FibroBiologics Advances Fibroblast-Based Therapy Amid Clinical Risks and Nasdaq Compliance Challenges

FibroBiologics, a clinical-stage biotech focused on fibroblast cell therapeutics, navigates research milestones and liquidity constraints while addressing Nasdaq listing compliance.

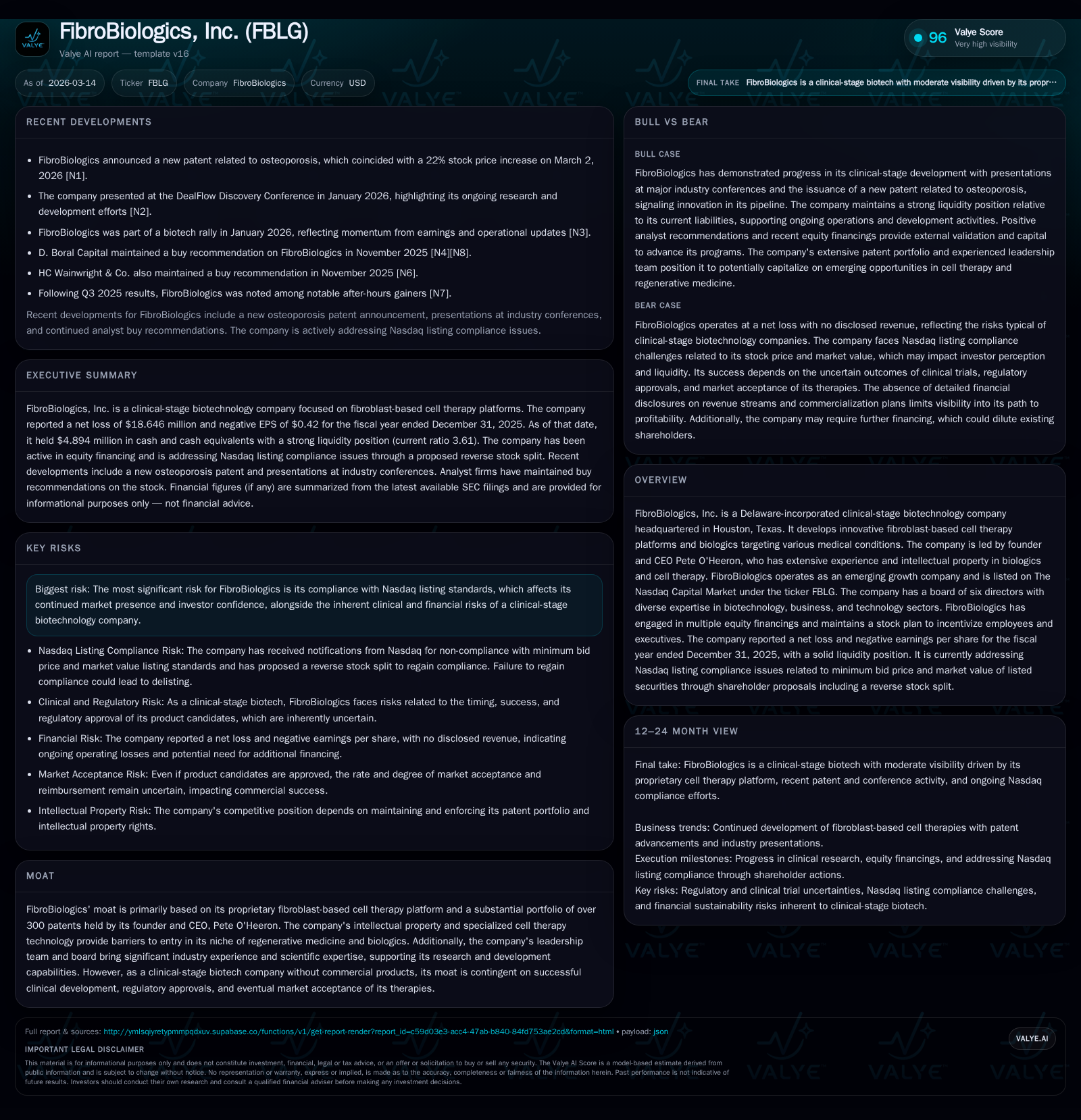

FibroBiologics, Inc. operates as a clinical-stage biotechnology firm specializing in innovative fibroblast-based cell therapy platforms targeting multiple medical conditions. Its growth trajectory has been fueled by intellectual property and equity financings but constrained by net losses and regulatory hurdles, including risks of Nasdaq delisting due to its stock price. Recent patent grants bolster its pipeline prospects. The company faces typical biotech development risks alongside significant near-term liquidity needs and capital structure complexities. Close scrutiny of upcoming clinical trial results, regulatory submissions, and Nasdaq compliance efforts will be critical to its evolution.

Company Overview

FibroBiologics, Inc., headquartered in Houston, Texas, is a Delaware-incorporated clinical-stage biotechnology company focused on developing fibroblast-based cell therapy platforms and biologics targeting various medical conditions . The company is led by founder and CEO Pete O’Heeron who holds extensive intellectual property—over 300 patents—and experience in biologics and cell therapy. Despite its nascent stage without approved commercial products, FibroBiologics positions its fibroblast technology as the core moat fostering entry barriers within regenerative medicine.

Historical Financial Performance

FibroBiologics' financials reflect typical challenges facing clinical-stage biotechs with increased R&D expenses and no revenue streams yet from marketed therapies. As summarized below from latest available SEC filings and company facts XBRL data [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | -16 | -17 | 262000 | -67.1% |

| 2024 | -11 | -12 | -14 | 184000 | +32.3% |

| 2023 | -16 | -6 | -9 | 495000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -17 | -302.9 |

| 2024 | -12 | -408.1 |

| 2023 | -7 | -1315.6 |

Source: SEC companyfacts cache [F1].

Operating income steadily declined reflecting increased R&D outlays toward advancing cell therapy candidates through preclinical and clinical stages. Negative net income significantly deepened in FY2025 versus FY2024 due both to operational expenses and higher operational burn.

Operating cash flows remained negative due to fundamental lack of earnings; the company's free cash flow (operating cash flow minus capex) was approximately negative $16.7 million in the latest fiscal year [F1]. Equity improved somewhat due to capital raises but remains modest relative to accumulated deficits.

Growth Prospects

FibroBiologics' future growth hinges primarily on successful advancement of its fibroblast platform across multiple indications:

- Recent issuance of a patent covering osteoporosis treatment highlights expanding IP coverage and potential indication diversification [N1]. This signals strategic efforts toward musculoskeletal regenerative disorders where fibroblast-mediated tissue repair might prove transformative.

- The platform's flexibility allows targeting internal injuries or autoimmune conditions by modulating fibroblast activity.

- Proprietary technology underpinned by CEO O’Heeron’s patented innovations provides differentiation amid competitive regenerative medicine landscape.

However, these prospects are constrained by typical clinical-stage biotech realities:

- No approved products; all candidates in early development requiring extensive trials and regulatory approval.

- Market acceptance of cell therapy approaches remains evolving with reimbursement and pricing unknowns.

- Ongoing need for substantial financing amid costly R&D without revenue until commercialization.

Capital Allocation and Financial Strategy

FibroBiologics has raised funds principally through equity offerings complemented by issuance of preferred stock and warrants:

- During late 2025 into early 2026 periods there were several registered direct offerings raising roughly $1.5–$1.7 million per transaction plus concurrent private placements with attached warrants exercisable at prices around $0.33 per share [S15,S22,S26,S27].

- The company has no debt outstanding as older convertible notes were converted into equity by mid-2023 [S5,S6].

- Cash balance stood at approximately $4.9 million as of December 31st, 2025 providing limited runway given negative operating cash flow trends [F1,S1].

- No cash dividends or share repurchases have occurred; instead capital allocation prioritizes funding clinical programs along with employee equity incentives via the approved 2022 Stock Plan with about 6.8 million shares reserved for issuance [S7,S23].

This equity-heavy financing approach is consistent with early-stage biotech norms where shareholder dilution is a tradeoff for continued funding R&D progress.

Management and Governance

The leadership team brings specialized scientific expertise centered on CEO Pete O’Heeron’s role as the technology originator holding key patents driving platform value creation. The board includes six directors with diverse backgrounds spanning biotechnology innovation and business strategy which support governance decisions including overseeing compliance with Nasdaq listing requirements.

In terms of executive compensation aligned with growth objectives:

- Recent salary adjustment for CFO Jason Davis effective January 2026 was announced reflecting expanded responsibilities associated with capital management under challenging market conditions [S3].

- Stock option grants are used extensively for key executives incentivizing contributions toward clinical milestones and company success [S28,S29].

Regulatory Compliance Risk: Nasdaq Listing Concern

A prominent near-term risk arises from non-compliance with Nasdaq minimum bid price rule (below $1 threshold over requisite time period), which places FibroBiologics at risk of delisting from The Nasdaq Capital Market:

- The company received notices beginning July 2025 of non-compliance; subsequent actions include filing proxy materials proposing a reverse stock split (between ratios of 1-for-5 to 1-for-30) aimed at restoring compliance through adjusted trading price levels [S18,S19].

- A hearing request has been filed contesting imminent delisting measures while actively monitoring share price recovery options.

This compliance challenge adds market uncertainty impacting investor confidence though management intends proactive engagement to address it.

Industry Context (Analysis)

Fibroblast-based therapies form an emerging niche within cell therapy focused on tissue regeneration distinct from more established hematopoietic or mesenchymal stem cells platforms. Success depends on overcoming challenges related to delivery mechanisms, immunogenicity control, manufacturing scale-up complexities given living-cell therapeutics' bespoke nature.

Patents protecting manufacturing processes and targeted biological pathways provide defensibility but require sustained innovation pace ahead of generics or alternate regenerative solutions entering the field.

What To Watch Forward (Analysis)

Key developments will include:

- Clinical trial progression benchmarks including initiation/completion dates and initial efficacy/safety readouts,

- Regulatory milestone filings such as IND submissions or requests for Fast Track designation,

- Outcomes from Nasdaq compliance hearings including any granted extensions or reverse split implementation details,

- Progression in expanding IP portfolio particularly into new indications like osteoporosis where recent patents suggest pipeline depth,

- Additional financing rounds or collaborations signaling capital availability amidst persistent negative cash flow profiles.

Summary

FibroBiologics exemplifies an innovative but inherently high-risk clinical-stage biotech endeavor propelled by unique fibroblast-centered technology protected via robust patent holdings from its visionary founder CEO. Operating losses have expanded rapidly reflecting intensified developmental expenditures without offsetting revenues yet. Its balance sheet shows finite liquidity buffered somewhat by multiple equity fundraises but requires vigilant capital management.

Nasdaq listing challenges necessitate structural stock actions adding complexity atop scientific risks inherent in pioneering cell therapies whose commercial viability remains speculative pending regulatory validation.

Investors should maintain focus on execution across the clinical development timeline coupled with corporate governance navigating market standard compliance thresholds that could affect tradability within the public markets.

This report is prepared solely for informational purposes based on available regulatory filings and news disclosures as of March 14th, 2026. It does not constitute investment advice or a recommendation to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments