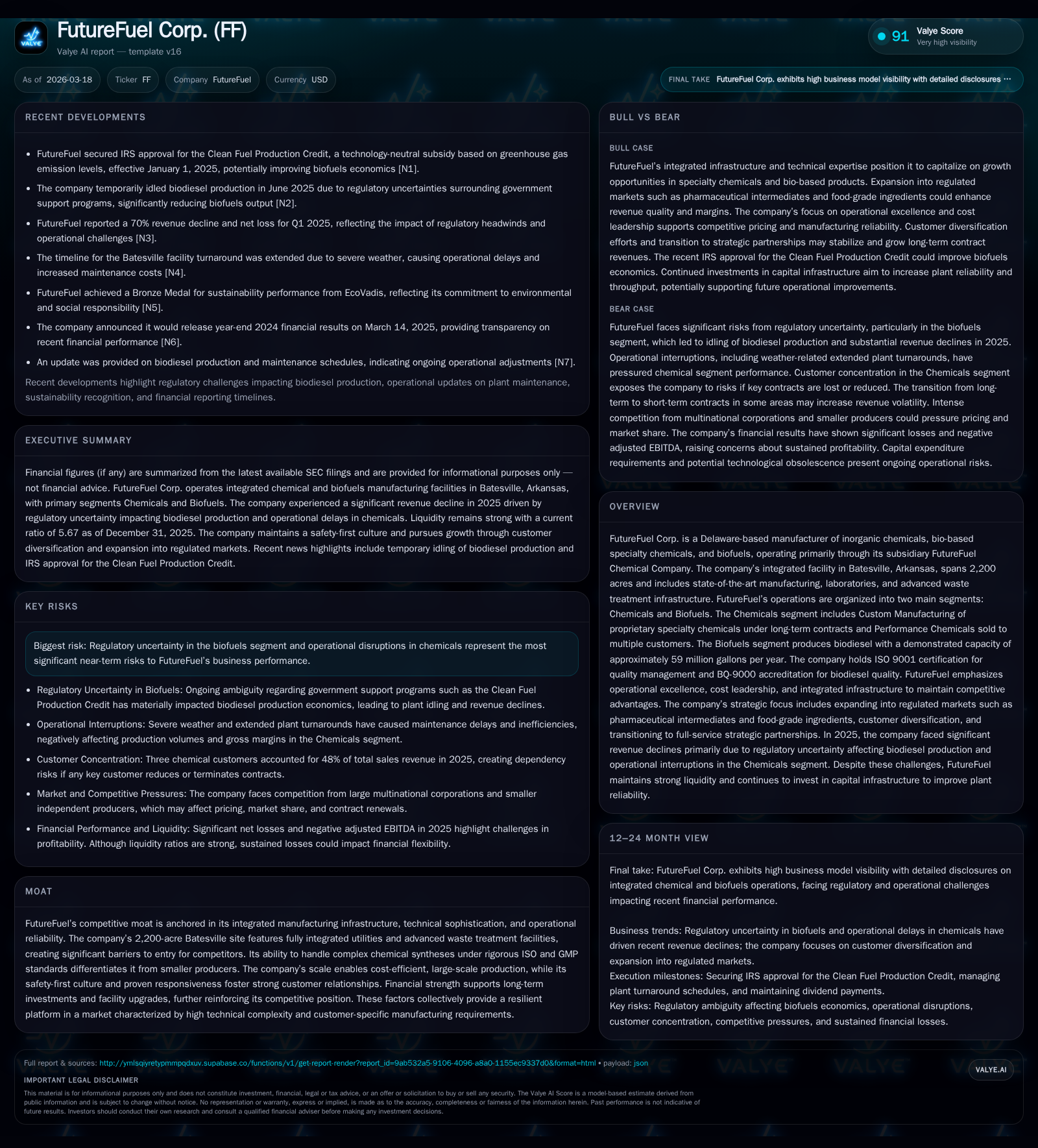

FutureFuel Corp.'s Financial Uplift and Renewable Energy Outlook

An exploration of FutureFuel’s recent financial setbacks and strategic positioning amidst evolving biofuel regulations and specialty chemical market demands.

FutureFuel Corp. experienced a sharp earnings decline in fiscal 2025, stemming primarily from operational disruptions in its Chemicals segment and regulatory uncertainty impacting its Biofuels segment. Despite these challenges, the company’s integrated 2,200-acre manufacturing complex and long-term customer relationships provide a defensible moat in specialty chemicals. The recent IRS approval of the Clean Fuel Production Credit (CFPC) offers potential incremental support, though timing and eligibility nuances temper near-term benefits. Capital allocation remains balanced with ongoing dividends and increased capital expenditures focused on facility modernization advancing operational resilience.

Evolution of FutureFuel’s Financial Performance and Operational Drivers

FutureFuel Corp. endured a marked decline in financial performance during fiscal year 2025 compared to prior years, with consolidated revenue contracting approximately 13% year-over-year as reported in prior years [F1]. Operating income deteriorated sharply, moving from a positive $6.4 million in 2024 to a loss nearing $53 million in 2025, reflecting operational challenges [F1]. Net income fell correspondingly from $15.5 million profit in 2024 to a net loss close to $49.4 million in the latest fiscal period [F1].

The downturn was driven by extended plant turnaround schedules delaying restart within the Chemicals segment alongside strategic idling of biodiesel production amid uncertain regulatory frameworks affecting feedstock economics and subsidy structures in the Biofuels segment [S1][S19]. Contract expirations further contributed to revenue decreases—especially related to long-term agreements within Custom Chemicals [S25].

Operating cash flow turned negative at about $28.7 million against positive inflows exceeding $24.8 million previously, resulting in negative free cash flow after capital expenditures which increased by nearly 18% to approximately $17.2 million invested mainly for capacity upgrades at the Batesville facility [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -49 | -29 | -53 | 17 | -418.6% |

| 2024 | 16 | 25 | 6 | 15 | -33.7% |

| 2023 | 23 | 21 | 27 | 6 | +56.6% |

| 2022 | 15 | 52 | 18 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | -46 | -31.9 |

| 2024 | 120 | 10 | 7.5 |

| 2023 | 11 | 15 | 7.5 |

| 2022 | 11 | 48 | 5.3 |

Source: SEC companyfacts cache [F1].

The Anatomy of the Chemicals Segment: Technical Complexity as a Moat

In 2025, FutureFuel's Chemicals segment accounted for approximately 62% of total revenue, integrating custom manufacturing with performance chemicals serving diverse markets such as agrochemicals, coatings, automotive polymers, and specialty solvents [S10][S15]. Custom products are typically produced under confidential long-term contracts for global brand owners supported by an integrated supply chain [S5][S11].

This segment leverages high technical barriers including proprietary synthesis routes maintained under ISO 9001 quality management systems with expanding GMP compliance aimed at pharmaceutical intermediate production [S6]. Pricing mechanisms vary from indexed raw material passthroughs for certain contracts to competitive market pricing without formal protections for others [S1][S15].

The expansive Batesville site spanning over 2,200 acres features fully integrated utilities and advanced waste treatment facilities providing meaningful barriers against new entrants while ensuring operational reliability [S6][S12]. Forward initiatives include vertical integration through backward integration into key raw materials securing internal supply chains and enabling external sales opportunities alongside process automation and lean manufacturing adoption to enhance margins amid global competition primarily from Asian multinational firms [S6][S12].

Biofuels Segment Challenges amid Regulatory Flux and Market Competition

The Biofuels segment represented about 38% of revenues but confronted headwinds due to fluctuating feedstock prices (vegetable oils, animal fats, food waste oils), volatile biodiesel pricing frameworks, and unsettled federal incentives transitioning from BTC to CFPC beginning January 2025 [S1][N1][S16]. The annual biodiesel production capacity stands near 59 million gallons; however, actual output was significantly curtailed due to mid-2025 plant idling responding to regulatory uncertainties limiting market visibility [S19].

Sales rely on monthly or short-term purchase orders rather than fixed long-term contracts with a broad customer base across transportation fuel refiners providing flexibility but exposing the company to spot market volatility including RINs and California LCFS credit price fluctuations [S1][S19]. Competitive pressures arise from renewable diesel producers favored by higher equivalency values (1.7 vs biodiesel's 1.5) along with growing electric vehicle adoption reducing demand for liquid combustion fuels incrementally [S1][N1][S17].

Logistically, rail/truck access combined with substantial storage enables opportunistic feedstock procurement during favorable pricing windows; however ongoing policy shifts at federal/state levels increase operational risk—delays in RFS2 renewable volume obligations add further uncertainty depressing market confidence [S1][S19].

Recent Federal Incentives: The Clean Fuel Production Credit Impact

Effective January 1, 2025, CFPC replaced BTC but remains subject to pending final IRS rulemaking expected mid-2026 causing interim ambiguity industry-wide [N1][S1]. CFPC credits scale based on GHG emissions reductions rewarding near net-zero emissions fuels potentially up to $1 per gallon; however, standard biodiesel producers like FutureFuel face practical limitations achieving maximum credits due to lifecycle carbon footprints inherent in their processes [S1][N1].

Additional qualifying criteria such as prevailing wage and registered apprenticeship requirements introduce complexity further delaying full benefit realization pending clarity from forthcoming regulations [N1][S1]. While CFPC establishes a more stable framework compared to retroactive BTC extensions that complicated planning historically, implementation will require operational agility.

Capital Allocation Priorities: Dividends, Capex, and Balance Sheet Strength

Despite profitability challenges reflected by net losses driving an approximate negative ROE of -31.9%, FutureFuel maintained shareholder returns through quarterly dividends totaling $0.24 per share during calendar year 2025 with initial dividend declarations continuing into early 2026 [F1][S14]. Dividend payments reduced cash reserves relative to prior years but were supported by robust liquidity with a current ratio above 5.6x at fiscal year-end ($100.5 million current assets vs $17.7 million current liabilities) indicating strong short-term solvency [F1][S4].

Capital expenditures rose roughly +17.6%, increasing from $14.7 million in FY24 to about $17.2 million invested primarily toward plant modernization aimed at enhancing throughput reliability while aligning production capabilities with evolving GMP standards supporting specialty chemical growth strategies outlined earlier [F1][S14]. Financial leverage remains managed under a revolving credit facility expiring around February 2030 with floating interest rates tied variably to SOFR plus modest spreads depending on leverage ratios offering funding flexibility if needed for future projects [S4].

Operational Risks and Market Headwinds Facing FutureFuel

Raw material sourcing vulnerabilities especially for inorganic chemical precursors sourced globally impact scheduling precision across segments combined with macroeconomic softness affecting sales volumes tied closely to cyclical end markets such as energy exploration or agriculture chemicals amplifying top-line pressures [S17][S18][S21].

Biofuel-related risks persist around government mandate renewals or expirations compounded by opposition from petroleum interests potentially leading to abrupt subsidy withdrawals which could invert gross margins if feedstock prices do not decrease proportionally creating unprofitable operating conditions [S17][S21][S29]. Renewable diesel competitors benefit from higher incentive equivalency factors embedded in programs posing sustained pricing challenges for biodiesel producers like FutureFuel [N1][S1].

Legal exposures remain limited largely to routine litigation typical within chemical manufacturing without material pending proceedings anticipated to affect financial outcomes significantly ensuring operational continuity absent extraordinary contingencies as disclosed recently [S17].

Future Milestones and Indicators to Watch in Biofuel Policy Progression

Critical forthcoming developments include IRS final rulemaking clarifying CFPC eligibility mid-2026 which will materially influence production economics alongside potential legislative actions extending or modifying BTC legacy mechanisms during transitional periods—these outcomes will decisively impact fuel blending economics influencing volume utilization rates dependent on renewed legislative certainty cycles [N1][S1].

Monitoring state-level Low Carbon Fuel Standard credit valuations alongside upcoming Renewable Fuel Standard volumetric quota adjustments is essential for assessing whether FutureFuel’s capacity deployment aligns efficiently or remains curtailed due primarily to policy uncertainties rather than asset constraints.

Parallel expansion efforts targeting pharmaceutical intermediates under GMP guidelines warrant attention given their potential insulated earnings contribution counterbalancing broader commodity volatility inherent in fuel markets reinforcing resilience afforded by FutureFuel’s infrastructure moat underpinning technical capability leadership.

Disclaimer: This analysis is based solely on available SEC filings and public disclosures through March 18, 2026; it is not investment advice or solicitation.

Comments