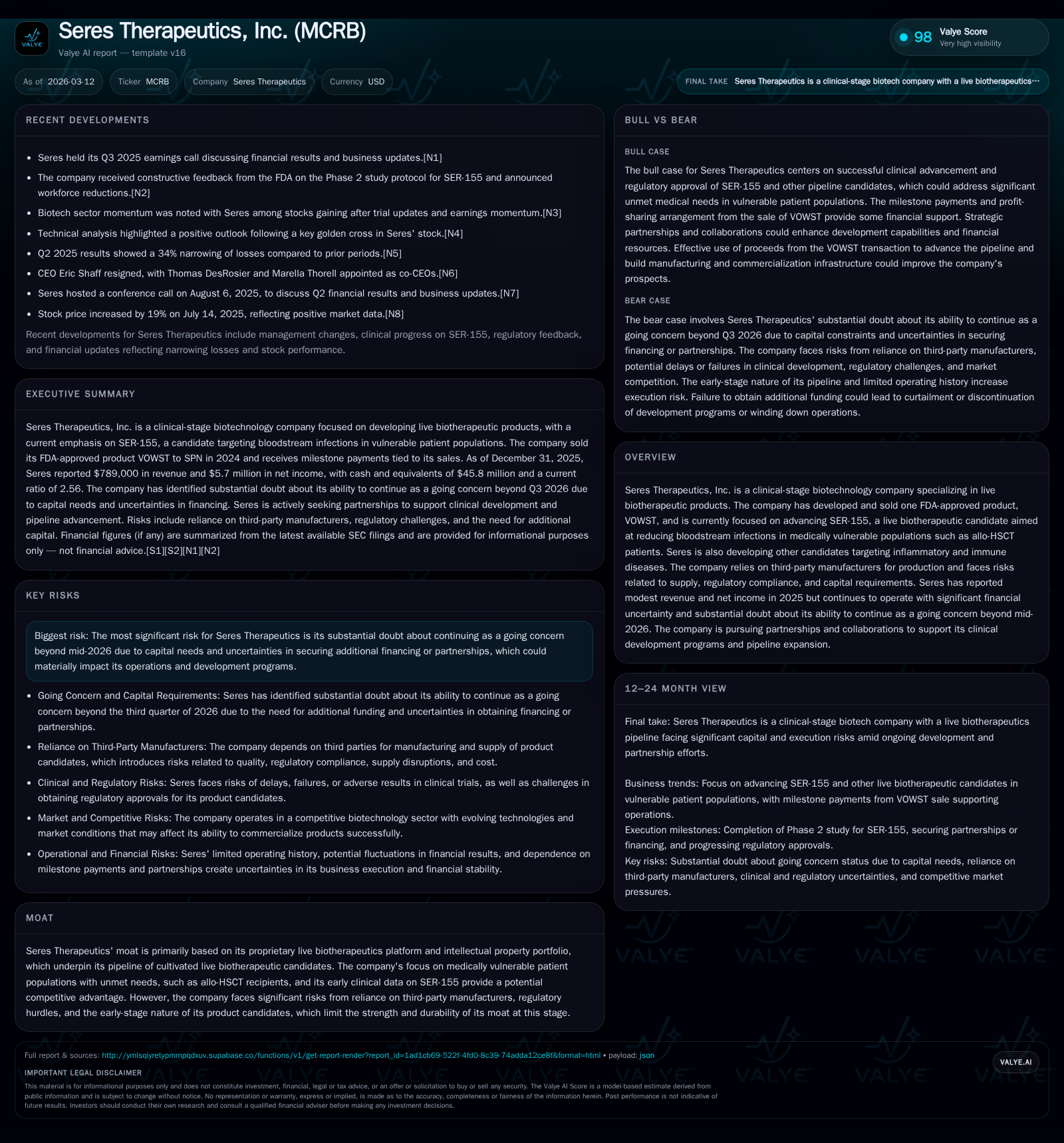

Seres Therapeutics' Transition from Revenue Collapse to Clinical Promise: Assessing Viability Amid Financial Strain

Seres Therapeutics confronts a steep revenue decline while advancing SER-155 development and wrestling with critical liquidity challenges.

Seres Therapeutics has witnessed a dramatic revenue drop from $145 million in 2021 to under $1 million in 2025, reflecting significant disruption after divesting its flagship VOWST business. Despite this, the company reports modest net income in 2025, driven by cost controls and non-recurring items, even as operating losses remain substantial. Its clinical pipeline centers on SER-155, targeting bloodstream infections in allo-HSCT patients, with ongoing efforts to secure partnerships amid looming financial sustainability concerns beyond mid-2026. Manufacturing dependency on third parties and tight regulatory compliance add operational complexity alongside capital raising imperatives.

From Early Momentum to Revenue Collapse: Charting Seres’ Growth Trajectory

Seres Therapeutics’ financial history over the last half-decade reveals a narrative marked by an abrupt revenue contraction that underscores structural shifts and strategic recalibrations. The company’s reported revenues peaked at approximately $145 million in fiscal year 2021 but plummeted precipitously to an almost negligible $0.8 million by fiscal 2025 — representing a staggering year-over-year decline of roughly 99.4% [F1]. This collapse primarily follows the September 2024 divestiture of its FDA-approved VOWST product line — a cultivated live biotherapeutic focused on recurrent Clostridioides difficile infection — along with associated commercial rights and manufacturing infrastructure [S16].

Operating income during this period portrays persistent losses despite steady improvements; the fiscal year 2025 operating loss narrowed by about 22.5% compared to the prior year, settling near negative $94 million [F1]. This reflects tighter expense discipline post-divestiture but still indicates ongoing high fixed costs and investment outlays primarily related to research and development programs. Notably, net income turned positive at just under $5.7 million in 2025 due chiefly to cost reductions and non-recurring items rather than core revenue generation [F1]. The underlying operating model reflects a biotech firm transitioning into clinical development phases without sustainable product earnings.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1 | 6 | 1 | -94 | +4088.2% | |

| 2024 | 0 | -149 | -121 | +100.1% | ||

| 2023 | 126 | -114 | -117 | -108 | +1672.2% | +54.5% |

| 2022 | 7 | -250 | -229 | -246 | -95.1% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1 | 12.9 |

| 2024 | -149 | 1.0 |

| 2023 | -125 | 253.5 |

| 2022 | -239 | -2319.9 |

Source: SEC companyfacts cache [F1].

Note: The apparent increase in revenue from FY2022 to FY2023 likely reflects interim operational factors prior to divestiture followed by the dramatic collapse post asset sale culminating in FY2025 results.

Product Portfolio Spotlight: FDA-Approved VOWST and the Clinical Hope of SER-155

Seres’ initial commercial footprint was anchored by VOWST — its sole FDA-approved live biotherapeutic product derived from cultivated consortia of gut microbiota aimed at reducing recurrences of C. difficile infection [S16]. After spinning off this asset and related intellectual property in late 2024 [S16], Seres redirected its R&D focus toward next-generation live biotherapeutics designed for niche but medically vulnerable populations.

The frontrunner candidate SER-155 exemplifies this pivot. It is engineered as a cultivated live bacterial consortium tailored specifically for allo-HSCT recipients — a cohort defined by immunocompromise and elevated susceptibility to bloodstream infections including antimicrobial-resistant pathogens [S2]. The pathological challenge involves gut microbial disruption leading to bacterial translocation into systemic circulation with significant mortality risks.

SER-155’s mechanism aims at microbiome restoration to reduce such infections during this vulnerability window [S2]. Planned Phase 2 studies will assess efficacy endpoints centered on prevention of bloodstream infections in allo-HSCT patients [S2]. Beyond this population, Seres explores expanding applications into other immunocompromised groups such as autologous HSCT recipients, neutropenic cancer patients, CAR-T therapy recipients, organ transplant patients, and those in intensive care settings — all recognized for dysbiosis-linked infection risks [S2]. This specialty focus underscores both opportunity and challenge given limited existing therapies but heightened clinical trial complexity.

Financial Health under Scrutiny: Capital Constraints and Going Concern Considerations

The sharp revenue decline combined with ongoing R&D spending has created acute liquidity pressures for Seres Therapeutics. Official disclosures explicitly state "substantial doubt" about the company’s ability to sustain operations beyond the third quarter of calendar year 2026 absent additional equity financing or securing partnership agreements [S1][S2]. These conditions arise despite maintaining approximately $45.8 million cash & equivalents at end-2025 [F1], which provides only limited runway given spending commitments.

Management cautions that favorable financing terms cannot be assured due to factors outside their control and failure to raise capital could force program curtailment or winding down operations entirely [S1]. Market perceptions tied closely to going concern classifications can restrict investor appetite and counterparties’ willingness for collaborations or licensing deals.

This frames a precarious balancing act between advancing SER-155 clinical trials requiring capital infusion and managing expenses prudently amid constrained resources.

The Clinical Development Roadmap: Milestones and Strategic Collaborations

Seres positions Phase 2 clinical evaluation of SER-155 as pivotal for near-term growth [S2]. Clinical endpoints prioritize reduction in life-threatening bloodstream infections driven by antimicrobial-resistant organisms among allo-HSCT populations — an area with inadequate standard prophylaxis options.

Successful demonstration of safety, microbiome engraftment, and efficacy could unlock significant commercial potential alongside intellectual property protection rooted in proprietary bacterial compositions [S2]. Concurrently, Seres actively pursues business development arrangements intended not only as sources of capital but also collaborative support encompassing manufacturing scale-up expertise and commercialization capabilities [S1][S2].

Exploratory programs targeting inflammatory bowel diseases like ulcerative colitis and Crohn's disease leverage platform technologies but remain earlier stage with less visibility on timelines [S2]. Analysts should monitor data readouts related to SER-155 plus partnership announcements as critical catalysts shaping medium-term viability.

Manufacturing Dependencies and Regulatory Barriers: Operational Risks

Reliance on third-party contract manufacturers constitutes material risk for Seres [S4][S7]. Live biotherapeutics production demands stringent adherence to current Good Manufacturing Practices (cGMP), especially given strain stability concerns inherent in cultured microbiome products destined for fragile patient subsets.

Regulatory authorities maintain vigilant oversight across manufacturing quality controls, labeling accuracy, safety monitoring (pharmacovigilance), post-market commitments, and promotional activities strictly limited by approved indications [S7][S11]. Violations including unapproved off-label promotion could result in severe sanctions ranging from fines to market withdrawal.

Complexity arises from multi-jurisdictional compliance requirements spanning US federal/state laws—such as anti-kickback statutes—and analogous international frameworks imposing fraud & abuse safeguards plus pricing/reimbursement constraints [S5][S13][S18][S22]. Failure or delays in obtaining necessary marketing approvals or reimbursement coverage will directly impede commercial scalability, mandating prudent risk management around legal/regulatory dimensions placed concurrently against tight budgets.

Capital Allocation Profile: Cash Flow and Shareholder Value Dynamics

From a financial stewardship perspective reflecting its clinical-stage biotech status [F1], operating cash flow modestly returned positive at approximately $1.1 million for fiscal year 2025 after prolonged negative outflows exceeding $117 million annually before divestiture altered expense profiles [F1]. Capital expenditures declined sharply from near $10 million pre-divestiture years down to around $250 thousand recently—consistent with scaled-back physical asset needs concurrent with outsourcing manufacturing functions.

Return metrics remain constrained; while net income registered a small positive number translating roughly into an approximate return on equity near 13%, this does not denote sustained profit generation but rather effects linked to one-time gains or adjustments alongside low equity base post restructuring [F1]. Seres has neither declared dividends nor engaged in share buybacks—typical for firms focusing available capital on advancing R&D programs versus returning cash.

Emerging free cash flow highlights operational stabilization albeit at low levels insufficient yet for self-sustaining growth absent external investment.

Outlook: Evaluating Feasibility Amid Funding Imperatives

Looking ahead, Seres confronts critical inflection points hinging principally on funding ongoing developments without which operational continuity is jeopardized [S1][S2][F1]. While SER-155 addresses a high unmet medical need niche among allo-HSCT patients—a population underserved therapeutically—the pathway remains fraught with developmental risk typical for pioneering live biotherapeutics involving complex host-microbe interactions.

Success depends on achievement of meaningful clinical milestones validating safety/efficacy; timely enrollment/completion of phase trials; negotiation of strategic collaborations aiding trial conduct/manufacturing scale-up plus commercialization; regulatory approvals navigating evolving agency safeguards specific to microbiome-derived drugs; plus effective management of manufacturing integrity via third parties under cGMP compliance frameworks.

Due diligence should focus sharply on upcoming quarterly reports detailing cash burn trends alongside announcements regarding partnerships or capital raises shaping funding runway beyond Q3 2026—the horizon delineated explicitly by management’s going concern disclosures [S1]. In absence of clear financing pathways accessible at reasonable terms, cost-cutting or wind-down scenarios could materialize.

Nonetheless if progression milestones are met indicating strong therapeutic signals coupled with successful strategic partnerships absorbing capital load risks while reinforcing technical capabilities—Seres may recover footing toward re-establishing value creation paths within specialized live microbiome drug sector landscapes increasingly appreciated by clinicians addressing immunocompromised patient ecosystems.

Disclaimer: This analysis is based solely on public information available as of March 12, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments