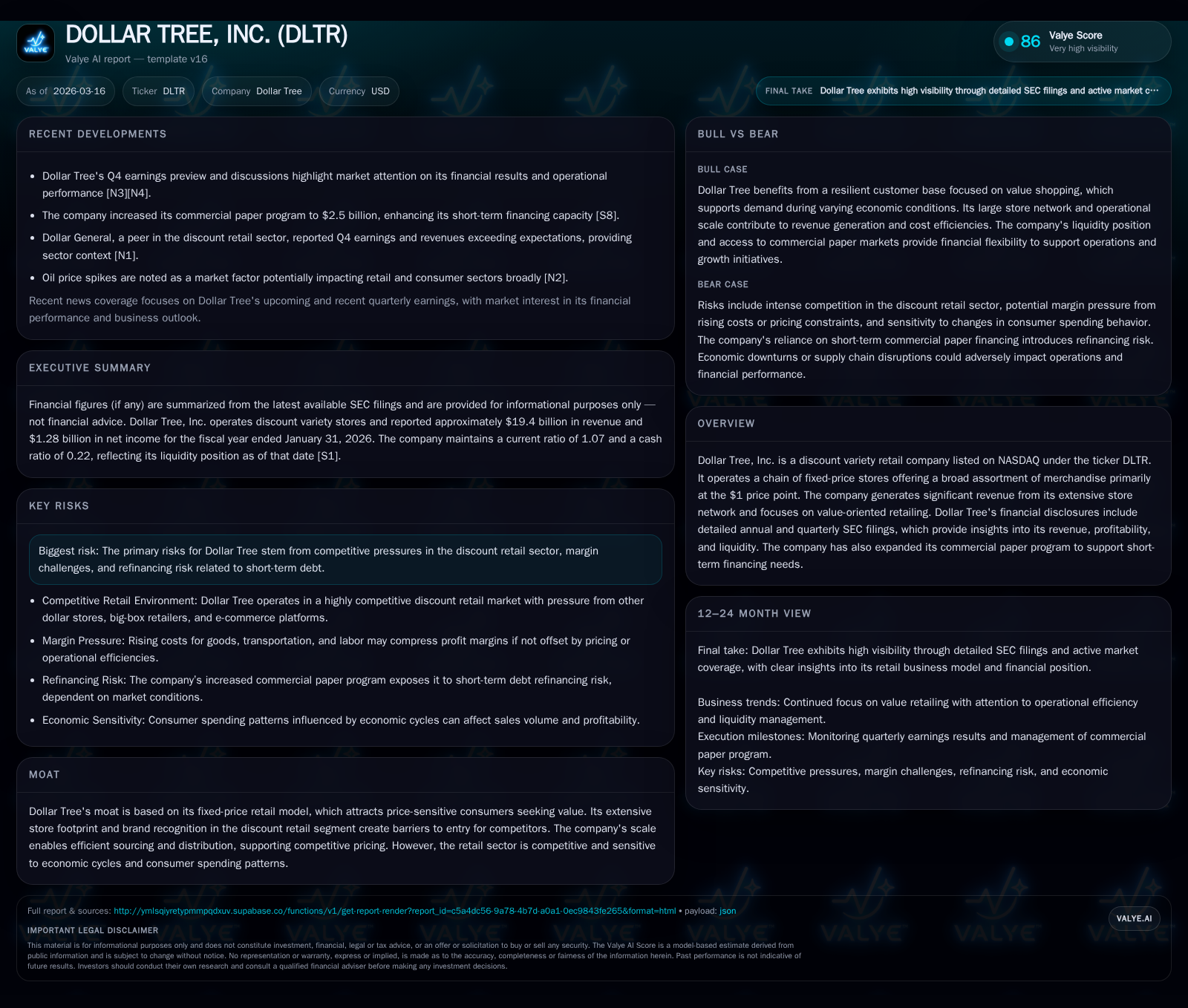

Dollar Tree’s Strategic Reinvention and Financial Recovery After Family Dollar Sale

Post-divestiture, Dollar Tree refocused on its core fixed-price business, recovering profitability and reshaping capital structure amidst discount retail pressures.

Dollar Tree’s sale of Family Dollar in mid-2025 marked a pivotal strategic reset, enabling a concentrated emphasis on its value-oriented, fixed-price stores. This shift is evidenced by a robust rebound in FY2025 revenue and profitability metrics, with revenue up 10.4% and net income doubling year-over-year. However, margin pressures from inventory shrinkage and seasonal variances remain operational challenges. The company also augmented its commercial paper program to strengthen liquidity management post-divestiture while executing sizable share buybacks that reflect deliberate capital allocation priorities. Forward focus includes navigating regulatory compliance cost increases and refinancing risks tied to short-term debt facilities.

From Divestiture to Focused Growth: The Impact of Family Dollar’s Sale

Dollar Tree’s strategic decision to divest Family Dollar culminated in July 2025, following a review process initiated in fiscal 2024 [S1]. This transaction realigned the company away from a dual-banner model toward an intensified focus on the core fixed-price ($1) retail stores that constitute its brand moat. Financially, this divestiture was significant — the business met held-for-sale classification criteria in late 2024 and subsequently incurred an impairment loss of approximately $3.4 billion recorded in fiscal 2024 [S1]. Upon completion, an additional loss on disposal of roughly $408 million was recognized in fiscal 2025 reflecting actual proceeds against the carrying amount less selling costs.

The divestiture effected a major shift in Dollar Tree's asset base and operational footprint, including cessation of depreciation on Family Dollar-related right-of-use assets [S1]. The sale also generated total cash inflows around $793 million combining net proceeds and monetized working capital adjustments prior to closing [S1]. Importantly, results for all presented periods are restated to exclude continuing Family Dollar operations as they are now classified under discontinued operations per accounting standards.

This financial reset freed resources and management attention for expanding and optimizing the fixed-price store network under the Dollar Tree banner. It also simplified operational complexities posed by running two distinct discount retail formats.

Revenue and Profitability Trends Underlying the Turnaround

Post-divestiture FY2025 figures showcase a meaningful rebound across key performance dimensions supported by [F1], [S3], and [N13]. Revenue advanced 10.4% year-over-year to approximately $19.4 billion [F1], reversing prior contraction when combined with exit from Family Dollar's lower-margin business lines.

Operating income climbed more modestly by 13.1% to about $1.65 billion driven by efficiency gains but tempered by ongoing margin headwinds [F1]. Net income experienced an impressive turnaround from substantial losses the prior year — an increase of over 134% year-over-year to $1.28 billion highlighting strong bottom-line recovery post divestiture [F1].

Cash generation improved significantly as well; operating cash flow jumped by over 66% year-on-year (data from earlier years limited to FY2023 and FY2022 levels) indicating better working capital management and profitability translating into free cash flow estimated near $1.87 billion after capital expenditures [F1]. Capital expenditures rose moderately reflecting ongoing investments into store remodels and distribution capabilities necessary for fixed-price retail expansion.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 19.4 | 1.3 | 1.7 | +10.4% | +134.7% | |

| 2024 | 17.6 | -3.7 | 1.5 | -42.6% | -270.2% | |

| 2023 | 30.6 | -1.0 | 2.7 | -0.9 | +8.0% | -161.8% |

| 2022 | 28.3 | 1.6 | 1.6 | 2.2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 1548 | 34.2 |

| 2024 | 400 | -92.9 |

| 2023 | 500 | -13.7 |

| 2022 | 648 | 18.5 |

Source: SEC companyfacts cache [F1].

Note: CFO data only available through FY23; capex data not comparable beyond earlier fiscal years.

Price-Point Retail Pressures and Their Effects on Margins and Consumer Demand

The essence of Dollar Tree’s business model is fixed-price pricing strategy which reliably attracts value-conscious consumers but exposes the company to intense cost pressures typical in discount retailing [S1]. A pronounced industry-wide challenge reflected at Dollar Tree is escalating inventory shrinkage attributed primarily to theft, run rates hitting historic highs recently according to management commentary [S1]. Such shrinkage demands elevated investment in loss prevention technologies and personnel increasing SG&A expense pressure.

Operational cadence is also complicated by seasonality: Easter timing shifts materially compress or extend selling windows critical for seasonal products such as holiday-related merchandise impacting inventory turnover rates as well as requiring markdown activity if sales fall short [S1]. Merchandise markdowns directly compress gross margins, a crucial concern given low price points leave limited room for error or cost absorption.

Further margin pressures derive from macroeconomic dynamics influencing consumer price sensitivity since fixed-price retailers experience constrained ability to pass cost increases onto customers compared with broader multiple-price competitors.

Evaluating Key Forecasts and Factors to Monitor Going Forward

While specific forward guidance remains guarded without explicit numerical targets disclosed publicly recently [N1], strategic paths point towards monitoring several critical risk vectors impacting growth trajectory:

- Seasonal selling variability due to weather patterns or calendar shifts like early Easter shortening effective selling periods poses downside sales risk [S1], [N3].

- Regulatory scrutiny around pricing clarity within multi-price assortments may compel operational adjustments increasing compliance costs as noted in risk disclosures [S4].

- Refinancing risk remains prominent given reliance on expanded short-term borrowings with evolving credit market conditions potentially influencing borrowing cost volatility [S1], [N1].

- Competitive positioning requires watchfulness amidst intensifying rival discount chains optimizing multi-tier pricing models which could erode traffic into fixed-price formats.

Analysts should track quarterly releases for updates on these factors alongside any changes in inventory turnover metrics or SG&A expense trends signaling shifts in underlying operating leverage.

Capital Structure Reshaping: Debt Dynamics and Commercial Paper Expansion

In parallel with operational realignment post-Family Dollar sale, Dollar Tree enhanced its liquidity framework by increasing its commercial paper program limit from $1.5 billion up to $2.5 billion late in fiscal 2025 aimed at bolstering short-term financing flexibility [S6],[S7]. This adjustment correlates closely with maturing debt profiles including the impending March 2026 maturity of the existing $364-day facility, creating space for refinanced liquidity buffers.

From a practitioner perspective, this expanded unsecured commercial paper capacity allows dynamic management of working capital needs while smoothing refinancing cycles amid potentially volatile credit markets common for retailers reliant on cyclical inventories.

Such liquidity provisions help buffer against seasonal cash flow swings or unexpected operational disruptions related to supply chain or regulatory enforcement costs flagged under risk disclosures [S5],[S9].

Capital Allocation Excellence: Buybacks, Cash Flow, and Return on Equity

Consistent with renewed profitability power demonstrated by operating cash flow growth (+66% YoY) estimated at about $2+ billion range before capex deductions, Dollar Tree aggressively ramped share repurchases totaling approximately $1.55 billion during FY2025—a nearly fourfold increase relative to FY2024 levels [F1],[S10]. This elevated buyback pace signifies focused capital return strategy designed to leverage earnings quality improvements while offsetting equity base contraction post-divestiture which reduced book equity notably.

Calculated return on equity stands near a strong ~34% ratio derived from net income over average equity reported at about $3.75 billion year-end FY25—underscoring highly efficient use of invested capital post-product portfolio streamlining [F1].

This capital discipline aligns well with sector norms where legacy bricks-and-mortar retailers seek continuous shareholder value creation amid competitive headwinds via disciplined balance sheet deployment rather than solely chasing growth initiatives.

Operational Challenges: Inventory Management, Shrinkage, and Compliance Costs

Retail industry terminology sharply focuses here on "shrinkage" describing inventory losses primarily from theft including organized retail crime—recently highlighted as reaching unprecedented levels at Dollar Tree prompting increased investment into sophisticated preventative solutions both technological (e.g., RFID tagging enhancements) and human resource-intensive measures [S1]. Despite these efforts, residual shrinkage remains a persistent margin eroder necessitating accurate accrual predictions which if misjudged can lead to significant earnings volatility.

Compounding these challenges are escalating regulatory compliance burdens spanning areas critical for discount retailers such as food/drug safety laws rigorously enforced under federal statutes alongside localized scrutiny over pricing transparency rules expectedly tightening due to growing multi-price assortment initiatives at Dollar Tree [S4]. Employee safety regulations further raise SG&A costs particularly important amid high staff turnover inherent to low-wage sectors impairing productivity.

These factors collectively contribute upward pressure on operating expenses consequently constraining margin improvement prospects even during top-line growth phases highlighting complexity underlying discount retail profit structures beyond just volume dynamics.

Disclaimer: This analysis is based solely on publicly available information as referenced from SEC filings and primary news sources as of March 16, 2026, without extrapolation or undisclosed estimates; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments