Oruka Therapeutics’ Clinical Progress and Capital Strain Shape Near-Term Outlook

The clinical-stage biopharma company evolves post-merger with advanced antibody drugs targeting psoriasis, facing growing losses amid trial progression.

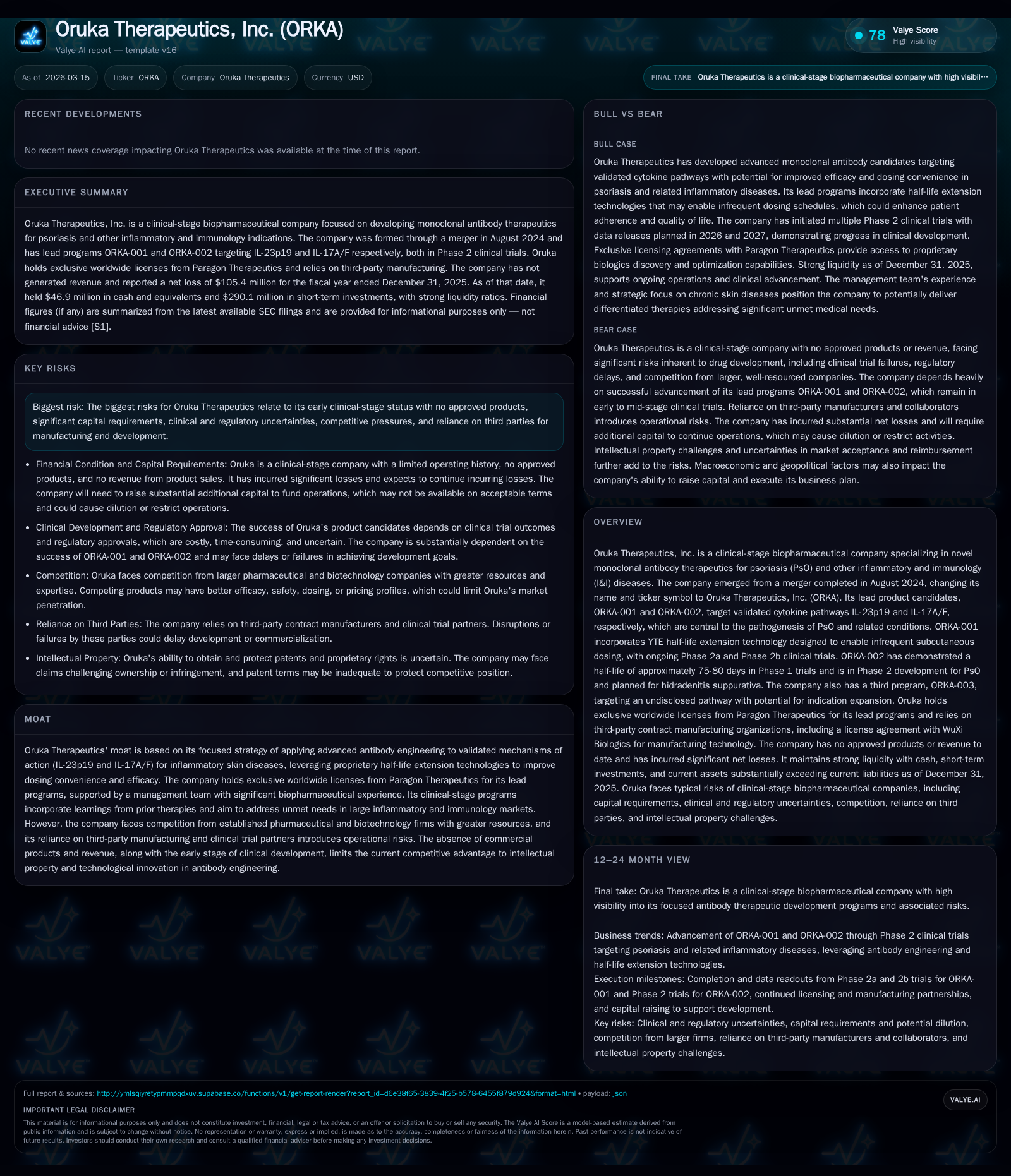

Oruka Therapeutics, Inc. emerged in 2024 from a merger and focuses on monoclonal antibodies for psoriasis and related inflammatory diseases. Despite no revenues as of 2025 year-end, it advanced lead candidates ORKA-001 and ORKA-002 through Phase 2 development leveraging proprietary half-life extension technologies. Operating losses deepened to $122 million in 2025 with negative cash flows reflective of ongoing clinical investments and limited capital returns. Key risks include regulatory uncertainties, competitive pressures, and sustained capital needs as the company aims to demonstrate clinical proof points while preparing for potential commercialization.

Company History and Strategic Focus

Oruka Therapeutics, Inc. emerged as a combined entity in August 2024 from a merger involving ARCA biopharma, Inc. and the then Pre-Merger Oruka Therapeutics. This strategic consolidation created a clinical-stage biopharmaceutical company focusing on novel monoclonal antibody therapeutics targeting psoriasis (PsO) and other inflammatory and immunology (I&I) diseases. The new corporate name reflects its mission centered on skin restoration therapies addressing chronic conditions that impact patient quality of life [S1].

The company’s lead assets—ORKA-001 and ORKA-002—target well-validated immune pathways: IL-23p19 and IL-17A/F respectively, both critical cytokines playing central roles in psoriatic disease pathogenesis. These programs leverage proprietary half-life extension technologies designed to enable infrequent subcutaneous dosing schedules to improve patient adherence and convenience compared to existing biologics [S1], reflecting an industry trend toward optimized dosing regimens without sacrificing efficacy.

Historic Financial Performance

As a clinical-stage biotech without commercial products as of yet, Oruka Therapeutics has no revenue-generating operations. It has incurred increasing operating losses consistent with advancing clinical development efforts:

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -105 | -88 | -122 | -25.9% | |

| 2024 | -84 | -58 | -88 | -1468.2% | |

| 2023 | 0 | -5 | -5 | -7 | +46.2% |

| 2022 | 0 | -10 | -11 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -88 | -22.3 |

| 2024 | -58 | -21.9 |

| 2023 | -5 | -14.4 |

| 2022 | -11 | -23.8 |

Source: SEC companyfacts cache [F1].

Operating income deteriorated significantly year-over-year by approximately 38.5%, driven largely by increased R&D spending related to clinical trials [F1]. Net losses also expanded by roughly 25.9%, reflecting the company's continued investment phase.

Operating cash flow remained deeply negative at $88 million in fiscal year ending December 31, 2025, signaling substantial cash burn consistent with ongoing clinical development activities [F1]. Capital expenditures are minimal relative to operational expenses.

Liquidity is supported by a robust current ratio of approximately 22x at year-end 2025 due to sizable current assets including cash equivalents totaling about $47 million [F1]. Return on equity is negative at about -22%, typical for early-stage biopharmaceutical companies yet to generate earnings [F1].

Pipeline Overview and Growth Prospects

ORKA-001 targets the IL-23p19 subunit involved in psoriasis pathogenesis with proprietary half-life extension technology aimed at enabling less frequent dosing schedules compared to existing treatments [S1]. The program is in Phase 2a/b clinical development.

ORKA-002 targets the IL-17A/F heterodimer implicated across multiple inflammatory conditions including psoriasis (PsO), hidradenitis suppurativa (HS), and psoriatic arthritis (PsA). Phase 1 data showed promising pharmacokinetics consistent with extended half-life supporting infrequent administration [S1]. This candidate is progressing through Phase 2 trials.

An additional preclinical program focused on pathogenic tissue-resident memory T cells (TRMs) aims at potential disease modification beyond symptomatic treatment but remains early stage [S1].

The company’s growth hinges on successful execution of these pipeline milestones including pivotal Phase 2 data readouts and subsequent regulatory submissions in sizable dermatology/immunology markets.

Upcoming Milestones & What to Watch For

While no explicit forward guidance is provided [S2], investors should monitor:

- Release of Phase 2 efficacy data for ORKA-001 measuring key endpoints such as Psoriasis Area Severity Index (PASI).

- Progression timelines for ORKA-002 Phase 2 studies in psoriasis as well as planned expansion into HS indications.

- Potential strategic partnerships or collaborations that could provide additional funding or commercialization support.

- Scalability efforts regarding third-party manufacturing relationships critical for supply chain continuity.

These developments will be important indicators of the company’s ability to advance its novel antibody formats amidst competitive pressures.

Risk Landscape

Oruka faces several inherent risks typical of early-stage biopharmaceutical developers:

- Regulatory approval uncertainty inherent in drug development requiring extensive safety and efficacy demonstration [S1–S6].

- Competitive challenges from established biologic therapies targeting similar pathways with proven track records.

- Intellectual property risks including patent disputes or failure to secure comprehensive protection despite provisional filings handled by Paragon Therapeutics [S15,S19].

- Dependence on third-party contract manufacturing organizations introduces operational risks related to quality control and supply disruptions.

- Exposure to global healthcare regulatory environments imposing pricing controls or reimbursement limitations that may affect future revenues [S4,S14].

- Product liability exposure remains a concern although currently insured against known risks [S16].

Capital Allocation & Returns Profile

With no revenue generation or plans for dividends/share repurchases given its developmental stage, Oruka allocates capital primarily toward research and development activities supporting pipeline advancement.

Financial metrics reflect this focus: approximate return on equity stands near -22% due to net losses against shareholder equity invested [F1]. Free cash flow remains deeply negative owing to significant operational cash outflows vastly exceeding minimal capital expenditures.

Equity base has grown substantially following the merger and associated financing activities—from approximately $37 million in FY2023 to nearly $472 million by FY2025—highlighting investor capital infusion supporting the company’s expansion phase [F1]. Dilution risk persists until commercial viability is demonstrated.

Industry Context (Analysis)

In dermatology-focused immunology drug development, extending antibody half-lives while maintaining safety profiles is critical due to the chronic nature of diseases like psoriasis requiring long-term therapy adherence. Oruka’s emphasis on YTE-based half-life extension aligns with sector trends aiming for differentiated treatment regimens that reduce injection frequency—a key factor for improved patient compliance versus standard biweekly or monthly dosing used by incumbents.

Commercial barriers remain significant due to entrenched products commanding broad formulary coverage backed by insurers worldwide. New entrants must demonstrate not only comparable efficacy/safety but also clear advantages in dosing convenience or cost-effectiveness.

Conclusion

Oruka Therapeutics stands at a pivotal juncture following its August 2024 merger creating a focused clinical-stage biotech competing in the lucrative inflammatory skin disease segment via innovative monoclonal antibodies enhanced with half-life extension technology. Although financially stressed due to high cash burn rates typical of early-stage development companies—with liquidity adequate near term—the company’s near-term value depends heavily on successful advancement of lead candidates through mid-stage trials amid intense competition and regulatory complexities.

Upcoming clinical data releases will be critical signals validating Oruka’s technology platform potential to disrupt existing treatment paradigms and justify further capital deployment toward commercialization readiness.

Disclaimer: This analysis is based exclusively on publicly available information including recent SEC filings up to March 2026 ([F1], [S#]) without predictions or investment advice. Readers should conduct independent due diligence before making decisions related to Oruka Therapeutics or its securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments