KLX Energy Services Holdings Stakes Out Growth with Proprietary Tech in U.S. Oilfield Services

KLX Energy Services develops a technically focused oilfield services platform leveraging regional scale and proprietary technologies amid cyclical sector challenges.

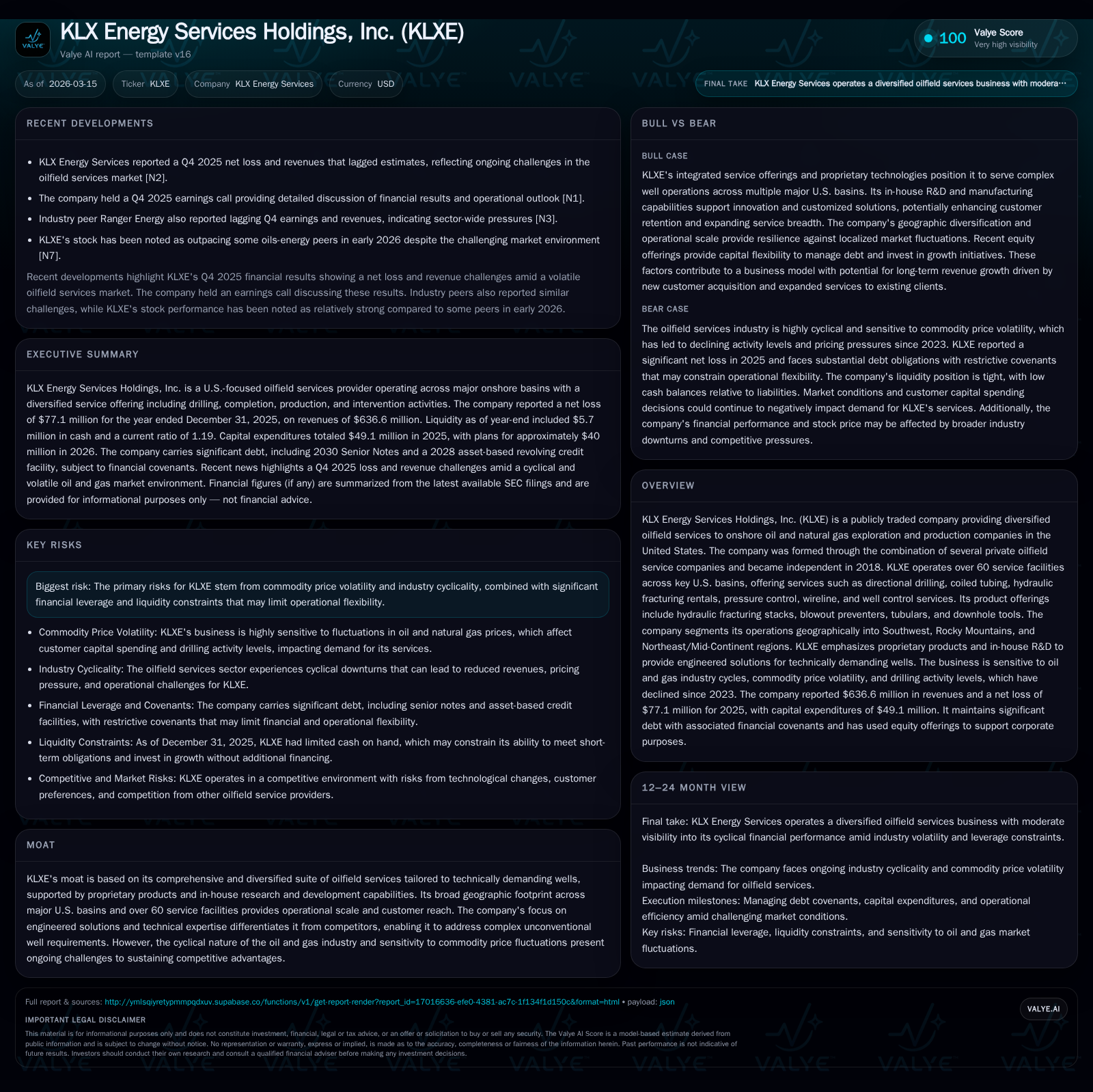

Since its 2018 spin-off, KLX Energy Services Holdings (KLXE) has built a diversified oilfield services business centered on engineered solutions for unconventional wells across major U.S. basins. The company blends proprietary product innovation with over 60 geographically dispersed service sites to address complex drilling and completion demands. While revenues and operating cash flow contracted in 2025 due to lower customer activity, KLXE’s March 2025 refinancing extended maturities but introduced high-interest debt with restrictive covenants limiting capital return flexibility. Going forward, growth depends on expanding engineered solutions and navigating commodity-driven cyclicality alongside financial leverage constraints.

Evolution from Private Consolidation to a Public Oilfield Service Specialist

KLX Energy Services Holdings originated from the aggregation of seven private oilfield service companies acquired during 2013 and 2014, each initially serving distinct regional niches with select capabilities. Incorporated in Delaware in mid-2018, KLXE spun off from KLX Inc. later that year to become an independent publicly traded entity [S1]. The company further consolidated its platform with acquisitions including Quintana Energy Services Inc. in 2020 and Greene's Energy Group LLC in 2023 [S1].

This strategic evolution underpins KLXE’s positioning as a technically differentiated oilfield service specialist focusing on integrated engineered solutions tailored for complex unconventional wells. Its growth-oriented strategy targets expanding the breadth of services offered to both new and existing customers by harnessing its in-house R&D capabilities.

Revenue and Cash Flow Trends Reflecting Shifts in the U.S. Onshore E&P Market

While explicit multi-year numeric revenue data is not fully detailed in filings, disclosures note KLXE experienced a significant contraction in revenue and operating cash flow during fiscal year 2025 relative to 2024 [N2][S15]. Operating cash flow dropped sharply to $7.5 million in 2025 from $54.2 million the prior year, illustrating weakened market demand [S15]. Capital expenditures also declined from $65.1 million in 2024 to $49.1 million in 2025, reflecting prudent spending aligned with reduced activity [S10].

Operating income pressures mirror broader cyclicality affecting US onshore drilling and completion markets where capital spending has softened due to commodity price fluctuations [N2]. The downturn impacted all geographic operating segments as per disclosures [S1].

| Fiscal Year | Operating Cash Flow | Capital Expenditures |

|---|---|---|

| 2024 | $54.2M | $65.1M |

| 2025 | $7.5M | $49.1M |

Revenues are not explicitly quantified; CFO and Capex shown per SEC filings.

Proprietary Products and In-house R&D as Engines of Technical Differentiation

A central pillar of KLXE’s competitive positioning is its proprietary product suite supported by internal R&D that underpins manufacturing, repair, and maintenance capabilities [S1]. Key offerings include hydraulic fracturing stacks, blowout preventers, tubulars, downhole tools, as well as dissolvable plugs designed for complex well architectures.

These engineered products enable customers to optimize unconventional well completions involving extended reach horizontals with intense completion stages — scenarios prone to higher risks of non-productive time (NPT). By integrating advanced technical innovations with field expertise, KLXE aims to reduce NPT through improved pressure control systems and custom tool designs.

This differentiation aligns closely with ongoing customer demand for tailored solutions enabling more efficient stimulation programs under evolving geological challenges [S24].

Geographic Segment Performance Highlights and Regional Demand Drivers

KLXE operates across three main regions covering major U.S. basins:

- Southwest Region: Permian Basin and Eagle Ford plays.

- Rocky Mountains Region: Bakken/Williston plus smaller basins such as DJ and Uinta.

- Northeast/Mid-Continent Region: Marcellus/Utica shale gas plays plus Mid-Continent STACK/SCOOP.

This regional footprint facilitates adaptation of technical service offerings tailored for specific basin geologies and operator preferences [S1][S17]. For example, the Southwest segment driven by the Permian requires high-intensity frac fleets supported by durable proprietary stacked rental equipment while the Northeast focuses more on coiled tubing interventions aligned with gas production optimization.

Performance across these regions fluctuates according to localized E&P activity driven by commodity cycles and operator capital allocation decisions impacting completion volumes.

Capital Structure Refinancing: High-Interest Debt with Restrictive Covenants

In March 2025, KLXE completed a refinancing replacing its maturing $235 million Senior Notes due 2025 with approximately $244 million senior secured notes due March 2030 bearing a floating interest rate linked to Term SOFR plus margin resulting in an effective annual rate around 12.3% [S4][S6][S7]. Concurrently, it entered into a $125 million asset-based revolving credit facility incorporating a first-in-last-out tranche providing liquidity support [S6][S8].

The new indenture imposes stringent covenants restricting dividend payments, incurrence of additional indebtedness beyond permitted amounts (up to approximately $150 million within twelve months post-refinancing), asset sales without lender consent, affiliate transactions among other limitations designed to protect collateral value [S12][S13].

Cross-acceleration clauses mean default under one agreement could accelerate debt repayment obligations across related instruments potentially impairing liquidity [S12]. As of December 31, 2025, total net debt approximated $258 million after amortizations [S6][S21]. This restructuring lengthened maturity profiles but increased borrowing costs reflecting sector risk perceptions.

Liquidity Position, Cash Flow Generation, and Capital Allocation Priorities

Cash balances fell markedly—from $91.6 million at end-2024 down to $5.7 million at end-2025—driven by financing outflows related to refinancing ($60.5 million net cash used) and investing activities ($32.9 million net cash used), partially offset by modest operating inflows totaling $7.5 million during full-year 2025 [S15][S16][S21]. Liquidity is supplemented by the ABL Facility which had approximately $39.9 million borrowing availability as of late Q4/25 [S8][S10].

Capital expenditure guidance indicates moderation toward roughly $40 million for fiscal year 2026 focused primarily on sustaining operations rather than expansionary investments [N1][S10]. Given elevated leverage combined with covenant restrictions curtailing dividends or share buybacks ([S12][N2]), shareholder returns have been limited.

Consequently, capital allocation prioritizes debt service resilience over immediate returns while maintaining operational stability amid softer market conditions.

Risk Factors: Commodity Cyclicality, Indebtedness, and Contractual Restrictions

KLXE’s revenues remain tightly correlated with upstream E&P activity heavily influenced by commodity price volatility—this cyclicality pressures utilization rates for hydraulic fracturing rentals and related services [N2][S18]. The company’s substantial indebtedness constrains financial flexibility especially under covenant frameworks mandating deleveraging targets stepping down over coming years (maximum leverage ratios declining from approximately 4.50x toward about 2.50x net leverage) [S12][S13].

Covenant breaches could trigger accelerated debt repayment or lien enforcement adversely affecting liquidity during downturns.

Additionally indemnity obligations tied to facility leases or acquisition agreements carry contingent liabilities that are not material currently but represent managed risks without precise quantification on the balance sheet [S23]. These factors underscore the challenge of balancing investment in proprietary technology development while managing leverage through cyclical industry headwinds.

Outlook: Market Dynamics and Milestones To Monitor

Explicit forward-looking financial guidance remains limited; near-term outlook will depend on basin-level activity recovery trajectories combined with operator willingness to invest in completions testing advanced engineering solutions highlighted by KLXE’s proprietary portfolio [N1][N2]. Key milestones include backlog growth signaling renewed demand for hydraulic fracturing stacks or dissolvable plug tools as well as integration success metrics tied to recent acquisitions like Greene's Energy Group.

Monitoring compliance with debt covenants such as fixed charge coverage ratio tests under the ABL facility will be critical indicators of financial health or stress revealing liquidity posture changes.

The macroeconomic environment remains uncertain given variables influencing commodity prices alongside regulatory developments affecting environmental compliance costs.

KLXE’s strategy—anchoring growth through combined scale across diverse geographies while leveraging R&D-driven technical differentiation—offers resilience potential if industry cycles improve moderately.

Disclaimer: This analysis is based solely on publicly available company filings and news sources up to March 15, 2026; it does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments