Bimini Capital Management Strengthens Profitability Through Strategic Agency MBS Focus

Focused investment in Agency Mortgage-Backed Securities supports Bimini's financial recovery, underpinned by disciplined capital management and governance.

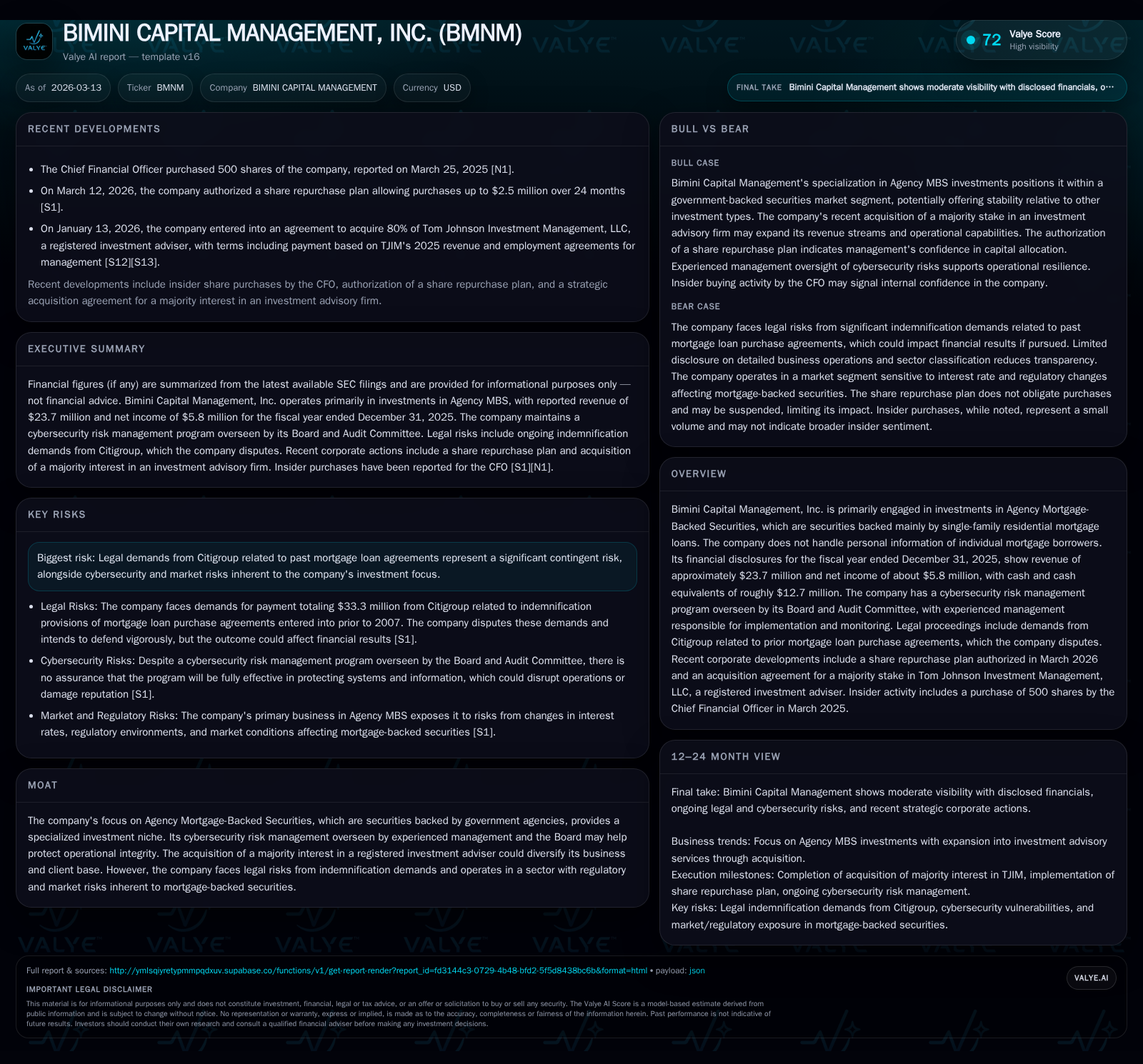

Bimini Capital Management, Inc. reported a significant financial turnaround in 2025 with revenues increasing nearly 22% to $23.7 million and net income recovering to $5.8 million from prior losses. The firm’s core strategy centers on managing Agency Mortgage-Backed Securities, providing stable revenue streams and reduced credit risk exposure. Despite ongoing legal challenges involving a $33.3 million indemnification dispute with Citigroup, Bimini maintains robust cybersecurity oversight and has authorized a $2.5 million share repurchase plan, signaling confidence in its intrinsic value. The recent acquisition of an 80% interest in Tom Johnson Investment Management aims to diversify the company’s growth avenues beyond mortgage securities.

Core Business Focus: Agency Mortgage-Backed Securities

Bimini Capital Management concentrates on investments in Agency Mortgage-Backed Securities (MBS), which are backed by U.S. government agencies such as Ginnie Mae, Fannie Mae, or Freddie Mac [S1][S8]. These securities primarily consist of single-family residential mortgage loans with credit risk mitigated by agency guarantees, limiting exposure to borrower defaults and enhancing portfolio stability.

This focus provides predictable cash flows supported by robust secondary market liquidity, enabling Bimini to manage interest rate risks effectively within its asset portfolio [S1][S8]. The company does not handle personal borrower information given its investment-centric operations.

Financial Performance: Significant Turnaround in Fiscal Year 2025

Bimini achieved a notable financial recovery in FY2025 following several years of net losses. Revenues increased by 21.9% year-over-year to approximately $23.7 million, while net income swung positively to roughly $5.8 million compared to losses in prior years [F1]. This represents a substantial improvement from net losses of -$1.3 million in FY2024 and deeper losses in earlier years.

Operating cash flow was positive at $2.9 million for FY2025, slightly down (-9.7%) from the previous year’s $3.2 million but maintaining healthy cash generation capacity [F1]. Capital expenditures remained negligible consistent with Bimini's asset-light model [F1]. Equity capital rose significantly from about $6.8 million at the end of 2024 to over $12.6 million as of December 31, 2025, reflecting retained earnings accumulation [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 24 | 6 | 3 | +21.9% | +544.1% | |

| 2024 | 19 | -1 | 3 | +8.4% | +67.2% | |

| 2023 | 18 | -4 | 2 | 0 | +11.0% | +79.9% |

| 2022 | 16 | -20 | 5 | 46176 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 46.0 | |

| 2024 | 0 | -19.2 | |

| 2023 | 13133 | 2 | -49.0 |

| 2022 | 1052666 | 5 | -163.5 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance (FY2022–FY2025)

Legal Risk: Citigroup Indemnification Dispute

Bimini faces a contingent legal claim from Citigroup totaling approximately $33.3 million related to indemnification provisions under mortgage loan purchase agreements predating Royal Palm’s mortgage origination cessation in 2007 [S1][S4]. The company disputes these demands and intends to defend vigorously if litigation ensues.

No accrual or provision has been recorded for this claim in the financial statements, reflecting management's assessment that the liability remains contingent without current recognition [S1][S4]. This dispute represents a material legal risk relative to Bimini's equity base.

Cybersecurity Governance

Cybersecurity oversight is managed by Bimini’s Audit Committee and Board of Directors, with periodic reviews addressing risk exposure pertinent to its operating model [S1][S9][S10]. Experienced executives lead implementation of policies designed for prevention, detection, mitigation, and response aligned with industry standards.

Given the firm's investment focus without direct borrower data handling, cybersecurity measures emphasize protecting proprietary systems and information critical to operational integrity.

Capital Structure and Liquidity Position

As of December 31, 2025, Bimini held approximately $12.7 million in cash and equivalents providing liquidity cushions supportive of operational needs and strategic initiatives [F1][S5][S11][S12]. The equity base strengthened markedly over the prior year due to improved profitability and retained earnings accumulation [F1].

The company maintains a conservative leverage profile with no significant debt increases disclosed recently [S5]. Enhancements to shareholder rights agreements further protect investor interests [S19].

Share Repurchase Authorization

On March 12, 2026, Bimini's Board authorized a share repurchase plan allowing up to $2.5 million aggregate purchases of Class A Common Stock over two years under Rule 10b5-1 plans [S3][S16]. No repurchases were executed during FY2025.

This program signals management confidence in the company’s valuation and reflects prudent capital allocation aligned with generating shareholder value when excess liquidity is available.

Acquisition Expands Diversification into Fee-Based Management

In January 2026, Bimini agreed to acquire an eighty percent ownership stake in Tom Johnson Investment Management (TJIM), a registered investment adviser [S25][S26]. The purchase price is structured as a multiple (2.5x) of TJIM's fiscal year revenue with deferred payments subject to performance conditions including EBITDA margin targets.

This acquisition diversifies Bimini’s revenue base beyond Agency MBS investments towards fee-based asset management revenues potentially reducing reliance on mortgage market cycles.

Outlook and Monitoring Points

Key areas for ongoing observation include:

- Resolution status of the Citigroup indemnification claims impacting contingent liabilities;

- Integration progress and financial contribution from TJIM acquisition;

- Sensitivity of Agency MBS portfolios to changes in interest rates affecting prepayment speeds and spreads;

- Future financial results confirming sustainability of profitability improvements;

- Capital deployment decisions including potential share repurchases or dividend declarations.

This analysis is based exclusively on publicly filed SEC disclosures through March 13, 2026, supplemented by Valye News research summaries.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments