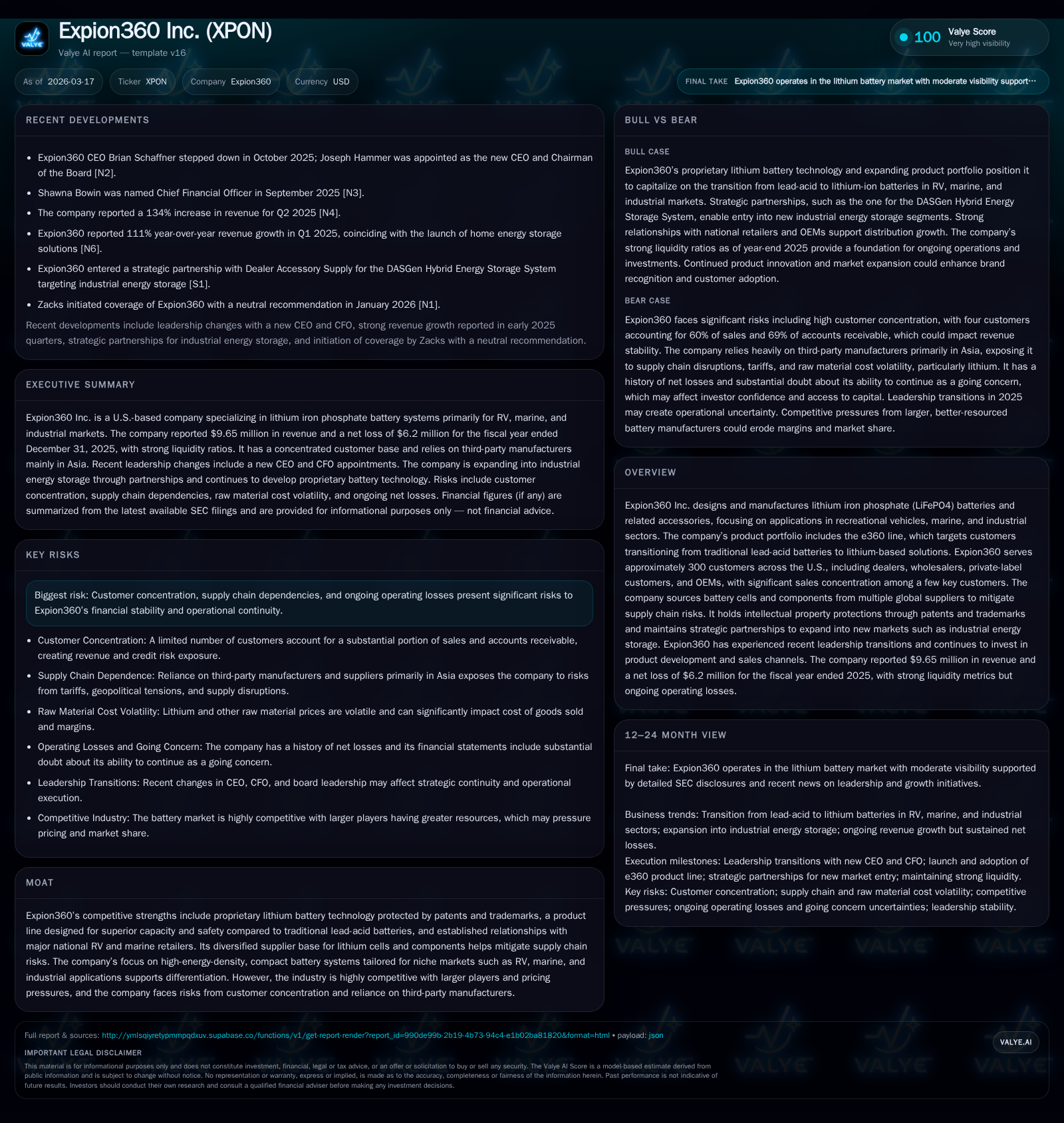

Expion360 Inc. Faces Growth Opportunity Despite Ongoing Losses and Customer Concentration

The lithium iron phosphate battery maker shows strong top-line growth but must manage operational and financial risks to sustain momentum.

Expion360 Inc. has delivered robust revenue growth driven by rising demand for lithium iron phosphate batteries in niche recreational vehicle, marine, and industrial markets. However, operating losses remain substantial, stemming from escalating costs and margin pressures tied to raw materials and supply chain dependencies. The company grapples with significant customer concentration and recent leadership changes that add layers of strategic uncertainty. Capital structure shows improved equity but persistent negative cash flows underscore the need for sustained operational improvements and financing access. Future growth hinges on successfully expanding customer breadth while maintaining cost control amid a competitive, tariff-impacted environment.

Company Overview

Expion360 Inc., trading as XPON, develops and manufactures lithium iron phosphate (LiFePO4) batteries tailored for recreational vehicle (RV), marine, and industrial use cases. The company’s core product line, branded as e360, targets replacement customers transitioning away from traditional lead-acid battery technologies by emphasizing higher energy density, safety features compliant with UL 1973 standards (pending final certification), and longer lifespans [S29][S14][S27]. Serving approximately 300 customers across the U.S., Expion360 counts among its clientele dealers, wholesalers, private-label partners, and original equipment manufacturers (OEMs), including leading national RV retailers like Camping World and Keystone Automotive [S17].

Historical Performance

Over recent years through fiscal 2025, Expion360 has achieved meaningful revenue expansion but continues to struggle with profitability challenges. Total revenue grew from approximately $7.16 million in 2022 to about $9.65 million in 2025—representing a compound annual growth rate around 9%, with an especially pronounced jump of +71.6% last year compared to 2024's $5.62 million [F1]. This increase reflects growing adoption of lithium battery solutions amid favorable industry trends such as electrification efforts in recreation and marine sectors.

Despite accelerating sales, operating income remained negative throughout the period, with an operating loss widening somewhat to -$10.7 million in 2025 from -$6.75 million in 2024 [F1]. Net losses have moderated from a peak of -$13.5 million in 2024 to -$6.2 million in the latest year, hinting at limited operating leverage but persistent challenges controlling costs [F1]. Operating cash flows have stayed negative as well (-$6.15 million in 2025), underpinning liquidity pressures despite minimal capital expenditure outlays ($20k in 2023 after a larger $567k capex step-up in 2022) [F1]. Equity rose to $6.53 million at end-2025 from about $2.52 million at end-2024 due to financing events [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 10 | -6 | -6 | -11 | +71.6% | +53.7% |

| 2024 | 6 | -13 | -10 | -7 | -6.0% | -80.8% |

| 2023 | 6 | -7 | -6 | -7 | -16.5% | +1.1% |

| 2022 | 7 | -8 | -5 | -6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 46889 | -95.4 | |

| 2024 | 46889 | -535.3 | |

| 2023 | -6 | -139.4 | |

| 2022 | -6 | -64.9 |

Source: SEC companyfacts cache [F1].

Note: All figures sourced from consolidated company filings [F1]. Capex shown only where data available.

Business Model and Market Positioning

Expion360’s strategy revolves around leveraging proprietary battery technology protected by eleven U.S. patent applications—including seven design patents and four utility patents—as well as trademarks extensively registered or pending both domestically and in Canada [S16][S17]. The focus is on delivering a compelling value proposition through lighter weight products featuring improved safety over incumbent lead-acid batteries while sustaining performance levels essential for niche recreational and industrial verticals.

The company's manufacturing relies significantly on third-party suppliers headquartered mainly in Asia—China producers are particularly critical—including secondary sourcing agreements with European suppliers offering alternative lithium iron phosphate cell components [S10][S25]. This dual-sourcing approach attempts to mitigate supply disruptions amid ongoing geopolitical trade tensions such as tariffs imposed by U.S authorities on Chinese imports affecting key battery components [S24][S10]. However, exposure remains elevated given that raw materials represent more than half the cost of goods sold; supply volatility and price fluctuations materially affect gross margins [S25][S15].

Customer Concentration Risks

A noteworthy risk factor is intense revenue concentration: four customers generated roughly sixty percent of gross sales during fiscal year ending December 31, 2025; these same clients represented nearly seventy percent of accounts receivable balances at year-end [S4][S17]. This high concentration exposes Expion360 to substantial demand fluctuations or credit risk if key accounts reduce purchasing or delay payments substantially.

Most transactions occur via purchase orders without long-term firm commitments or contracts binding customers over extended periods—a typical characteristic of the industry that increases revenue predictability challenges [S4][S17]. The possible loss or downsizing by any major buyer could prompt pricing pressures or necessitate discounting that compresses margins further [S4][S15].

Leadership Transitions Impact

Recent corporate governance changes have added complexity to executing strategic priorities effectively. In April and September of last year respectively, Expion360 appointed a new Chief Operating Officer (Carson Heagen) and Chief Financial Officer (Shawna Bowin). Subsequently in October 2025 both the existing Chief Executive Officer Brian Schaffner and President/Chairman Paul Shoun resigned; the board installed Joseph Hammer as new CEO/Chairman shortly thereafter [S18][S2].

These leadership shifts introduce transitional risks associated with potential disruption in management continuity affecting operations or customer relationships. While new executives bring fresh perspectives possibly conducive to execution acceleration, integration remains at an early stage with outcomes uncertain over the near term [N/A].

Competitive Environment

The lithium battery market is intensely competitive; Expion360 competes against global giants as well as numerous regional players producing lithium-ion or lead-acid alternatives [S14]. The firm claims superiority through product performance traits—particularly lower weight and safer chemistry—yet it confronts pricing pressure from rivals benefiting from scale economies or lower labor costs abroad.

OEM partnerships offer expansion potential but typically come at reduced average selling prices relative to direct-to-consumer sales channels compromising overall margin profiles [S14]. Maintaining differentiation relies heavily on continued innovation plus strengthening dealer relationships while managing rising input costs tied primarily to global raw material price surges including lithium metal itself which remains subject to cyclical volatility despite advances like recycling programs aimed at supply sustainability improvements [S10].

Regulatory and Operational Considerations

Deliveries comply with regulations governing transport of dangerous goods given classification of lithium-ion batteries requiring adherence under laws enforced federally/state/local regulators [S17][S22]. Environmental compliance currently poses limited immediate liabilities though regulatory scrutiny could intensify as production scales, potentially adding cost burdens.

Operationally dependence on limited warehouse facilities raises exposure against capacity constraints or disruption risks impacting timely fulfillment capabilities [S24]. Likewise any interruptions at external Asian-manufactured components sites could ripple through Expion360’s production scheduling aggravating inventory imbalances noted recently due to overcapacity driving unit cost escalations inhibiting margin improvement attempts [S4][N/A].

Capital Allocation & Financial Health

Expion360’s capital management reflects priorities aligned with long-term growth albeit funded largely via equity infusions evidenced by rising shareholders' equity balances [$6.54M end-2025 vs $2.52M prior year] rather than debt-heavy structures which remain modest per filings [F1][S21].[F1] Cash & equivalents stood at just under $3 million end-2025 providing near-term liquidity cushion given operating burn rates.

Operating cash flows were negative nearing $6.15 million last fiscal year versus capital expenditures being negligible resulting in free cash flow reflecting significant net cash usage indicative of the ongoing investment phase typical for emerging companies prioritizing market share gains over short-term profitability.

No dividends are declared given persistent losses; minor share repurchases (~$47K) reported for prior periods suggest limited buyback activity consistent with funding conservation during development cycle stages [F1]. Return on equity calculated approximately at negative ~95%, underscoring unprofitability relative to invested capital base despite revenue gains highlighting operational leverage constraints thus far.

Forward-Looking Considerations & Growth Prospects (Analysis)

Explicit financial forecasts or guidance remain undisclosed within filings reviewed or announcements available through March '26; yet several factors will likely shape near-to-medium term trajectory:

- Expansion of OEM customer base beyond currently concentrated few would improve revenue visibility and reduce key-account dependency.

- Broadening direct-to-consumer channels leveraging dealer networks nationally strengthens recurring revenue potential.

- Continued R&D investment towards product improvement may enable premium positioning supporting price maintenance thus counteracting raw material-driven cost inflation.

- Mitigation strategies addressing supply chain fragility—such as securing alternative suppliers outside Asia—may reduce tariff exposure risks stemming from geopolitically sensitive procurement locations.

- Leadership stabilization fostering consistent strategic execution critical following recent executive turnover potentially impacting organizational momentum.

- Industry dynamics including regulatory evolution for battery technology safety standards could impose compliance costs but also open opportunities for certified differentiators.

Monitoring quarterly operational metrics including order backlog progression along with inventory turns will be important barometers indicating capability scaling without eroding unit economics critically necessary for approaching sustained profitability milestones (currently elusive given losses).

Conclusion

Expion360 stands at a pivotal junction characterized by encouraging top-line growth fueled by increasing market penetration for its lithium iron phosphate batteries within specialized niches such as RVs and marine applications.[F1][N/A] The company's patent-backed technological edge combined with multiple sourcing strategies partially offsets competitive threats yet exposure remains pronounced from concentrated customer relationships alongside volatile raw material inputs exacerbated by tariffs.[S4][S15][S25]

Persistent net losses accompanied by sizable negative cash flow highlight ongoing operational hurdles threatening its going concern status flagged by auditors.[F1][S15] Recent leadership transitions inject uncertainty regarding strategic continuity even as fresh management seeks traction toward reducing dependency risks while improving operational efficiency.[N/A]

Long-term success will depend on capitalizing further on market demand momentum balanced against managing increasingly complex supply chain logistics provider diversification together with measured expense control efforts vital for eventual profitability realization without surrendering technical differentiation advantages crucial in this fragmented energy storage landscape.

This analysis summarizes publicly available information from SEC filings up through March ‘26 without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments