Lifeway Foods Innovates Through Niche Probiotic Dairy Expansion

Lifeway Foods leverages cultured dairy innovation and strategic capital investment to enhance profitability and operational capacity.

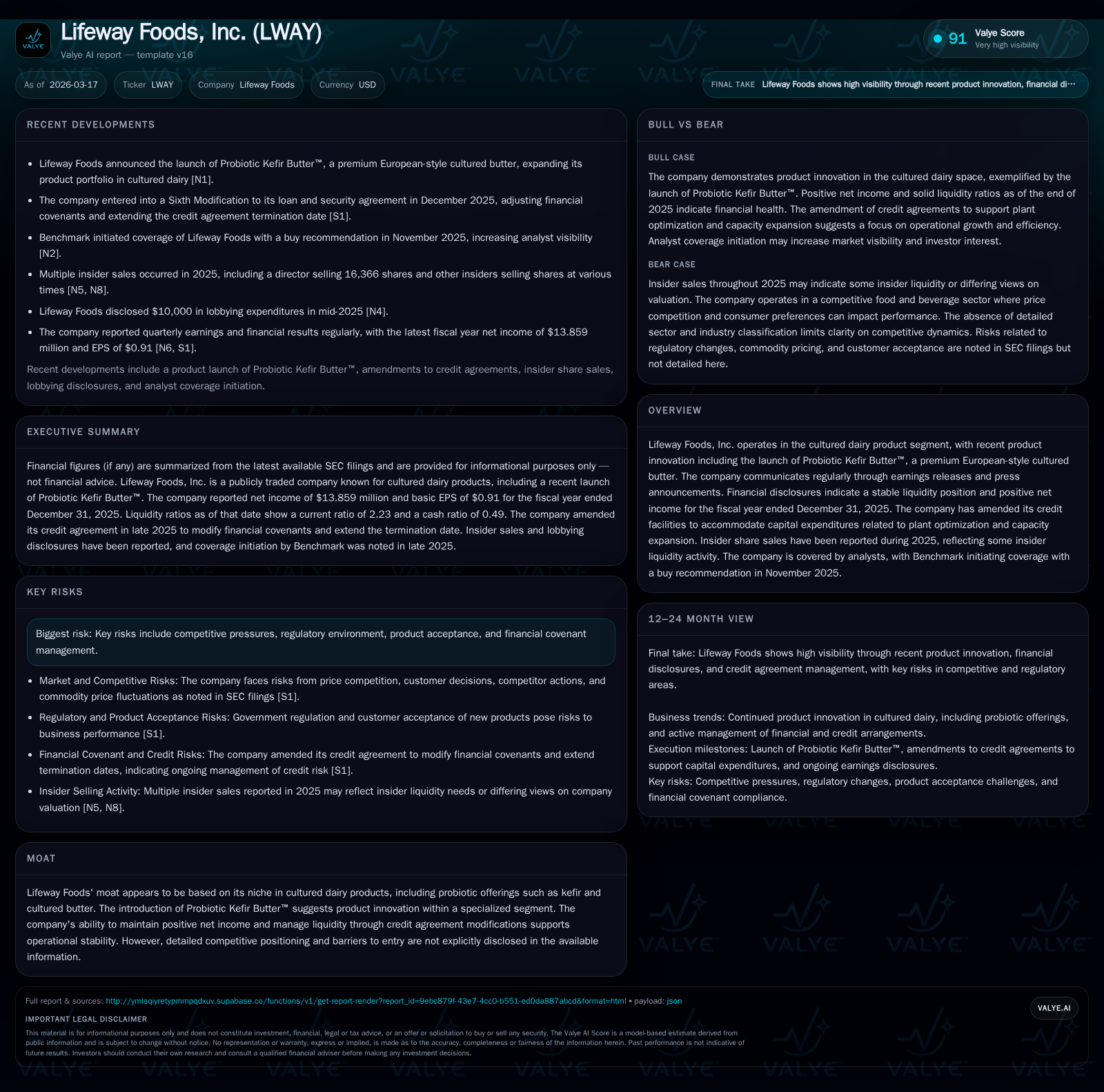

Lifeway Foods, a specialist in probiotic cultured dairy products, has successfully navigated a period of revenue contraction while expanding profitability through margin improvements and operational efficiencies. The recent launch of Probiotic Kefir Butter™ represents a step forward in product innovation aimed at premium markets. Supported by a substantial uptick in capital expenditures tied to plant optimization and capacity expansion — enabled by amendments to credit facilities — the company maintains strong liquidity and a solid financial foundation. Analyst endorsement alongside ongoing insider share sales presents a mixed but constructive investor outlook.

Historic Revenue Trends and Profit Dynamics

Lifeway Foods’ measured journey reflects a nuanced balance between top-line contraction and bottom-line enhancement over recent years. The company's revenue base notably retracted from its FY2018 high point of approximately $103.35 million by nearly 25%, highlighting pressures on sales volumes or pricing within its niche markets [F1]. Despite this top-line softness, operating income saw an encouraging ascent from $13.85 million in FY2024 to $16.17 million in FY2025 — an increase of roughly 16.7%. Net income showed even stronger growth of over 53%, reaching $13.86 million in FY2025 from $9 million the prior year [F1]. This disparity between revenue decline and net income increase indicates Lifeway has implemented effective cost containment measures or leveraged operational improvements that expanded margins.

However, it is important to note that operating cash flow (CFO) softened by about 15.5% year-on-year in FY2025 compared with FY2024, reflecting potential working capital demands or timing effects amid capex spending [F1]. Such trends suggest the company is maneuvering through transitional phases balancing growth investments against near-term cash generation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 14 | 11 | 16 | 27 | +53.6% |

| 2024 | 9 | 13 | 14 | 7 | -20.6% |

| 2023 | 11 | 17 | 17 | 4 | +1130.2% |

| 2022 | 1 | 4 | 2 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -16 | 16.1 | |

| 2024 | 6 | 12.6 | |

| 2023 | 0 | 13 | 18.8 |

| 2022 | 4 | 1 | 1.9 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Snapshot (FY2018-FY2025); source [F1]

Product Innovation: From Kefir to Probiotic Butter

Lifeway’s moat resides largely within its specialization in probiotic cultured dairy products—a segment catering increasingly to health-conscious consumers seeking functional food benefits beyond traditional dairy. The company's introduction of Probiotic Kefir Butter™, a premium European-style cultured butter infused with probiotics, underscores this strategy . This product represents an extension beyond their established kefir portfolio into high-margin specialty butters that appeal to gourmet as well as wellness-driven consumers.

This innovation not only distinguishes Lifeway within the specialty dairy segment but also aligns with broader industry trends favoring fermented and functional foods rich in beneficial microbial cultures. In doing so, Lifeway enhances its value proposition against competing producers often anchored solely in conventional dairy offerings.

Capital Expenditures Accelerate Production Expansion

FY2025 marked a pivotal year for capital investment as Lifeway dramatically scaled its production capabilities through plant optimization efforts centered on its Waukesha, Wisconsin facility [S7, S9]. Capital expenditures climbed sharply by over 300% year-over-year to approximately $27.4 million from just under $6.7 million the prior year [F1]. The accelerated spend targets both capacity expansion and manufacturing efficiency upgrades designed to support increased volumes of both existing and newly launched premium products like Probiotic Kefir Butter™.

Financially underpinning this strategic reinvestment was the Sixth Modification to Lifeway’s Amended Credit Agreement executed late December 2025 [S7]. This amendment extended the credit facility termination date to February 2029 while relaxing the Fixed Charge Coverage Ratio covenant for the period through mid-2027 to exclude up to $50 million of unfinanced capital expenditures related specifically to plant enhancements—a clear sign of lender accommodation toward Lifeway’s growth initiatives.

Financial Structure and Liquidity Strengthening

Lifeway entered these ambitious capex outlays from a position of relative liquidity strength. As of December 31, 2025, the company reported cash and equivalents totaling approximately $5.57 million against current liabilities near $16.64 million — supplying a comfortable current ratio of about 2.23x [F1]. Furthermore, no borrowings were outstanding immediately following the credit agreement amendments, signaling restrained leverage at the start of the expansion phase [S9].

The combination of solid short-term asset coverage and extended debt maturities mitigates refinancing risk over coming years while providing flexible capacity for incremental investment or potential working capital needs as production scales up further.

Analyst Endorsement and Shareholder Returns Overview

Recent market interest includes Benchmark’s initiation of analyst coverage with a buy recommendation reported in November 2025 , underscoring institutional recognition of Lifeway’s niche positioning combined with growth prospects.

Shareholder returns reflect mixed dynamics: while share repurchases have been suspended since FY2023 after prior intermittent activity totaling nearly $4 million until that year [F1], the company continues modest dividend distributions without significant acceleration as per available disclosures [S15, S20]. Return on equity (ROE) approximated at about 16% for FY2025 signals efficient capital deployment coinciding with earnings improvements despite negative free cash flow constrained by elevated capex ($10.95 million CFO minus $27.36 million capex yielding roughly -$16.4 million FCF) [F1].

Insider selling during calendar year 2025 contrasts with analyst optimism but may represent typical leadership liquidity rather than directional corporate signals given overall performance trends .

Risks from Competitive Pressures and Regulatory Environment

Lifeway operates within a competitive landscape shaped by increasing entrants into functional dairy segments and shifting consumer preferences that can be fickle regarding novel probiotic products [S4, S5]. Regulatory oversight on health claims related to probiotics imposes compliance complexity that can affect marketing efficacy and product labeling.

Additionally, financial covenant management remains sensitive amid ongoing capex commitments requiring careful balance to preserve lender relationships without constraining operational flexibility . Consumer acceptance uncertainty also tempers upside potential; introducing new probiotic formulations or premium priced products invites market testing risks inherent to specialty food categories.

What Investors Should Monitor Next

Looking ahead, key indicators will include tangible progress on expanded production output from optimized facilities—gauging whether scale efficiencies materialize without disruptive cost overruns or supply chain bottlenecks.

Equally important is measuring retail uptake of Probiotic Kefir Butter™ across distribution channels relative to competitive specialty butters, which could validate Lifeway's premiumization strategy.

Liquidity trajectory during this capex-intensive phase will warrant close observation; continued strong current ratios alongside prudent covenant compliance will be critical metrics reflecting financial health sustainability.

In absence of explicit updated guidance beyond existing framework disclosed through amendments or press releases [N#], these operational milestones serve as practical markers for assessing ongoing execution quality.

This analysis synthesizes publicly filed data from SEC sources , company facts filings [F1], and select third-party research commentary without offering investment recommendations or forecasts beyond documented disclosures. Market participants should consider broader sector trends impacting cultured dairy demand alongside Lifeway’s niche product development when evaluating future prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments