Monte Rosa Therapeutics Advances Molecular Glue Pipeline While Managing Clinical-Stage Headwinds

Monte Rosa pushes forward its innovative molecular glue degrader programs and key clinical collaborations while demonstrating improving financial discipline amid ongoing operational losses.

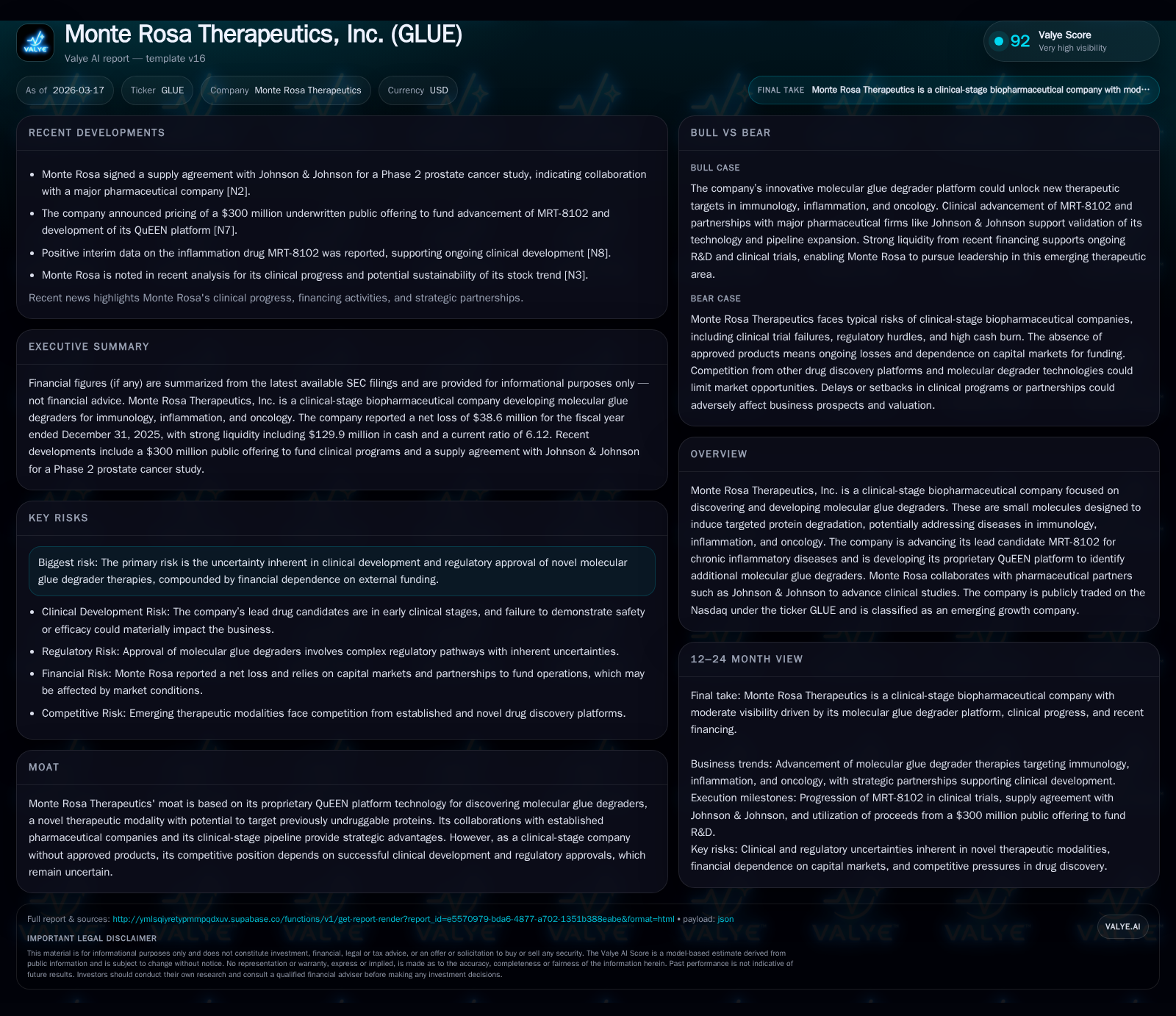

Monte Rosa Therapeutics, a pioneer in molecular glue degraders, has shown marked improvements in operating losses and net income over the last four years as it invests in clinical-stage development of its lead MRT-8102 candidate and QuEEN discovery platform. Strategic partnerships, notably with Johnson & Johnson, provide validation and operational support for its pipeline advancement targeting inflammation and oncology. However, the company remains a clinical-stage entity facing significant execution, regulatory, and financing risks, with recent capital raises bolstering a liquidity runway into 2029. Upcoming clinical milestones and IND filings will be critical for validating its novel therapeutic modality.

From R&D Momentum to Clinical-Stage Realities: Historical Performance Review

Monte Rosa Therapeutics has exhibited a meaningful trajectory of financial improvement over recent years, driven by its concentrated efforts on molecular glue degrader discovery and clinical study advancement. Operating income losses shrank significantly from -$112 million in FY2022 to -$54 million in FY2025 — a roughly 33% year-on-year improvement most recently. Net income followed a similar pattern with losses narrowing from -$108.5 million in FY2022 to -$38.6 million at FY2025 year-end [F1]. This reflects both improved expense discipline and potential early efficiencies as clinical programs mature.

Operating cash flow remains negative at -$22.8 million in FY2025 but compares favorably to larger outflows in prior years [F1]. Capital expenditures have been relatively stable though declining after peaking at $19 million in FY2023, underscoring a shift into focused trial execution versus heavy upfront infrastructure buildout. The current ratio of over 6x highlights solid short-term liquidity management [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -39 | -23 | -54 | 5 | +46.9% |

| 2024 | -73 | 42 | -81 | 4 | +46.3% |

| 2023 | -135 | -44 | -143 | 19 | -24.7% |

| 2022 | -109 | -92 | -112 | 13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -27 | -16.6 |

| 2024 | 0 | 38 | -32.6 |

| 2023 | 0 | -63 | -75.5 |

| 2022 | 0 | -105 | -40.0 |

Source: SEC companyfacts cache [F1].

Declining operating loss reflects better cost control alongside ongoing R&D spend.

QuEEN Platform’s Edge in Targeted Protein Degradation

Central to Monte Rosa's competitive moat is the proprietary QuEEN platform—an advanced molecule-discovery tool designed to identify molecular glue degraders (MGDs), which induce targeted protein degradation by promoting induced proximity between target proteins and E3 ubiquitin ligases [S1][N5]. This approach allows modulation of ‘‘undruggable’’ targets that traditional inhibitors cannot reach, notably within inflammation and oncology pathways.

The technology leverages nuanced structural biology insights to design small molecules mediating protein ubiquitination selectively, opening broader therapeutic scope across challenging proteomes—a frontier in degrader drug discovery not widely accessible to many competitors [N5]. This technological edge supports multiple internal programs beyond MRT-8102 and informs strategic pharmaceutical collaborations.

Strategic Collaborations Bolstering Pipeline Development

Monte Rosa’s alliance model demonstrates its pragmatic approach toward balancing internal innovation with external expertise and resources. A recent supply agreement with Johnson & Johnson underpins the company's plan to contribute its molecular glue candidate MRT-2359 into J&J-led Phase 2 studies in prostate cancer [N5].

Such collaboration serves dual purposes: reducing capital intensity by sharing development burdens while leveraging J&J’s established regulatory and clinical trial apparatus potentially accelerates timelines and enhances program validation externally.

This partnership complements other efforts such as Novartis planning multiple Phase 2 studies for another MGD asset (MRT-6160) emphasizing immune disease targets for further pipeline diversification [S28].

Pipeline Outlook: MRT-8102 and Emerging Candidates

The lead clinical asset MRT-8102 targets the NLRP3 inflammasome pathway implicated in various chronic inflammatory conditions including atherosclerotic cardiovascular disease [S17][N2]. Its ongoing Phase 1/2 studies encompass single/multiple ascending dose cohorts plus an expansion cohort focused on subjects with elevated cardiovascular risk.

Early data presented suggests favorable safety signals although efficacy proof awaits larger readouts anticipated soon [S29]. The company expresses plans for accelerated Phase 2 trials (GFORCE-2) targeting ASCVD expected within the year with parallel exploration into liver (MASH), gout, and pericarditis indications linked to the NLRP3/IL-1/IL-6 axis [S17][S18].

Additional pipeline candidates include next-gen NEK7-directed MGDs along with oncology-focused MRT-2359 under combination regimens targeting castration-resistant prostate cancer (CRPC) with androgen receptor mutations—the latter being studied under new Phase 2 protocols following promising interim data [S28][S29]. IND applications continue to expand the breadth of target engagement.

Financial Health: Cash Position, Operating Losses, and Capital Strategy

At December 31, 2025, Monte Rosa held approximately $130 million in cash and equivalents against current liabilities around $64 million yielding a current ratio near 6.1 — clear evidence of comfortable near-term liquidity [F1]. This strong position was materially enhanced by a January 2026 public offering which raised net proceeds close to $282 million [S19], underpinning operational funding into at least early 2029 [S14].

Despite improved operating loss trends, free cash flow remains negative at about -$27 million due largely to continued R&D investment imperative for clinical-stage progress [F1]. Such burn rates are typical given trial execution intensity but highlight reliance on capital markets for sustained operation.

Capital Deployment: Fundraising, Cash Burn, and Share Dilution Risks

The recent equity raise featuring common stocks and pre-funded warrants was geared specifically toward advancing MRT-8102 development across prioritized inflammatory indications alongside enhancing utilization of the QuEEN discovery platform to spawn next-generation MGDs [S8][N5]. The firm confirmed no dividends nor share buybacks reflecting full reinvestment strategy typical of early-stage biotechs focused on pipeline maturation.

Pre-funded warrants include ownership limitations carefully structured not to exceed threshold holdings unless prior notice is provided—measures balancing investor concentration risk against fundraising flexibility [S15]. Management also terminated prior at-the-market offerings indicating shift towards larger block transactions over gradual float-based capital generation to reduce dilution frequency [S21][S27].

Investors should weigh dilution risks inherent in recurring financings against long-term value creation potential residing in molecular glue modality breakthroughs.

Clinical & Regulatory Hurdles Ahead

The novelty of molecular glue therapies inherently elevates clinical risk profiles due both to unproven regulatory pathways and mechanistic complexities inherent in induced proximity pharmacology [S4][S5][S6]. Early signals though encouraging are insufficient for final approval decisions pending robust efficacy datasets from randomized controlled trials.

Regulatory agencies may impose extensive scrutiny given first-in-class nature requiring rigorous evaluation of safety margins especially when modulating inflammasome cascades or oncogenic pathways where off-target effects could be problematic.

Competitive landscape intensifies as more entities enter targeted protein degradation — demanding rapid yet careful translation of preclinical insights into clinching human proof-of-concept readouts.

Investor Watchpoints: Upcoming Milestones and Market Catalysts

Key near-term milestones include scheduled presentations of interim Phase 1 data for MRT-8102 anticipated within early 2026 along with initiation of Phase 2 GFORCE-2 trial targeting ASCVD patients [N2][S29]. Positive outcomes here could validate MOA claims establishing market differentiation.

Other critical events encompass IND submissions planned for novel MGDs addressing NEK7, CDK2/cyclin E1 axes plus updates from the prostate cancer combination study MRT-2359 slated during ASCO Genitourinary Cancers Symposium proceedings [S28][N5].

Additionally, progress updates on collaborative trials led by J&J or Novartis will provide directional insight into external partner confidence levels impacting valuation sentiment.

Overall, while opportunities are substantial given therapeutic novelty plus platform scalability, investors must remain vigilant regarding clinical-readout-dependent swings typical of biopharma innovation sectors.

This report synthesizes publicly filed SEC financial documents alongside recent news announcements without offering investment advice or price forecasts. Monte Rosa Therapeutics exemplifies emerging growth biopharma challenges wherein proprietary technology platforms promise transformative impact conditional upon successful clinical development execution amid capital-intensive investing cycles.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments