Spirit Aviation's Transformation Amid Bankruptcy and Competitive Pressures

Spirit Aviation Holdings operates a value-based low-cost model while navigating restructuring and market challenges.

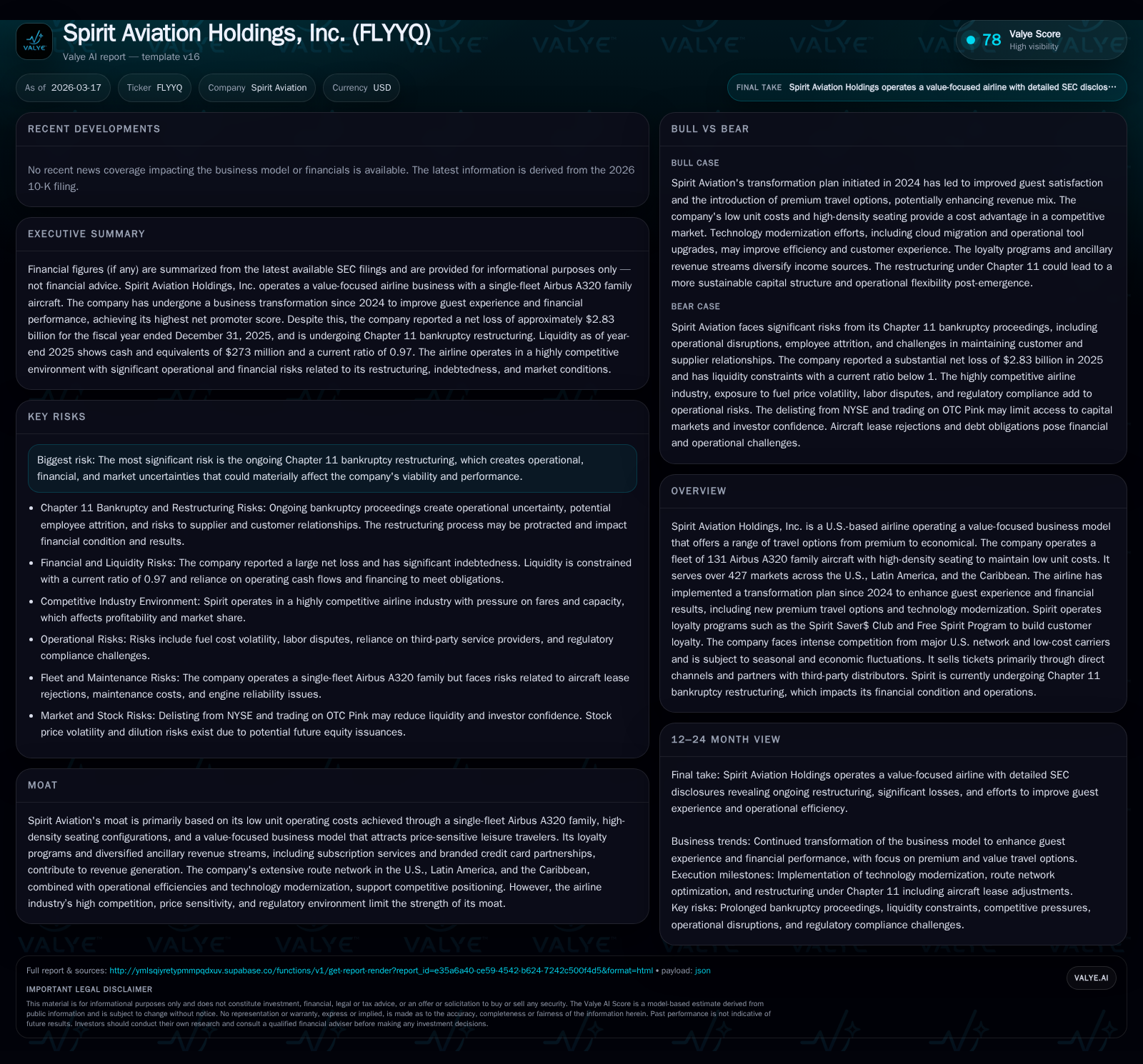

Spirit Aviation Holdings, Inc. remains a value-oriented airline operating a uniform Airbus A320 family fleet across 427 markets in the U.S., Latin America, and the Caribbean. The company filed for Chapter 11 bankruptcy in 2025 after sustained financial losses worsened by industry capacity growth and inflationary pressures. Since 2024, it has pursued a strategic transformation to diversify travel options and enhance guest satisfaction, reflected in its highest net promoter score historically. Despite these efforts, Spirit reported significant net losses and negative operating cash flows in fiscal year 2025, with equity deeply negative due to accumulated deficits and restructuring impacts. Liquidity remains constrained with cash balances near parity with current liabilities. The airline faces ongoing risks from competitive intensity, regulatory compliance costs, operational uncertainties, and its restructuring process. Future performance depends critically on successful emergence from bankruptcy alongside effective execution of its transformation strategy.

Company Background

Spirit Aviation Holdings, Inc. operates as a value-focused carrier providing low-cost air travel mainly within the United States, Latin America, and the Caribbean. The company maintains a uniform fleet of 131 Airbus A320 family aircraft configured with high-density seating to keep unit operating costs among the lowest in the industry [S9]. Its product offering includes tiered travel options ranging from basic Value fares to enhanced Spirit First and Premium Economy classes introduced under its transformation plan launched in 2024 aimed at elevating guest experience [S1].

Historical Performance

Spirit demonstrated revenue growth from approximately $474 million in fiscal year 2014 to $667 million by 2017 [F1]. However, beginning in 2022 the company faced significant financial deterioration marked by sustained operating losses and negative net income as shown below:

Historical performance (annual)

| FY | Net ($bn) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2.8 | -707 | -482 | -230492.9% |

| 2024 | 0.0 | -758 | -1105 | +100.3% |

| 2023 | -0.4 | -247 | -496 | +19.3% |

| 2022 | -0.6 | -89 | -599 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 135.4 |

| 2024 | 1 | -1.5 |

| 2023 | 3 | -39.4 |

| 2022 | 2 | -35.3 |

Source: SEC companyfacts cache [F1].

Operating income remained negative reflecting operational stress; net losses surged particularly in fiscal year 2025 due largely to restructuring charges associated with Chapter 11 proceedings [F1].

Chapter 11 Bankruptcy and Restructuring

In August 2025, Spirit filed voluntary petitions for relief under Chapter 11 citing liquidity challenges intensified by post-pandemic industry dynamics such as excess capacity and wage inflation undermining its ultra-low-cost structure [S3][S1]. Credit rating agencies downgraded the company’s ratings to D following the filing highlighting elevated credit risk [S6]. As of December 31, 2025, Spirit held cash and cash equivalents of approximately $273 million but faced current liabilities slightly exceeding current assets resulting in tight short-term liquidity [F1][S6].

The ongoing transformation plan initiated in 2024 seeks to reposition Spirit as a value carrier offering expanded premium products alongside affordable base fares [S1][S9]. This includes exiting over 200 unprofitable routes by end-2025 to focus capacity on profitable markets [S5][S15]. Early results show improvement in average fares compared to prior years though profitability remains elusive.

Business Model Nuances

Spirit targets primarily leisure travelers who prioritize price while seeking diverse travel options. Low base fares are supported by operational efficiencies including a single aircraft type fleet which simplifies training and maintenance [S9][S15]. Ancillary revenues from baggage fees, seat selection charges, subscription services like Spirit Saver$ Club®, branded credit cards linked to the Free Spirit Program®, and travel packages supplement ticket revenue [S9][S24].

Post-pandemic labor cost inflation and reduced fleet utilization have eroded margins relative to historical ultra-low-cost operations that relied heavily on high utilization levels [S1]. Additionally, Spirit’s lack of marketing alliances limits feed traffic common among legacy network carriers impacting competitiveness especially on international routes [S12].

Industry Competition & Regulatory Environment

The airline industry is highly competitive with Spirit’s largest network overlaps involving Southwest Airlines, Frontier Airlines, American Airlines, and Delta Air Lines competing aggressively on price or product breadth [S19]. Price discounting pressure is acute given nominal incremental costs once flights are scheduled.

Extensive regulatory oversight from FAA safety standards, DOT consumer protections including evolving rules around disabled passengers’ accommodations, TSA security protocols impose operational complexities and cost burdens [S10][S14][S25]. Recent regulatory developments concerning ancillary fee disclosures introduce further revenue mix uncertainties [S25]. Tariffs related to aircraft parts imports remain a risk factor affecting capital expenditures amid suspended EU-US trade agreements [S11].

Liquidity & Capital Allocation

At December 31, 2025 Spirit reported approximately $273 million in cash & equivalents against current liabilities slightly exceeding current assets yielding a current ratio of about 0.97—indicating constrained liquidity [F1]. No share buybacks occurred during fiscal year 2025 following minor repurchases earlier reflecting capital preservation amid insolvency proceedings [F1].

Equity was deeply negative at approximately minus $2.09 billion underscoring accumulated losses compounded by restructuring-related write-downs within bankruptcy context [F1]. Capital expenditures have declined from prior periods consistent with curtailed fleet expansion or refresh initiatives pending resolution of restructuring plans [F1].

Return metrics such as ROE are not meaningful given large net losses coupled with negative shareholder equity. Operating cash flow remains negative requiring continued emphasis on cost containment amid uncertain revenue trends.

Future Growth Prospects & Milestones

Spirit’s return to sustainable profitability depends critically on successful emergence from Chapter 11 reorganization pursuant to court-approved plans involving fleet downsizing and network optimization [S26][S16]. Key growth drivers include:

- Expansion of premium travel offerings targeting higher yield customers.

- Continued rationalization of route network focusing on profitable markets.

- Leveraging technology modernization efforts for improved operational efficiency including advanced revenue management systems.

- Growth of ancillary revenues through loyalty programs like Free Spirit and subscription models.

Risks include intense competition suppressing pricing power; regulatory uncertainties especially around ancillary fees; labor relations; fixed obligations related to aircraft leases/debt; economic cycles affecting discretionary travel demand; cybersecurity threats impacting reliance on automated systems; plus inherent uncertainties tied to restructuring outcomes [S16][S17][S29].

No explicit forward guidance or milestone dates beyond those associated with bankruptcy proceedings are disclosed publicly at this time; monitoring court developments alongside quarterly financial results will be essential for assessing turnaround progress.

Conclusion

Spirit Aviation Holdings stands at a pivotal juncture transitioning from an ultra-low-cost carrier toward a broader value proposition amidst significant financial distress shaped by its Chapter 11 filing. Its single-family Airbus fleet provides scale advantages while new premium offerings aim to broaden appeal. However, deeply negative earnings reflect pandemic aftermath disruptions combined with intense fare competition complicating near-term recovery.

Liquidity remains tight despite meaningful cash reserves; capital allocation prioritizes sustaining operations over shareholder returns which are currently nonexistent due to insolvency status. Regulatory compliance demands add complexity particularly regarding passenger experience mandates.

Investors should closely watch developments around reorganization confirmation alongside execution of network adjustments and premium product rollouts—these factors will materially influence whether Spirit can restore profitability and stabilize operations post-bankruptcy.

This analysis is based exclusively on publicly available data as of March 17, 2026 ([F1], SEC filings S1-S29). It is intended for informational purposes only without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments