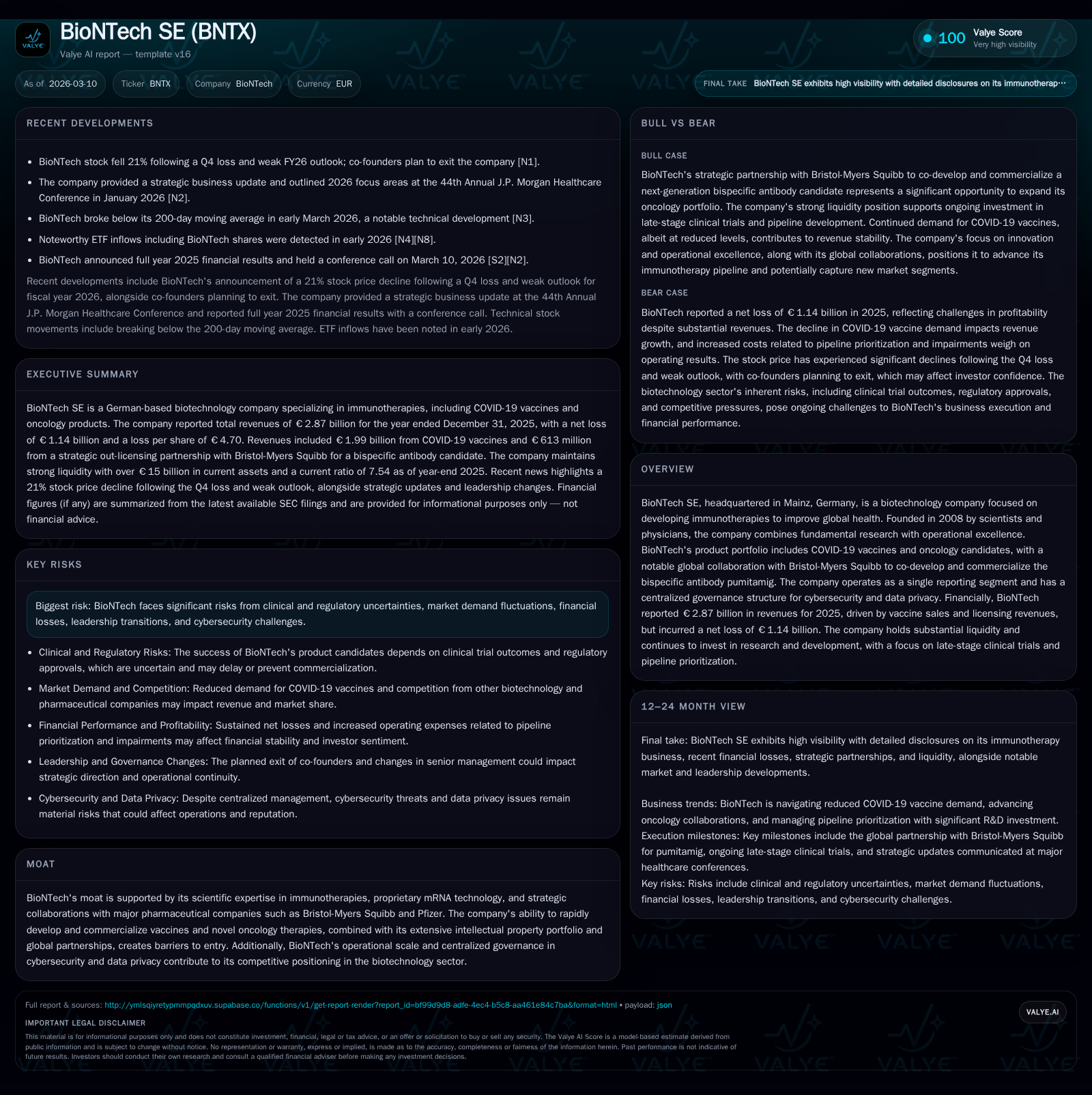

BioNTech Faces Profitability Challenges as Co-Founders Exit and FY26 Outlook Weakens

BioNTech’s transition from pandemic-driven revenues to a multi-product future is marked by financial losses, leadership changes, and ambitious R&D investments.

BioNTech SE reported growing revenues in 2025 driven by COVID-19 vaccine sales and lucrative out-licensing deals but returned to a net loss of €1.14 billion. The company’s foundational mRNA technology and partnerships, particularly with Bristol-Myers Squibb for pumitamig, underpin its future oncology pipeline, though near-term profitability remains elusive. Leadership shifts, including the announcement of co-founders forming a separate mRNA venture, add strategic uncertainty. Market watchers should track BioNTech's late-stage clinical progress and risk exposure as it aims to diversify beyond its pandemic legacy.

Historical Performance

BioNTech SE has demonstrated fluctuating financial performance since its IPO in October 2019, with peak revenues of €3.82 billion in 2023 primarily driven by COVID-19 vaccine sales. The pandemic tailwinds faded into 2024–25 with revenues moderately declining then rebounding slightly to €2.87 billion in 2025 [F1][S1]. Despite growth in total revenues largely due to out-licensing income from the BMS deal, BioNTech returned to a significant net loss of €1.14 billion in 2025 compared to a smaller loss of €665 million the prior year [F1][S1].

Historical performance (annual)

| FY | Net ($bn) | Net YoY |

|---|---|---|

| 2025 | -1.1 | -70.8% |

| 2024 | -0.7 | -171.5% |

| 2023 | 0.9 | -90.1% |

| 2022 | 9.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | -5.9 | |

| 2024 | 484 | -3.4 |

| 2023 | 484 | 4.6 |

| 2022 | 484 | 47.0 |

Source: SEC companyfacts cache [F1].

Note: Operating profit/loss reflects IFRS results inclusive of impairments and restructuring costs.

Cost of sales increased significantly (+19% YoY from €541 million in 2024), influenced by higher vaccine delivery volumes within Pfizer’s territory where BioNTech recognizes gross profits, alongside inventory write-downs exceeding €160 million related to scrapping and net realizable value adjustments [S4][S5][S18].

Despite an 18% decline in direct vaccine sales year-over-year to approximately €1.99 billion due to market normalization post-pandemic, substantial upfront out-licensing payments partially offset this drop — notably the $1.5 billion (~€613 million recognized as revenue during fiscal year) upfront payment from the June 2025 global pumitamig collaboration with Bristol-Myers Squibb [S10][S18]. This transaction broadens BioNTech’s revenue base beyond vaccines.

Future Growth Prospects

BioNTech aims to evolve into a multi-product biopharmaceutical company around 2030 through advancing oncology candidates leveraging its proprietary mRNA platform and bispecific antibodies like pumitamig [S3][S10]. The strategic partnership with Bristol-Myers Squibb grants co-exclusive licensing rights for development and commercialization along with shared costs and global profit splitting [S10]. Milestone payments under this agreement could reach up to $7.6 billion contingent upon successful development and commercialization milestones through 2028.

Pipeline prioritization continues with impairment charges reflecting project terminations or deprioritizations; however, late-stage trial acceleration is anticipated especially for immuno-oncology (IO) and antibody-drug conjugate (ADC) programs [S4][S5]. These areas are highly competitive but offer substantial value for first-to-market successes.

Headwinds remain: the COVID-19 vaccine market is normalizing with seasonal demand fluctuations; regulatory uncertainties around new product approvals persist; intense competition exists within mRNA-based oncology therapeutics requiring significant capital commitment [S6][S22]. Furthermore, the announcement that co-founders Sahin and Türeci plan a separate company focused on next-generation mRNA innovation may introduce strategic complexity or refocus organizational priorities at BioNTech itself [N6][S3].

Forecasts & Milestones

Explicit forward guidance for fiscal year 2026 was not provided [S1][N6], but key investor focus areas will include:

- Progression of late-stage trials for IO and ADC candidates.

- Revenue recognition milestones related to the BMS pumitamig partnership.

- Management of COVID-19 vaccine sales declines amid evolving health demands.

- Outcomes related to organizational restructuring following leadership changes.

The market responded negatively post Q4 earnings release with shares falling over 20%, reflecting skepticism about near-term profitability amid losses and leadership transitions [N6][N7].

Returns & Capital Allocation

BioNTech’s return on equity stands negative at approximately -5.9% based on net income of -€1.14 billion against shareholder equity of roughly €19.22 billion as of December 31, 2025 [F1]. This contrasts sharply with positive returns during peak pandemic years but aligns with industry norms during heavy investment phases transitioning pipelines.

While explicit operating cash flow data is unavailable publicly, BioNTech maintains strong liquidity with nearly €7.7 billion in cash and equivalents plus a current ratio above seven times current liabilities [F1][S26], supporting substantial annual R&D expenditures exceeding €2 billion [S4][S5].

No dividends were declared for fiscal year 2025 following prior consistent payments around €484 million annually during pandemic years, indicating capital preservation amid ongoing losses [F1].

Strategic & Operational Considerations

BioNTech has centralized cybersecurity governance through an Information Security Management System (ISMS), formalized in late 2025 under COO Sierk Poetting supported by an independent Chief Information Security Officer role — highlighting elevated vigilance against cyber risks critical to protecting proprietary technology and clinical data amid growing threats in life sciences [S22].

The company reports as a single segment with geographical diversification primarily centered in Europe where asset impairments have affected property outside Europe [S21][S4]. Its partnering strategy extends beyond Pfizer’s COVID vaccine collaboration into oncology alliances including those with Genentech/Roche nurturing pipeline candidates for future growth [S24].

Summary

BioNTech SE's transition beyond its blockbuster pandemic-era vaccines is marked by strong scientific capabilities backed by strategic partnerships but challenged by widening losses and evolving leadership dynamics. Its technological moat based on mRNA expertise remains intact with promising collaborations offering long-term optionality in oncology.

Investors should monitor clinical milestone progressions, commercialization strategy post-pandemic normalization, capital deployment effectiveness, and how organizational restructuring supports multi-product ambitions amid this transformative phase.

This report is based solely on publicly available documents as of March 2026 including BioNTech's SEC filings and relevant market news sources without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments