Syra Health Corp’s Integrated Healthcare Solutions Drive Mixed Growth Amid Financial Strain

The company expands digital and population health services but faces profitability and capital challenges.

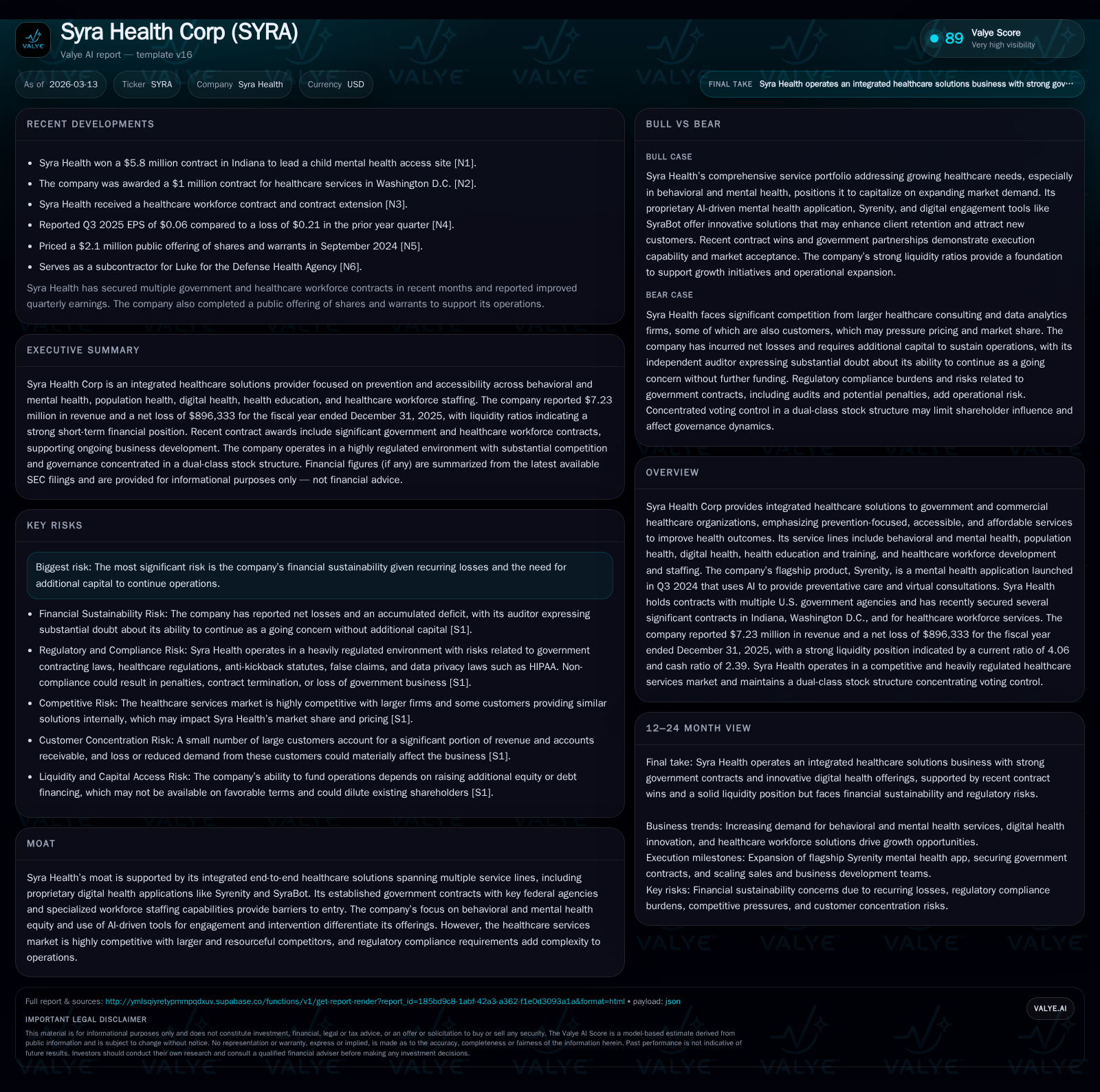

Syra Health Corp delivers multi-line integrated healthcare solutions focusing on behavioral, population, and digital health with an emphasis on mental health equity. Revenue modestly declined to $7.23 million in 2025 following prior growth, while losses narrowed significantly from 2024. The launch of the AI-driven Syrenity mental health app marks a key product milestone supported by government contracts. However, consistent operating losses, cash burn, and dependence on funding raise sustainability risks despite a solid liquidity position. Market competition and regulatory complexity compound operational challenges.

Company Overview and Historical Performance

Syra Health Corp operates as a comprehensive healthcare solutions provider targeting government and commercial sectors. Its approach emphasizes prevention-focused care making healthcare accessible and affordable across multiple service lines: behavioral and mental health, population health management, digital health innovation, health education/training, and workforce development/staffing [S1][S13].

Financially, Syra displayed a peak followed by a slight revenue contraction over recent years. Revenue grew from $5.52 million in FY2023 to $7.98 million in FY2024 (+44.7%) but then declined approximately 9.5% to $7.23 million in FY2025 [F1]. This deceleration may reflect market headwinds or contract variability.

Despite top-line growth until 2024, the company sustained losses annually though net losses have sharply narrowed—from $3.76 million net loss in FY2024 down to $896K in FY2025 [F1]. Operating income improved correspondingly from –$3.76 million (FY24) to –$0.9 million (FY25). This trend indicates improving cost controls or operational efficiencies but profitability remains elusive.

Cash flow from operations continues negative at –$447K in 2025 though this represents an improvement versus prior years’ deeper cash burns (–$2.93M in FY24) [F1]. Capex spending dropped sharply to just $107 in 2025 from thousands before highlighting cautious investment or a shift toward operating leverage.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 7 | -1 | 0 | -1 | -9.5% | +76.2% |

| 2024 | 8 | -4 | -3 | -4 | +44.7% | -27.9% |

| 2023 | 6 | -3 | -3 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | -42.7 |

| 2024 | -3 | -130.6 |

| 2023 | -3 | -73.2 |

Source: SEC companyfacts cache [F1].

*FY24 net loss grew less negative than FY23; percentages approximate.

Business Lines and Market Positioning

Behavioral & Mental Health

Mental health demand outpaces available resources globally—a gap Syra targets through digital equity-based interventions. Their flagship offering Syrenity launched Q3-2024 is a notable strategic asset: it leverages AI-driven user diaries for engagement alongside cognitive behavioral therapy modules delivered virtually [S13]. Syrenity enhances prevention access by enabling appointments with licensed professionals remotely while addressing treatment gaps caused by provider shortages.

Population Health Management

Syra provides data analytics integrating social determinants of health to stratify patient risk profiles and optimize resource allocation [S17]. Their epidemiological expertise supports quality care improvements across client populations involving government entities and large employers.

Digital Health Platform Solutions

Beyond Syrenity, the company develops complementary digital tools such as SyraBot—an AI-powered chatbot fostering continuous patient-provider engagement through automated support [S17]. These digital endeavors reflect broader industry trends emphasizing integrated telehealth capabilities.

Health Education and Workforce Development

Syra offers scalable medical training programs aimed at addressing workforce shortages exacerbated by demographic shifts within the U.S., including expanding their staffing solutions that serve governmental healthcare contracts [S17][S27].

Customers and Contractual Landscape

Government contracting constitutes a cornerstone of Syra’s revenue base encompassing federal departments such as HHS, NIH, CDC, NASA, DoD plus key state agencies like Indiana’s Family and Social Services Administration (FSSA) [S13][S15]. These relationships confer entry barriers but involve onerous compliance mandates subjecting Syra to audits and potential penalties if standards are unmet [S6][S10][S14].

However, a large degree of customer concentration poses risk; for instance Humana comprised around 37% of revenue in FY25 with FSSA divisions accounting for roughly 35%—a contraction from FSSA’s historic share over prior years [S15][F1]. Loss or reduction of demand from these clients could materially impact financials.

Industry Environment and Competitive Dynamics

The healthcare services sector is intensely competitive featuring entrenched incumbents with scale advantages alongside innovative startups in digital therapeutics and analytics platforms [S9][S14]. Regulatory scrutiny amplifies overhead as compliance with Anti-Kickback Statutes/FDA guidelines/HIPAA privacy rules demands robust internal frameworks which can disadvantage smaller players lacking resources [S18].

AI integration—while promising for engagement efficacy—introduces reputational risks due to unforeseen technical outcomes or regulatory uncertainty [S11]. Syra must balance innovation speeds against quality assurance.

Risks Overview

- Financial Sustainability: Operating losses persist despite improving margins; auditors flag going concern doubts absent fresh capital injections [S1][S14].

- Funding Requirements: Cash runway estimated at least one year based on current reserves ($1.6M); additional financing likely needed given recurring negative cash flows [F1][S10].

- Regulatory Compliance: Potential for governmental audits or contract terminations if regulatory adherence falters threatens access to lucrative public sector contracts [S6][S14].

- Customer Concentration: Heavy reliance on limited large clients magnifies revenue volatility risk if contracts are lost or renegotiated unfavorably [S15][S19].

- Technology Execution: Dependence on proprietary AI-driven apps entails risks related to intellectual property protection and possible adverse outcomes affecting reputation or legal liabilities [S11][S16].

- Market Competition: Larger competitors may outpace Syra’s innovation cycle; failure to upgrade solutions or adapt pricing could erode market share [S9][S14].

Capital Allocation and Returns

Given the early growth stage profile coupled with subscale revenues (~$7M) yet concentrated client base, the returns metrics remain subdued: FY25 reported an approximate negative ROE of –42.7%, reflective of net losses relative to ~$2M equity base [F1]. Free cash flow remains negative around –$448K.

No dividend payments or share repurchases have been documented indicating reinvestment focus or capital preservation aligned with growth objectives amidst fiscal constraints.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments