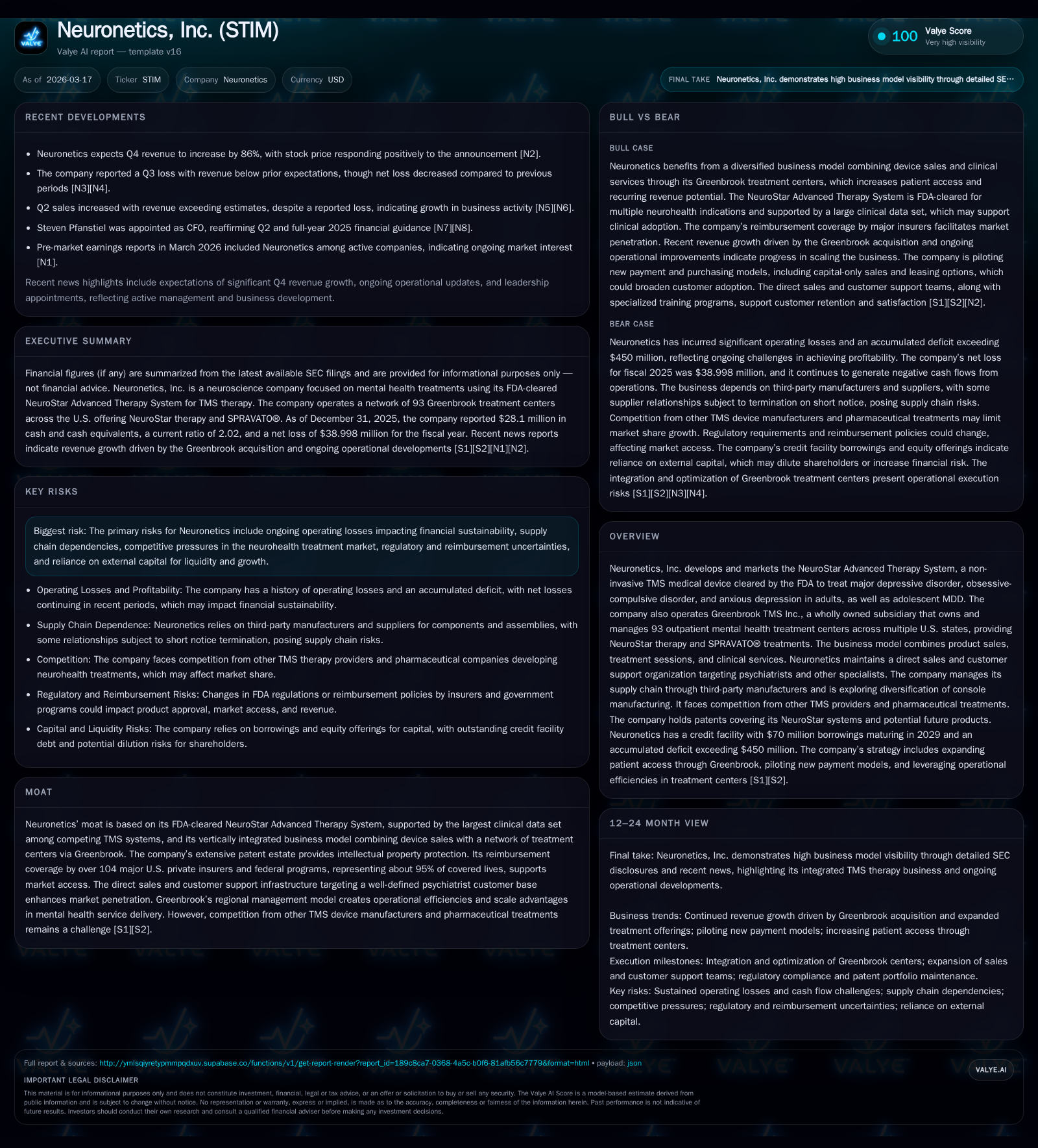

Neuronetics’ Revenue Momentum and Market Reach Under CEO Transition

Neuronetics leverages its FDA-cleared NeuroStar system and Greenbrook clinic network to grow transcranial magnetic stimulation therapy despite persistent losses and leadership changes.

Neuronetics, Inc. has maintained relatively steady revenues in recent years, driven by its NeuroStar Advanced Therapy System and expanded treatment services through Greenbrook TMS centers. The company operates an integrated model combining device sales with outpatient clinics, supported by broad reimbursement coverage and a robust patent portfolio. Despite ongoing operating losses and cash flow challenges, recent management changes may signal strategic shifts to accelerate growth. Key drivers include increased adoption of NeuroStar therapy, expansion of Greenbrook’s service footprint, and innovation in payment models within a competitive neurohealth landscape.

Historical Performance

Neuronetics’ annual revenues have been generally stable over recent years, reported at approximately $15.6 million in FY2018, rising slightly to $17.3 million in FY2019 before returning near $15.6 million by FY2020 [F1]. Despite this revenue stability, operating income reflected consistent losses: about -$35.1 million in FY2022 improving modestly to -$31.4 million by FY2025. Net losses followed a similar pattern with -$37.2 million in FY2022 and -$39.0 million in FY2025 [F1]. Operating cash flows remained negative but showed improvement from -$30.9 million in FY2024 to -$20.4 million in FY2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -39 | -20 | -31 | +10.8% |

| 2024 | -44 | -31 | -35 | -44.8% |

| 2023 | -30 | -32 | -31 | +18.8% |

| 2022 | -37 | -31 | -35 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -174.3 |

| 2024 | -157.8 |

| 2023 | -88.3 |

| 2022 | -65.1 |

Source: SEC companyfacts cache [F1].

Business Model Overview

Neuronetics combines sales of its FDA-cleared NeuroStar Advanced Therapy System with delivery of neurohealth treatments through the Greenbrook outpatient mental health network acquired in late 2024 [S5][S9]. Greenbrook operates 93 Treatment Centers across multiple U.S. states offering NeuroStar therapy alongside SPRAVATO® treatments for treatment-resistant depression [S16]. This vertically integrated approach provides recurring revenue streams from both device sales and ongoing treatment sessions.

The company targets approximately 53,000 psychiatrists across around 26,000 practices nationwide through a direct sales force focused on expanding NeuroStar adoption [S9]. Specialized teams handle customer support and reimbursement assistance to facilitate market penetration.

Market Access and Competitive Positioning

Neuronetics benefits from extensive reimbursement coverage enabling patient access: over 104 major private insurers plus federal healthcare programs cover NeuroStar therapies representing nearly 95% of insured U.S. lives [S1][S4]. This broad payor network supports sustainable treatment economics.

The company maintains a strong intellectual property portfolio with more than 60 issued patents globally protecting its technology platform related to TMS devices and manufacturing methods [S15]. Competition arises from other TMS manufacturers such as Brainsway and Magstim as well as pharmaceutical alternatives for neurohealth disorders [S15].

Supply Chain and Manufacturing Strategy

Manufacturing is outsourced under strict specifications managed by Neuronetics’ operations team based in Malvern, Pennsylvania [S4]. Console assembly recently transitioned to Ascential Technologies to enhance supply chain resilience. Key suppliers include Molex Incorporated for SenStar components and Gharieni Group GmbH for chairs used in treatment setups. Plans are underway to add a second console manufacturer partner to reduce dependence on single-source suppliers [S4].

Leadership Transition and Strategic Outlook

In March 2026 Neuronetics announced CEO Keith Sullivan would step down with Dan Reuvers named successor amid ongoing integration efforts following the Greenbrook acquisition [N3]. This leadership change could signify renewed emphasis on operational efficiencies and accelerating revenue growth.

Capital Allocation and Financial Position

Neuronetics finances operations through equity raises—including a secondary public offering netting approximately $18.9 million early in 2025—and an At-The-Market program generating net proceeds of about $7.8 million as of late 2025 [S7]. The company also maintains borrowings under a $70 million credit facility maturing in July 2029 with substantial outstanding balances [F1][S7][S13].

Despite improvements in operating cash flow (-$20.4 million in FY2025 versus larger negative flows previously), free cash flow remains negative reflecting continued investment needs and losses. Shareholders' equity declined from approximately $57 million at end-FY2022 to about $22 million at end-FY2025 due to cumulative deficits resulting in an approximate negative return on equity near -174% for the latest fiscal year [F1].

Growth Catalysts and Risks

Growth drivers include increased adoption of NeuroStar therapy supported by clinical data strength; expansion of Greenbrook Treatment Centers into additional regions using regional management models; payer coverage stability; and innovations in payment models such as capital-only equipment sales and leasing options piloted recently [N2][S9][S16].

Risks remain from regulatory compliance demands including FDA premarket clearance processes for product modifications; ongoing Quality System Regulation adherence; potential supply chain disruptions; intense competition from alternative therapies; and evolving reimbursement environments impacting profitability timelines [S6][S12][S20].

Key Milestones to Monitor

Important indicators going forward include quarterly trends in NeuroStar device sales; geographic growth of Greenbrook Treatment Centers; developments in reimbursement policies especially Medicare-related updates; new clinical study results expanding indications or demonstrating long-term outcomes; and announcements regarding strategic initiatives under new leadership [N2][N3][S9][S16].

Disclaimer: This analysis is based solely on publicly available SEC filings and news reports dated up to March 17, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments