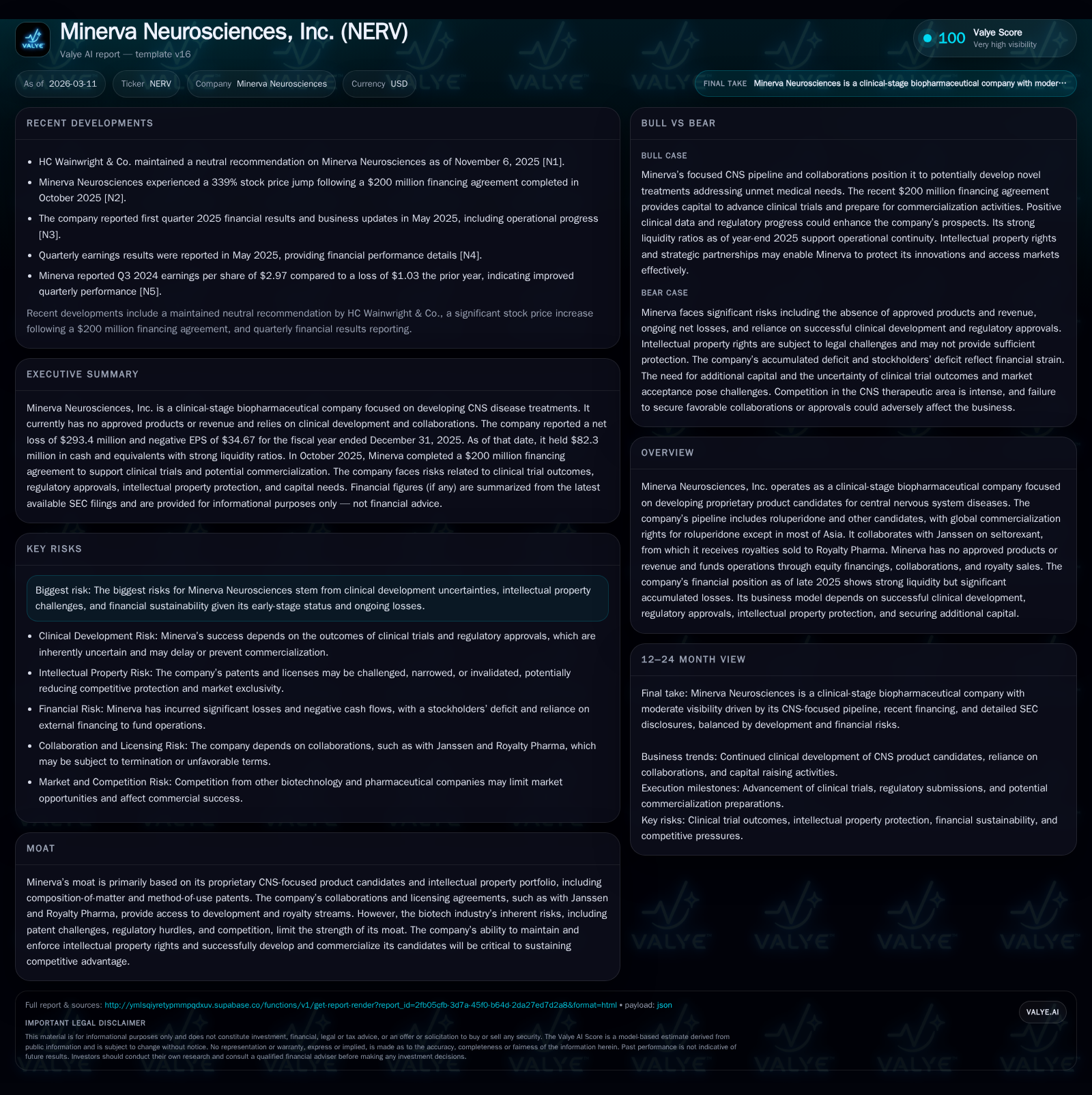

Minerva Neurosciences' Transition from Clinical Development to Commercial Potential

Examining how Minerva’s CNS pipeline progress and financial strategy underpin its path from clinical-stage biopharma to market readiness.

Minerva Neurosciences remains a clinical-stage biopharmaceutical company focused on proprietary CNS therapeutics, notably roluperidone. Despite sustained operating losses and no commercial revenue, expense reductions aligned with pipeline maturity have improved operating income recently. The company’s liquidity is bolstered by a sizable private placement and royalty asset monetization, supporting upcoming Phase 3 trials and regulatory submissions. Intellectual property rights and partnerships are central, yet development and financing risks persist as Minerva navigates the challenging pivot from R&D to commercialization.

Historical Financial Trajectory: Expense Reduction and Persistent Operating Losses

Minerva Neurosciences' financial performance through FY2025 illustrates the challenges common to clinical-stage biopharmaceutical companies focused on CNS disorders. The company has consistently operated at a loss, with operating income improving from approximately -$21.8 million in 2024 to -$15.1 million in 2025, a roughly 31% year-over-year reduction [F1]. This improvement largely reflects strategic expense management as research and development activities evolve alongside pipeline progression.

Operating expenses decreased notably, with research and development staff-related expenses declining from about $2.25 million in 2024 to $1.5 million in 2025, alongside significant reductions in drug product material costs [S5]. General and administrative expenses remained relatively stable but were managed tightly to contribute to the overall cost containment.

Minerva has not generated commercial revenues from product sales; historical revenues relate primarily to licensing or milestone events [F1][S5]. This absence of product-derived income contributes to substantial net losses—reported at approximately -$293 million in 2025—and negative operating cash flow of about -$13.5 million during the same period [F1]. Capital expenditures remain minimal relative to operational spending.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -293 | -14 | -15 | -20492.7% | |

| 2024 | 1 | -20 | -22 | +104.8% | |

| 2023 | -30 | -15 | -23 | 16326 | +6.6% |

| 2022 | -32 | -25 | -25 | 16326 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 208.5 | |

| 2024 | -5.6 | |

| 2023 | -15 | 105.4 |

| 2022 | -25 | 160.3 |

Source: SEC companyfacts cache [F1].

Table: Selected annual financial metrics for Minerva Neurosciences through FY2025 [F1]

Core Growth Drivers: Pipeline Assets and Licensing Collaborations

Minerva’s primary growth driver is its proprietary CNS-focused pipeline, notably roluperidone, which targets the negative symptoms of schizophrenia. The company holds global commercialization rights for roluperidone outside most Asian markets [S5]. The clinical strategy involves addressing unmet needs through confirmatory Phase 3 trials following FDA guidance after an initial Complete Response Letter [S15].

Additionally, Minerva benefits from collaborations such as those with Janssen Pharmaceuticals concerning seltorexant, another CNS candidate addressing insomnia associated with major depressive disorder [S24]. Minerva monetized anticipated royalty streams from seltorexant by selling these rights to Royalty Pharma for an upfront payment of $60 million plus potential future milestones up to $95 million contingent on Janssen's clinical progress [S24]. This transaction provided immediate liquidity while transferring some commercial risk.

The interplay between internal pipeline development and external royalty monetization defines Minerva’s strategic positioning amid the inherent uncertainties of drug development cycles.

Forward Outlook: Upcoming Clinical Milestones and Regulatory Pathways

A pivotal upcoming event is the initiation of the confirmatory Phase 3 C19 trial for roluperidone expected in Q2 2026 [S15]. This trial is designed based on FDA feedback received after the February 2024 Complete Response Letter and aims to evaluate efficacy using established endpoints over a treatment period including a long-term relapse observation phase.

The trial will enroll approximately 380 patients randomized between placebo and a daily dose of roluperidone, with a key focus on PANSS Marder negative symptom factor score changes at week twelve [S15]. Successful completion will be critical for NDA resubmission considerations and potential approval timelines.

Capital Structure and Liquidity Position

Following a private placement completed in October 2025 involving Series A convertible preferred stock issuance, Minerva secured upfront gross proceeds of $80 million with additional potential capital up to $200 million via warrants exercisable upon milestones [S16][S18].

This financing significantly strengthened liquidity, elevating cash, cash equivalents, and restricted cash balances to approximately $82.3 million as of December 31, 2025, against current liabilities near $2.3 million—yielding a robust current ratio around 36 [F1]. Such liquidity provides a sizeable buffer ahead of expensive late-stage clinical activities.

Other funding sources include collaboration-generated royalties (though sold) and corporate finance activities aligned with ongoing development needs [S7][S11][S18]. Management indicates ongoing evaluation of capital requirements tied closely to clinical progress.

Intellectual Property Portfolio as a Strategic Asset

Minerva maintains patent protections covering composition-of-matter and method-of-use claims relevant for its CNS therapeutic candidates [S10][S19]. These patents constitute critical barriers against generic competition during commercialization windows.

Patent prosecution involves both internal efforts and reliance on licensors where applicable; the company holds rights allowing it to pursue maintenance independently if licensors do not continue prosecution [S10]. Intellectual property strategy remains integral amid competitive CNS drug landscapes.

Risks Impacting Development Continuity and Financial Health

Key risks include:

- Uncertainty surrounding clinical trial outcomes given high failure rates typical in CNS drug development [S10][S15].

- Financial sustainability concerns due to large accumulated deficits exceeding $680 million at FY-end 2025 despite recent liquidity improvements [F1][S18].

- Contingent liabilities related to royalty sales where failure by collaborators like Janssen could trigger compensation obligations toward Royalty Pharma [S24].

- Potential intellectual property disputes or challenges that could delay commercialization efforts [S19][S28][S29].

- Cybersecurity risks given sensitive data handling requirements inherent in clinical operations [S1].

Capital Allocation Focus: Reinvestment Over Distributions

Consistent with its developmental stage, Minerva does not pay dividends or engage in share repurchases; capital deployment is concentrated on advancing R&D programs and preparing regulatory submissions essential for future commercialization efforts [F1][S27].

This approach aligns logically with its negative net incomes and reinvestment priorities typical within early-stage biotechnology firms.

Key Upcoming Catalysts for Investors

Investors should monitor:

- Initiation and progress updates from roluperidone’s confirmatory Phase 3 C19 trial expected in Q2 2026 [S15].

- Regulatory feedback regarding NDA resubmission parameters.

- Updates on collaboration-derived royalties collection reliability under Royalty Pharma agreements.

- Developments related to capital raises or warrant exercises impacting shareholder dilution.

- Broader CNS market dynamics influencing competitive positioning.

In summary, while Minerva’s pipeline progression coupled with strengthened liquidity supports continued advancement toward commercialization goals, execution risks remain notable given the complexities of late-stage CNS drug development.

This analysis synthesizes publicly filed SEC disclosures complemented by Valye News domain expertise on biotech financial structures and CNS pharmaceutical development pathways. It is intended solely for informational purposes without recommendation regarding investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments