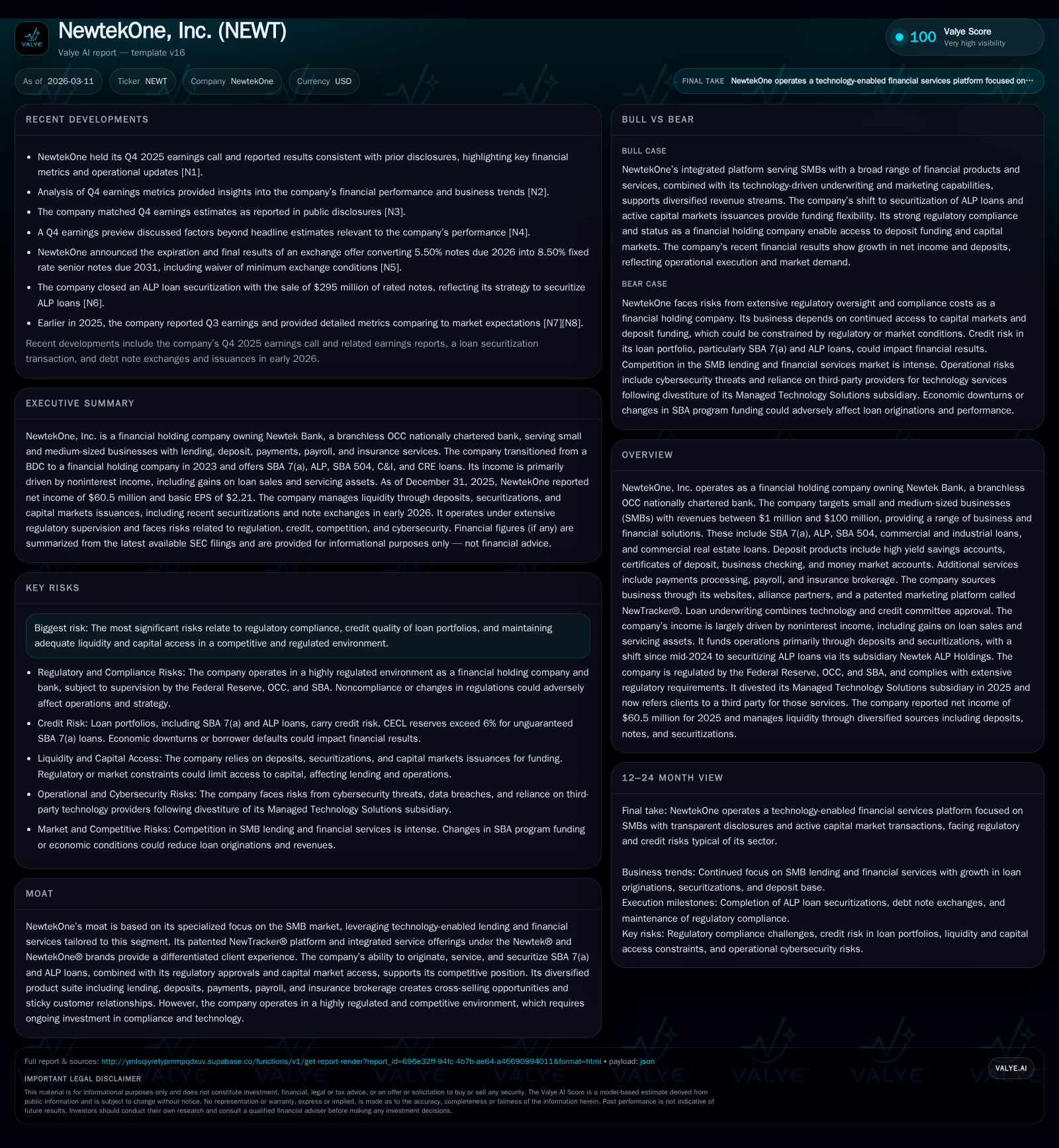

NewtekOne’s Transition to Financial Holding Company Drives Growth with Securitized ALP Loans and Diversified SMB Services

NewtekOne leverages its branchless banking model and technology platform to serve SMBs with a broad suite of lending and financial products, amid regulatory demands and evolving capital strategies.

NewtekOne, Inc. operates as a financial holding company centered around Newtek Bank, targeting small and medium-sized businesses with tailored lending and financial services. Since its 2023 shift from a BDC to a financial holding company and acquisition of Newtek Bank, the company has expanded its loan securitization capabilities, particularly in ALP loans. Its income is driven largely by noninterest income from loan sales and servicing fees. Liquidity remains supported by diversified deposits and capital markets issuances, while regulatory compliance and competitive pressures pose ongoing challenges. The company reported a 19% rise in net income for FY2025 driven by these core operational shifts, but continued negative operating cash flow signals investment and growth costs.

Company Overview

NewtekOne, Inc. repositioned itself fundamentally in early 2023 when it transitioned from a business development company (BDC) to a financial holding company through the acquisition of Newtek Bank, an OCC nationally chartered branchless bank [S1]. This marked a pivotal strategic shift dramatically broadening its product offerings, regulatory framework under the Federal Reserve and OCC supervision, and capital access.

The company's core market remains small and medium-sized businesses (SMBs) with revenues between $1 million and $100 million—a segment traditionally underserved by larger banks yet prolific in number (estimated over 34 million U.S. businesses) [S18]. Under its Newtek® and NewtekOne® brands, capabilities encompass SBA flagship loan products (7(a), ALP, 504), commercial & industrial loans (C&I), commercial real estate lending (CRE), deposit products including high yield savings accounts and zero-fee business checking, payments processing, payroll services, and insurance brokerage.

A notable component supporting client acquisition is the proprietary patented marketing platform NewTracker®, which enables data-driven prospecting and relationship management primarily through digital channels complemented by voice/video engagement [S1].

Historical Growth & Performance Drivers

Post-transition fiscal years reveal key drivers:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 61 | -579 | 106000 | +19.0% |

| 2024 | 51 | -153 | 439000 | +7.4% |

| 2023 | 47 | -169 | 458000 | |

| 2014 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 28 | 0 | -579 |

| 2024 | 20 | 402000 | -153 |

| 2023 | 14 | -170 | |

| 2014 |

Source: SEC companyfacts cache [F1].

[Financed via capital markets issuance/tap offerings], net income growth has been supported primarily by incremental noninterest income — notably gains on sale of SBA-backed loans and servicing fees deriving from retained portfolios [S1]. Despite rising earnings, operating cash flow remains deeply negative reflecting substantial funding needs for large volumes of loans held for sale (notably approximately $1.1 billion funded in FY25) [S4][F1]. Capital expenditures scale down substantially as digital platforms mature.

The increase in equity over this period parallels capital raises through registered offerings and ATM stock sales—enabling infrastructure investments supporting technology-enabled underwriting combined with credit committee oversight [S13][F1]. The dividend payout increased year-over-year yet remains moderate relative to net income.

Business Model Nuances: Loan Origination & Income Composition

NewtekOne distinguishes itself from conventional banks primarily by generating majority revenue not through net interest margins but via noninterest income streams — specifically gains on loan sales exceeding historically above 10% premiums on SBA guaranteed portions sold within 180 days post-origination [S10]. The unguaranteed loan portions are retained on balance sheet alongside reserve provisioning that exceeds standard CECL threshold levels (6%).

Moreover, servicing-retained loans produce servicing assets that provide predictable recurring fee income streams contingent upon loan amortization schedules [S10]. This hybrid model aligns well with SMB credit risk profiles while leveraging government guarantees.

A strategic recent shift occurred in mid-2024 concerning American Lending Program (ALP) loans which have longer terms (10-25 years), fixed rates reset quinquennially, often with prepayment penalties [S18]. Previously originated mainly for JV sales; since Q3/24 ALP loans are kept internally within sponsored securitizations through Newtek ALP Holdings — exemplified by a $216.6 million securitization closed in April 2025 rated 'A (low)' by Morningstar DBRS [S18][S19]. This internalizes returns but requires effective liquidity and capital management.

Deposit Base & Funding Profile

Total deposits climbed significantly by $444 million or about 47% over calendar year 2025 to reach $1.4 billion at year-end—underpinned by Newtek’s competitive high-yield deposit products fostering ‘sticky’ relationships important for sustained funding stability amidst competitive pressures [S8]. Approximately three quarters of deposits are FDIC-insured which mitigates liquidity risk.

Funding also includes diverse borrowings: bank notes payable, notes payable securitization trusts related to off-balance sheet transactions, lines of credit from multiple commercial banks/financial institutions such as Capital One & Deutsche Bank facilities across SPV conduits for asset-backed securitizations [S7][S19]. These structured credit arrangements underpin the ALP loans’ long-term amortizing nature.

The Company actively accesses capital markets annually issuing notes ranging from maturities through decade ends—recently closing private placements including $30 million aggregate principal amount of its unsecured senior notes due in 2030 at an approximate coupon of ~8.375% starting October 2025 [S15][S16][S22]. Interest expenses here reflect prevailing credit spreads supportive of flexible refinancing options.

Regulatory Environment & Compliance Risks

Operating as a nationally chartered bank holding company subjects NewtekOne to rigorous Federal Reserve supervision alongside OCC oversight for Newtek Bank operations congruent with banking regulations governing safety & soundness, capital adequacy (with Tier-1 Capital ratio around ~15%), liquidity frameworks, AML/CTF protocols as well as adherence to SBA guidelines applicable to loan origination/sale practices [S12][S14].

Given the legacy transition from a BDC model to a full-scale bank holding company plus multi-jurisdictional compliance demands from banking regulators plus SBA rule changes creates ongoing investment needs into compliance staff and technology infrastructure.

There are elevated risks from adverse regulatory scrutiny given historical FTC litigation involving some subsidiaries within payment processing arms requiring permanent injunctions restricting certain sales practices [S12][S14]. Further increasing complexity stems from tightened payments industry regulations addressing data security/privacy enhancing operational costs which may constrain volume growth if customers alter behavior.

Credit quality remains monitored tightly given portfolio concentration towards SMB borrowers often sensitive to economic volatility or sector-specific downturns within heterogeneous industries served.

Future Growth Opportunities & Constraints

Growth avenues include scaling ALP securitization issuance leveraging attractive fixed-rate long amortizing loan characteristics appealing to institutional investors seeking yield enhancement beyond Treasury proxies given embedded prepayment protection features [N1][S18][S19]. Cross-selling integrated product suites—payments processing coupled with payroll & insurance brokerage embedded within the Newtek Advantage 'one dashboard' digital interface—creates ‘stickiness’ fostering deeper wallet share per client [S1][S18][N2].

However, challenges persist:

- Regulatory uncertainty or tightening could elevate compliance costs or limit product innovation capability [S12].

- Credit losses or reserve inflation could impair profitability especially if macroeconomic headwinds intensify default rates on unguaranteed tranches.

- Raising additional capital might become onerous if market conditions worsen or share price declines restrict ATM program effectiveness [S25][N3].

- Competitive landscape with fintech challengers offering digitally native SMB lending platforms increases client acquisition pressure despite differentiated embedded service models.

Operationally internalizing ALP loans drives better margin control but increases reliance on volatile capital markets issuance cycles requiring timing precision.

Capital Allocation & Returns

ROE approximates a robust ~15% based on FY2025 net income versus shareholders’ equity—a positive signal about operational leverage translating into equity returns despite cash outflows associated with rapid balance sheet growth [F1].

Dividends paid increased significantly over recent years reflecting a stake-holder oriented policy yet share repurchase activity remains modest given reinvestment priorities amid scaling operations [F1][S24].

Liquidity management balances large negative annual CFO driven by front-loading loan originations offset partially by financing activities including bond issuances totaling over $750 million net inflows during FY25 showing adept capital structure flexibility allowing stable deposit-growth coupled with debt issuance programs anchored by institutional investor demand [S4][S5]. Restricted cash reserves linked to collateralized securitizations alongside compliance buffers temper risk exposures.

What To Watch: Forecasts & Milestones Analysis

While explicit forward guidance is not provided publicly within filings or transcripts reviewed through Q4/25 earnings commentary , key milestones will include:

- Quarterly originations volume trends highlighting successful funnel-to-close conversion within SBA-related lending products.

- Execution pace on ALP loan securitization transactions reflecting investor appetite in evolving fixed rate senior/subordinate tranches amid rising interest rate environments.

- Deposit base expansion metrics illustrating new client acquisition alongside retention under the Newtek Advantage ecosystem digital interface deployment progress.

- Monitoring noninterest income fluctuations stemming from servicing assets amortization schedules impacting recurring fee revenue predictability.

- Regulatory developments impacting allowable underwriting criteria or prudential limits influencing overall risk appetites.

- Ongoing cost efficiency improvements especially pertaining to technology upgrades addressing compliance burden increments expected within payments processing segment [S12][N2].

- Capital deployment decisions regarding opportunistic note buybacks versus dividend reinvestment balancing shareholder return objectives versus growth reinvestment needs [S24].

Conclusion

NewtekOne has redefined its strategic identity leveraging regulatory status elevation accompanied by integration of banking products into a singular platform targeting independent business owners underserved by major lenders. Its innovative combination of technology-enabled origination processes plus balance sheet management enhanced via targeted securitizations underpins growth while maintaining sound capitalization metrics suitable for rigorous regulation.

Risks remain meaningful especially tied to compliance rigor amidst regulatory intensification plus execution risks inherent in transitioning product mix toward longer duration fixed-rate assets within ALP securitizations demanding sophisticated liquidity forecasting ability.

Overall NewtekOne presents an interesting hybrid banking-lending fintech model focused on the SMB niche combining digital client engagement with complex financing architectures requiring ongoing monitoring for operational scalability balanced against regulation-driven cost burdens.

This analysis is intended solely for informational purposes reflecting data available as of March 2026 without any investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments