Smith & Nephew’s Expansion Through Portfolio Rationalization and Acquisition Integration

Smith & Nephew advances its 12-Point Plan by streamlining product lines and integrating Integrity Orthopaedics to drive growth and operational efficiency in 2025.

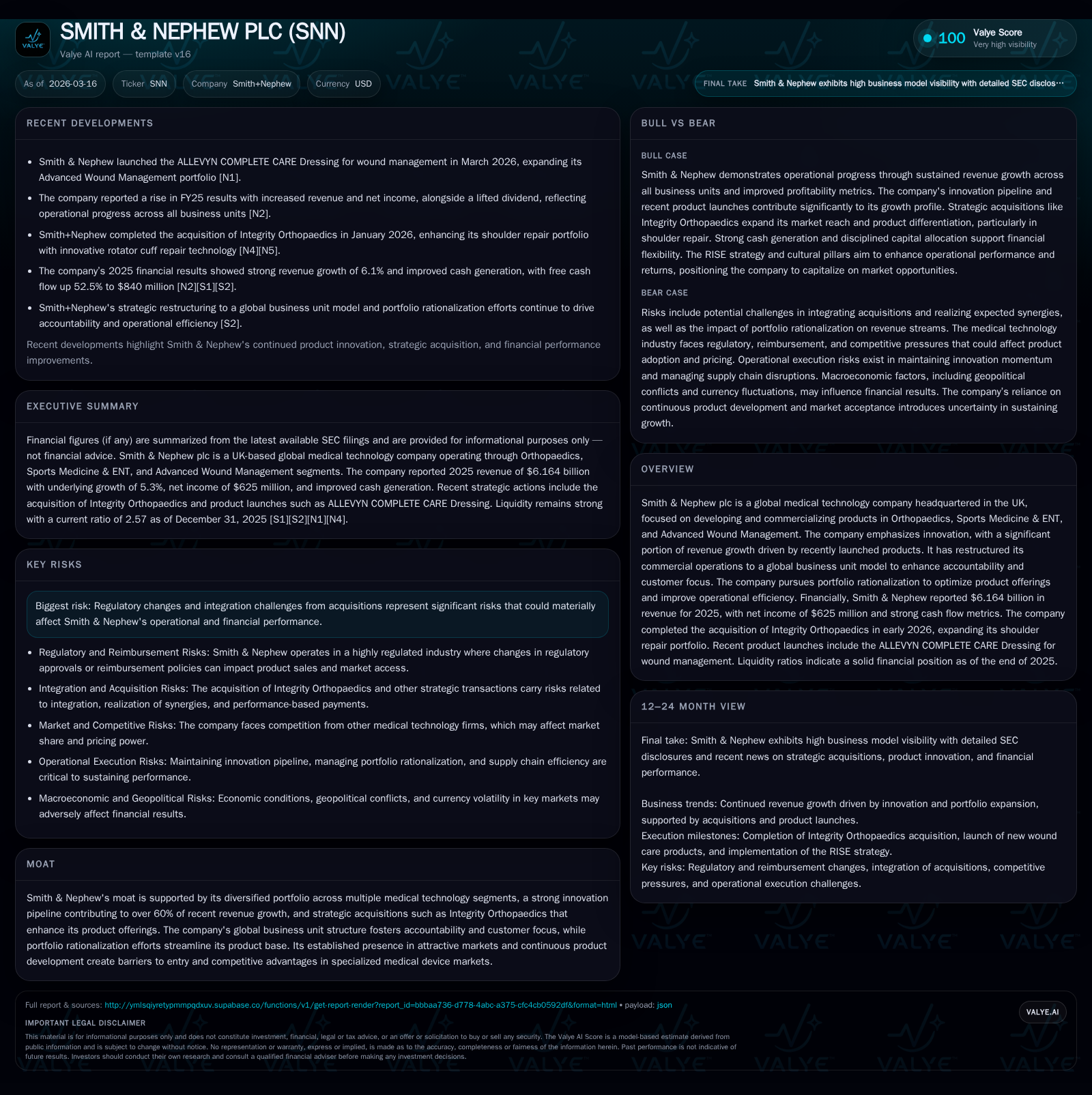

Smith & Nephew demonstrated robust financial momentum in 2025, achieving $6.16 billion in revenue and a 51.7% increase in net income supported by innovative product launches and operational restructuring. The company’s disciplined portfolio rationalization, particularly within Orthopaedics, alongside the acquisition of Integrity Orthopaedics, positions it for enhanced market penetration and margin expansion. Capital allocation remains balanced with meaningful dividends and share buybacks, while the commercial business restructuring fosters accountability and growth. Regulatory and integration risks persist, but the company’s innovation pipeline and strategic execution are key future catalysts.

Financial Momentum from Recent Years: The Path to $6.16B Revenue

Smith & Nephew closed FY25 with $6.164 billion in revenue, marking a 5.3% underlying growth rate that outpaced its guided target of around 5% [F1][S29]. This progression reflects successful execution of its 12-Point Plan aimed at fortifying the underperforming Orthopaedics segment while accelerating growth in Sports Medicine & ENT and Advanced Wound Management. The company’s net income surged by an impressive 51.7% year-over-year, reaching $625 million for FY25 compared to $412 million in FY24, signaling substantial margin improvement through operational discipline and cost control [F1].

Equity stood at approximately $5.29 billion at year-end, translating into a return on equity near 11.8%, underscoring the profitability gains commensurate with capital invested [F1]. The company also expanded trading profit margins by more than 200 basis points over recent years through improved pricing/mix dynamics and productivity savings embedded across its manufacturing network [S16][S24].

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 625 | +51.7% |

| 2024 | 412 | +56.7% |

| 2023 | 263 | +17.9% |

| 2022 | 223 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 330 | 11.8 |

| 2024 | 327 | 7.8 |

| 2023 | 327 | 5.0 |

| 2022 | 327 | 4.2 |

Source: SEC companyfacts cache [F1].

*Estimated revenues inferred from reported growth rates; net income and equity per [F1].

Innovation Pipeline Fueling Over 60% of Revenue Growth

Innovation remains a cornerstone of Smith & Nephew’s expansion strategy: over 60% of its underlying revenue growth in FY25 stemmed from products introduced within the last five years [N2][S19]. A notable example is the launch of the ALLEVYN COMPLETE CARE Dressing in Advanced Wound Management, which enhances clinical outcomes through superior moisture control and ease-of-use features tailored to evolving patient care settings [N2].

Orthopaedics saw revitalized momentum with new platforms designed to address surgeon preferences across knee and hip segments, incorporating personalization technologies and robotic enablement features detailed in the forthcoming LANDMARK Knee System launch slated for H2 2026 [S27][S29]. The Sports Medicine & ENT division sustained growth despite headwinds like the Volume-Based Procurement impact in China by focusing on high-margin products and expanding into ambulatory surgery settings.

The vitality of Smith & Nephew's innovation pipeline is reflected not only in accelerated time-to-market but also in lifecycle management practices that optimize portfolio value while balancing investments between incremental enhancements and breakthrough solutions—a critical competitive advantage amid rapid medical technology evolution.

Commercial Transformation: The Global Business Unit Model

In response to prior operational complexity, Smith & Nephew restructured its commercial operations around distinct global business units (GBUs): Orthopaedics, Sports Medicine & ENT, and Advanced Wound Management [S1]. This transition has embedded clearer profit-and-loss ownership within each GBU, prompting faster decision-making cycles and tighter alignment with customer needs across geographies.

This structural simplification replaces a matrix franchise-region setup with vertical teams accountable for all aspects from sales strategy through to customer engagement effectiveness. As a result, channel management has been optimized leading to improved organic growth prospects as sales forces can better prioritize high-impact accounts globally without regional friction.

Portfolio Rationalization and Integration of Integrity Orthopaedics

A pivotal element underpinning Smith & Nephew's transformation has been systematic portfolio rationalization—particularly visible within Orthopaedics—where the firm identified an initial 19 product families for phase-out mainly in knees and hips during early waves of pruning [S27]. In late 2025, this program intensified with approximately 50 additional families targeted predominantly in Trauma, aiming to trim SKU complexity by as much as 54% over three to five years.

Anticipated gross inventory reduction approximates $500 million mainly from eliminating lower-return or obsolete SKUs. This simplification bolsters capital efficiency while enhancing customer's ease-of-understanding product ranges, which is crucial for surgical instrumentation sets where tray efficiency translates directly into procedural cost savings.

Concurrently, Smith & Nephew integrated Integrity Orthopaedics early in 2026—an acquisition focused on augmenting its shoulder repair capabilities—which complements ongoing product rationalization by broadening therapeutic breadth within Sports Medicine platforms without diluting organizational focus or cannibalizing core orthopaedic lines [N1].

Capital Allocation Strategy: Dividends, Buybacks, and Investment

Smith & Nephew maintains a disciplined capital allocation framework balancing shareholder distributions against strategic reinvestment priorities [F1]. In FY25, dividend payouts edged up marginally to $330 million total reflecting confidence in sustainable cash flow generation amid growth investments.

Buyback programs accounted for approximately $502 million in treasury share purchases during 2025, demonstrating active efforts to enhance per-share metrics without compromising liquidity or debt capacity.

Free cash flow surged more than fifty percent from prior year levels reaching $840 million driven by strong operating cash conversion ratios above 100%—an indicator of tight working capital management especially through inventory reductions associated with portfolio pruning initiatives [S11][S15].

This approach supports sustained R&D funding essential for innovation continuity while ensuring capital returns align with shareholder expectations within mid-single digit payout ratios.

Operational Leverage and R&D Intensity Trends

Investment intensity remains robust as Smith & Nephew allocates capital towards capex expenditures estimated around $433 million annually aimed at manufacturing network optimization aligned with the ongoing portfolio rationalization program [S11].

R&D expenses are managed prudently relative to revenues but remain sizable given the company's commitment to maintaining leadership across diverse orthopedic technologies, wound care products, and minimally invasive surgical solutions.

Operational leverage effects have materialized through disciplined overhead allocations now directly charged to GBUs enhancing accountability accompanied by productivity savings that contributed significantly to margin expansions despite inflationary pressures including tariffs totaling approximately $17 million impact last year [S16][S20].

Risks: Regulatory Environment and Acquisition Complexities

Smith & Nephew faces inherent risks typical of the medical technology sector including evolving regulatory landscapes affecting device approvals, reimbursement frameworks particularly outside Western markets, as well as quality system compliance challenges which can trigger recalls or sanctions if not managed rigorously [S4][S7].

The acquisition integration process presents uncertainties related to realizing synergies timely without disrupting day-to-day operations or incurring excessive restructuring costs—a risk highlighted given the scope of the Integrity Orthopaedics deal alongside ongoing portfolio rationalization efforts.

Other sector-wide exposures include patent litigation threats common among device manufacturers along with geopolitical factors influencing cross-border supply chains impacting component availability or logistic cost structures.

What to Watch: Growth Catalysts and Milestones Ahead

Looking forward into FY26 and beyond under the newly announced RISE strategy framework designed to elevate Smith & Nephew’s performance trajectory across four pillars: reaching broader patient populations through differentiated products; accelerating innovation; scaling investments strategically; executing operationally with greater efficiency [S27], key areas merit close monitoring.

Particularly important will be rollout progress of major orthopedic platforms like LANDMARK Knee System expected H2 2026 launch offering integrated robotic compatibility emphasizing implant personalization. Success here could catalyze further market share gains notably within US knee implants where recovery remains pivotal.

Additionally, evaluation of ongoing portfolio rationalization progress—including phasing out remaining trauma-related families—and assimilation results following Integrity Orthopaedics acquisition will offer insight into sustainability of margin expansion trends.

Finally, vigilance over regulatory developments worldwide especially regarding device classification changes or coverage policies will influence product pipeline cadence impacting revenue realization timing.

Disclaimer: This analysis is based solely on information cited from publicly available SEC filings ([F1], [S#]) and news sources ([N#]) as of March 2026. It does not constitute investment advice or recommendations but aims to provide an informed overview grounded in disclosed company data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments