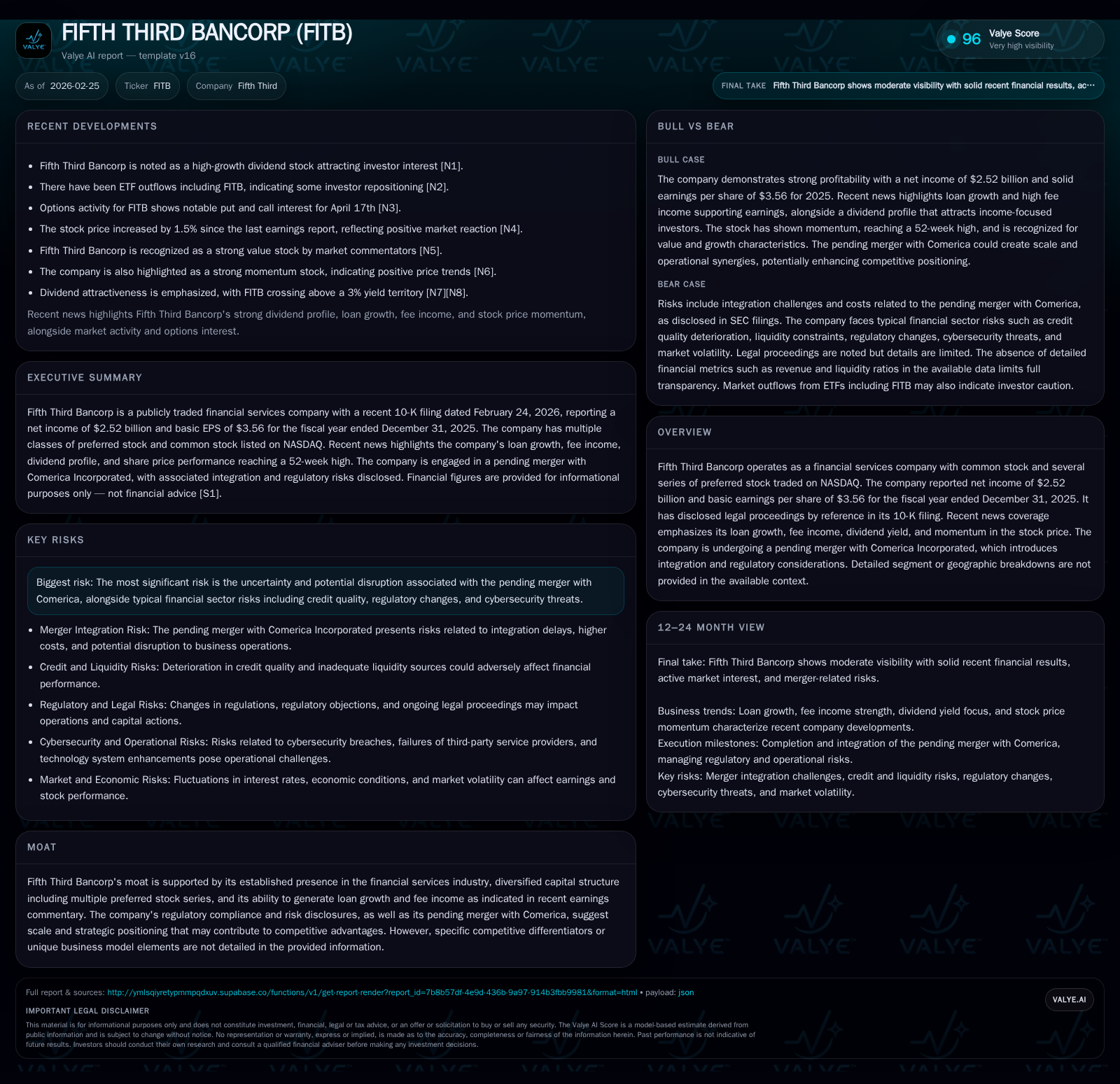

Fifth Third Bancorp's Steady Profit Surge and Merger Challenges

Fifth Third Bancorp reported robust net income growth in 2025 while preparing for a complex merger with Comerica, balancing growth and capital return amidst integration risks.

In the fiscal year 2025, Fifth Third Bancorp achieved a notable 9% year-over-year increase in net income, driven by sustained loan growth and elevated fee income. The company maintains strong operating cash flow and an active capital return policy, including dividends yielding above 3% and share buybacks, despite moderation in repurchase size. However, its pending merger with Comerica Incorporated introduces significant integration and regulatory challenges that could impact near-term operational stability. Market participants should monitor regulatory approvals, integration milestones, and shifts in investor sentiment reflected in ETF flows and option activity as key indicators of future trajectory.

Historical Earnings Performance and Key Drivers

Fifth Third Bancorp posted a solid net income gain of $2.52 billion for the fiscal year ended December 31, 2025, marking a healthy 9% increase over the prior year’s $2.31 billion [F1]. This reversed a slight net income dip observed in prior years (a -1.9% decline in 2024 vs. 2023). The earnings momentum reflects expansion in net interest income amid loan portfolio growth coupled with elevated fee income across diversified financial service offerings, as noted by recent industry commentary [N5].

Though revenue and operating income series are not available from disclosed XBRL tags, the substantial growth in net income implies prudent expense management complemented by positive mix shifts favoring higher-margin activities typical within regional banking franchises leveraging non-interest revenues.

Loan Growth and Fee Income Powering Momentum

Recent analysis underscores loan portfolio expansion as an immediate lever boosting Fifth Third’s top-line interest income base together with robust fee-based revenue streams derived from advisory services, transaction fees, and wealth management products [N1][N5][N10]. The bank’s ability to balance credit risk amid geographic and industry concentration mitigates vulnerability while feeding organic growth opportunities.

Loan portfolio diversification benefits come into sharper focus against competitive pressures faced by regional banks maintaining granular exposure across commercial lending categories and retail banking segments.

Merger with Comerica: Risk and Opportunity Assessment

The strategic rationale behind Fifth Third's planned merger with Comerica Incorporated is accompanied by discrete risks inherent to large-scale integration efforts [S4][S6][S12]. Merger agreements incorporate operational restrictions limiting routine business actions during pending close periods, elevating execution risks that include potential regulatory delays or extended timelines for anticipated cost synergies.

Regulatory scrutiny spans enhanced capital adequacy requirements given the enlarged consolidated entity size. The issuance of new common shares to fund parts of the acquisition creates dilution concerns albeit partially offset by expected long-term scale efficiencies.

Management explicitly acknowledges reputational risks involving customer retention challenges and cultural integration complexities typical of multi-regional bank combinations.

Capital Structure and Shareholder Returns

Capital allocation remains disciplined with total equity enlarging from $19.65 billion in 2024 to $21.72 billion by end-2025, underpinning an approximate return on equity of 11.6%, signifying effective deployment of shareholder funds despite muted disclosure on ROE metrics [F1].

Dividend payments hovered at roughly $1.16 billion without material change from prior year levels suggesting consistency in payout policies; dividend yields have recently crossed above the psychologically relevant threshold of 3%, appealing to income-oriented investors amid rate volatility [N11][N12].

Conversely, repurchase activity declined to $525 million from $625 million reflecting heightened prudence linked to merger-related uncertainties restricting aggressive buybacks at this junction [F1].

The company’s capital structure is further diversified through multiple series of preferred stock offering fixed-to-floating coupons that enhance funding flexibility while preserving common equity cushions [S3][S8][S9].

Operating Cash Flow and Investment Trends

Operating cash flow demonstrated remarkable strength with CFO surging almost 60% year over year to $4.51 billion in FY2025 from just $2.82 billion previously, signaling robust core cash-generative capacity notwithstanding cyclical banking trends [F1]. This uplift aligns with improved loan collections and fee realizations.

Simultaneously, capital expenditures rose sharply by over 40%, reaching $584 million versus $414 million a year earlier—likely reflecting escalated investments into technology infrastructure upgrades including digital platform enhancements aimed at competitive positioning post-merger [F1].

Resulting free cash flow approximates $3.93 billion illustrating ample liquidity for operational needs alongside sustained capital returns under existing frameworks.

Regulatory Oversight and Legal Considerations

Legal proceedings are generally referenced without material escalation per statutory filings integrated into the annual report’s notes section [S1]. Regulatory oversight intensifies amid merger reviews encompassing assessments around cybersecurity controls, capital requirement compliance, anti-money laundering protocols, and systemic risk mitigation frameworks essential within modern banking operations [S4][S12].

Risk disclosures highlight vulnerabilities associated with IT system upgrades incorporating artificial intelligence tools alongside traditional regulatory capital planning processes designed to support both standalone and combined entity resilience post-merger.

Outlook: Milestones and Market Signals to Monitor

Key upcoming milestones include federal regulatory approval timelines critical for transaction completion as well as merger close date confirmations per recent disclosures [N1][S3]. Integration progress tied to synergy delivery will serve as barometers for investor confidence restoration.

Market sentiment currently registers caution evidenced by ETF outflows linked to financial sector exposure and pronounced put-call option activity indicating hedging or speculative positioning around FITB shares ahead of further clarity on merger outcomes [N7][N8]. Equity compensation linked to performance shares awarded specifically for integration success underscores management’s incentive alignment towards seamless execution during this critical period [S27].

Fundamental growth drivers anchored on balanced loan book diversification alongside fee-income streams offer a platform for sustainable earnings expansion provided macroeconomic conditions remain stable across regional markets.

Historical Financial Summary (USD millions)

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 2.5 | 4.5 | 584 | +9.0% |

| 2024 | 2.3 | 2.8 | 414 | -1.5% |

| 2023 | 2.3 | 4.5 | 491 | -4.0% |

| 2022 | 2.4 | 6.4 | 348 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($bn) |

|---|---|---|---|

| 2025 | 1163 | 525 | 3.9 |

| 2024 | 1176 | 625 | 2.4 |

| 2023 | 1060 | 200 | 4.0 |

| 2022 | 927 | 100 | 6.1 |

Source: SEC companyfacts cache [F1].

This analysis is based solely on publicly available information including filings with the Securities and Exchange Commission and reputable news sources as of February 25, 2026. It does not provide investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments