First Choice Healthcare Solutions’ Strategic Shift to Functional Wellness Clinics Amid Continued Financial Challenges

FCHS is transitioning away from orthopedic services to a national functional health and wellness clinic model, facing profitability and liquidity hurdles.

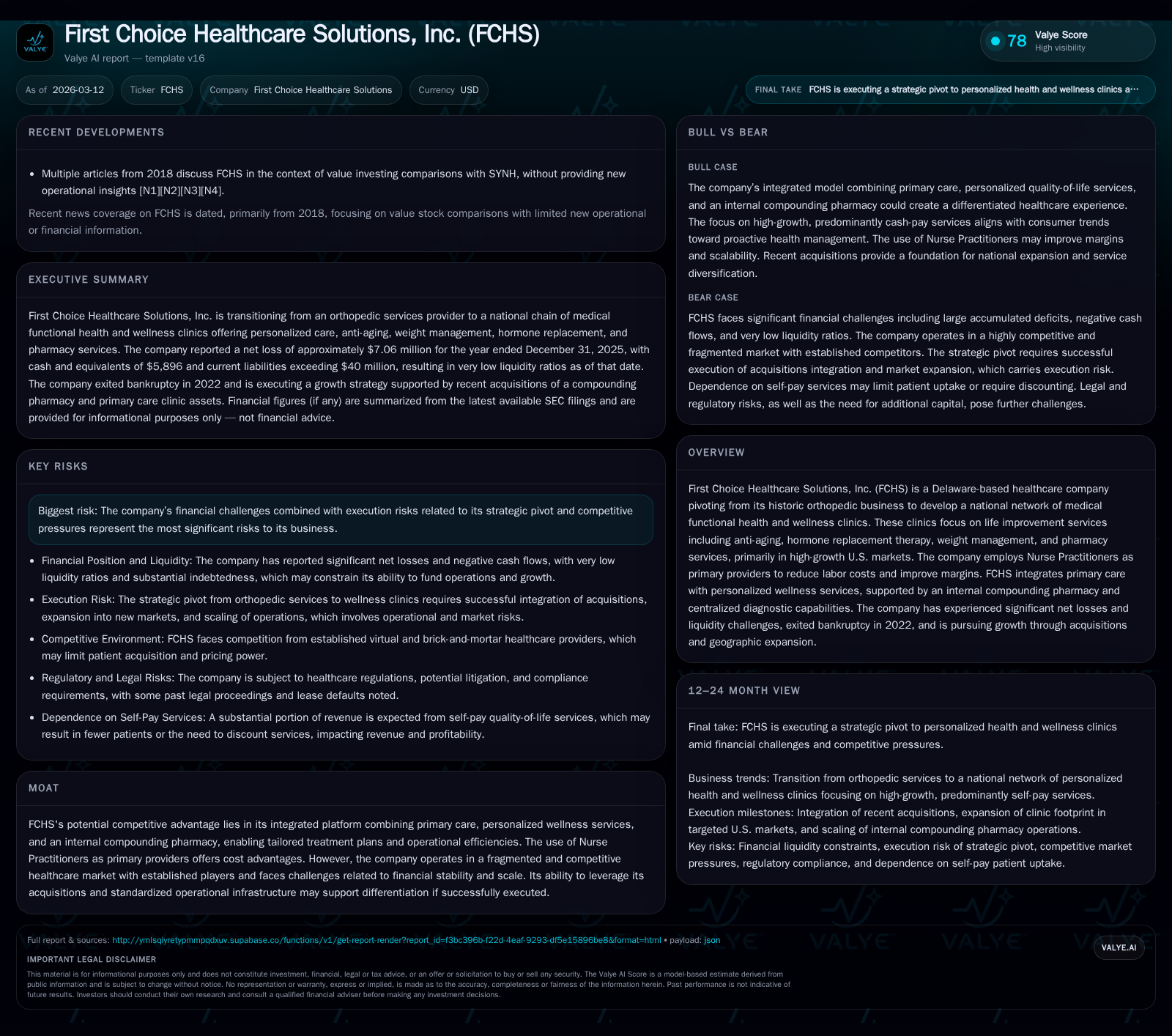

First Choice Healthcare Solutions, Inc. (FCHS) has pivoted from its legacy orthopedic business to focus on creating a national network of medical functional health and wellness clinics offering personalized, largely cash-pay services such as hormone replacement therapy and weight management. While this strategic shift targets high-growth U.S. markets and aims to leverage lower-cost Nurse Practitioners, the company remains burdened by historic financial losses, negative operating cash flows, and a highly leveraged balance sheet. Its future growth depends on successful acquisitions, operational execution, and access to additional capital amid regulatory complexities and competitive pressures.

Company Overview and Business Transformation

First Choice Healthcare Solutions, Inc. (FCHS), headquartered in Melbourne, Florida, is during a significant strategic transformation. Historically focused on orthopedic diagnostics, surgery, rehabilitation, and imaging services including MRI and ultrasound, the company has been moving away from these legacy offerings. The new core business revolves around establishing a chain of medical functional health and wellness clinics across high-growth U.S. markets. These clinics emphasize life improvement services such as anti-aging treatments, hormone replacement therapy (HRT), weight management, population health management, telehealth care, laboratory diagnostics, compounding pharmacy services, and select dermatological procedures (e.g., Botox injections).

FCHS envisages delivering personalized care tailored to patients' unique biology via integrated primary care supported by specialized therapies like peptide treatments and biohacking. Their model hinges on leveraging licensed Nurse Practitioners (NPs) as primary providers — an approach designed to reduce labor expenses substantially while boosting margins by approximately 25% compared with physician-led clinics [S4][S5][S6]. This pivot aligns with broader trends favoring personalized medicine outside traditional insurance reimbursement models.

Historical Financial Performance

Over recent years, FCHS's financial performance has been notably challenged as it contended with legacy operational issues compounded by legal troubles related to prior executive misconduct culminating in bankruptcy proceedings during 2020. Despite emerging from bankruptcy reorganization in early 2021 [S18], the company’s fiscal results reveal persistent losses:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | -1 | -3 | -80.9% | |

| 2024 | -4 | -2 | -1 | 82918 | +52.9% |

| 2023 | -8 | -7 | -2 | 82918 | |

| 2017 | 4 | -4 | 330439 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 17.6 | |

| 2024 | -2 | 11.9 |

| 2023 | -7 | 28.6 |

| 2017 | 35.4 |

Source: SEC companyfacts cache [F1].

[F1]

Cash flow from operations remained negative across these periods despite sequential improvements in 2025 signaling better cost controls or revenue stabilization efforts. The company recorded an accumulated deficit exceeding $74 million at year-end 2025 [S1][F1]. Current liquidity is severely constrained with current liabilities ($40.7 million) greatly surpassing current assets ($6.6 thousand), leading to a current ratio approaching zero [F1]. This mismatch underscores material uncertainty about FCHS’s ability to continue without raising external funds imminently [S3][S8][S16].

Market Positioning and Growth Prospects

FCHS targets state markets granting Nurse Practitioners full practice authority—currently active in at least 27 states plus D.C.—which facilitates clinic scalability by reducing provider credentialing constraints [S6]. The initial expansion focus for 2026-27 includes northeast/southwest Florida and Minnesota with ongoing evaluations for Denver and Phoenix [S5].

The company's services largely emphasize self-pay tiers comprising higher-margin offerings such as compounded pharmaceuticals for HRT/TRT (testosterone replacement therapy), metabolic therapies including medically assisted weight loss programs, regenerative peptides, inflammation management markers testing/treatment alongside insured primary care coverage avenues [S4][S5].

Marketing efforts incorporate a multi-channel digital-first approach combined with conventional media spots targeting demographics keen on proactive health optimization including athletes/corporate executives/aging populations [S5][S10]. Referral incentives internally bolster cross-selling ancillary products like vitamins/nutraceuticals sold within clinics.

One notable competitive edge resides in FCHS's vertically integrated platform combining: centralized electronic medical records compliant with federal Meaningful Use standards; internal compounding pharmacy enabling personalized medication plans; remote monitoring technologies; plus scalable infrastructure supporting geographically dispersed units via cloud technologies that other emerging wellness chains might lack [S11]. The clinical model emphasizes longitudinal care over episodic interventions emphasizing quality-of-life metrics rather than acute episode response typical of traditional orthopedic clinics.

Forecasts / Milestones / What To Watch For

Explicit company guidance remains limited but the strategic roadmap includes:

- Completion of geographic expansions into identified states starting Florida/Minnesota by end of 2027.

- Full exit from all legacy orthopedic/physical therapy service lines.

- Integration progress milestones related to Live Well Medical Group clinics acquired recently along with Live Well Drugstore compounding pharmacy consolidation [S27].

- Cost reduction outcomes particularly related to provider staffing mix changes introduced since late 2021.

- Achievement of positive cash flow projections driven by self-pay revenue stabilization.

Analysts should monitor quarterly filings for evidence of increased top-line revenue which is currently very modest (latest public data shows revenue was $1 million+ only as far back as FY2013) [F1], as well as margin improvements resulting from scale benefits or pricing leverage. A successful capital raise or partnership deal would be critical events that affect liquidity risk profile [S3][S8]. Also key will be adherence to evolving multi-state regulatory compliance regimes especially billing code accuracy and fraud mitigation per federal Medicare/Medicaid rules detailed under Stark Law/Anti-Kickback statutes [S9][S12][S15][S19].

Returns & Capital Allocation

The company has not paid dividends historically nor does it plan any dividend distributions in the near term given ongoing losses and need for reinvestment [S14][S27]. Return on equity calculations are compromised by negative shareholders’ equity (approximately negative $39 million at end-2025), but a back-of-envelope ratio using net income against absolute equity magnitude suggests roughly mid-teens percentage leverage effect albeit on a heavily deficit basis—a non-standard measure given bankruptcy history [F1].

Capital expenditure requirements are relatively modest compared with revenues but steady ($82K capex recorded in FY2024/23) reflecting clinic equipment investments rather than heavy fixed asset spending seen in some other healthcare chains [F1]. Operating cash flows remain negative despite gradual improvement (-$549K in FY2025 vs -$1.7M prior year). Future capital needs will likely necessitate additional equity or debt issuance potentially leading to shareholder dilution or increased leverage based on current balance sheet stresses noted previously [S3][S8]. The company’s elevated current liabilities raise risks related to solvency absent successful capital procurement or operational turnaround.

Industry Context & Competitive Risks

FCHS operates within a highly fragmented U.S. healthcare market where functional wellness intersects both traditional clinical medicine regulated extensively by federal/state frameworks and emerging elective cash-pay verticals driven primarily by consumer demand for anti-aging/biohacking solutions projected to grow at ~19% CAGR through the next decade [S10]. This sector overlaps bespoke pharmaceutical compounding expertise with primary care delivery innovation requiring tight compliance oversight due to complex fraud/abuse laws including Federal False Claims Act exposure risks.

Unlike incumbents focused purely on insurance-reimbursed care or specialized biohacking boutiques lacking medical licensure depth, FCHS attempts an integrated hybrid model addressing lifetime wellness anchored around nurse practitioner-based longitudinal care. However, the transition risks are material: legacy financial burdens persist; execution demands are high given geographic regulatory variability; patient adoption rates for self-pay models depend heavily on economic conditions affecting disposable income; competition includes both large multispecialty groups leveraging scale advantages plus specialized niche providers focused purely on personalized medicine segments; litigation exposure remains due to past CEO indictment fallout plus ongoing lease dispute proceedings potentially imposing cost burdens [S13][S23]; finally governance concerns arise owing to concentrated ownership structure potentially complicating strategic decision agility [S14].

Conclusion

First Choice Healthcare Solutions stands at a crossroads emblematic of many small-cap healthcare operators shifting toward lifestyle-oriented wellness amidst challenging financial legacies and systemic healthcare regulatory complexities. Its ambition to build a national footprint of innovative wellness-focused clinics led predominantly by cost-efficient nurse practitioners reflects a modernized care delivery vision targeting growing consumer demand outside traditional insurance paradigms.

However, survival hinges critically on securing fresh capital infusion promptly aligned with disciplined execution of expansion plans while navigating pervasive regulatory risks inherent in multi-state medical operations involving sensitive billing practices coupled with cutting-edge pharmaceutical compounding activities. Despite years of losses spanning COVID-19 disruptions through restructuring following leadership scandals culminating in bankruptcy reorganization, the firm shows tentative operational improvements though off a low revenue base last reported above $1 million more than a decade ago. Market participants should monitor subsequent quarterly updates for signs of sustainable revenue traction, improvement in cash flow dynamics, and progress against stated expansion milestones while staying alert to legal/regulatory developments impacting operational legitimacy.

This analysis is intended solely for informational purposes based on publicly available regulatory filings through March 2026. It should not be construed as investment advice or a recommendation regarding securities of First Choice Healthcare Solutions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments