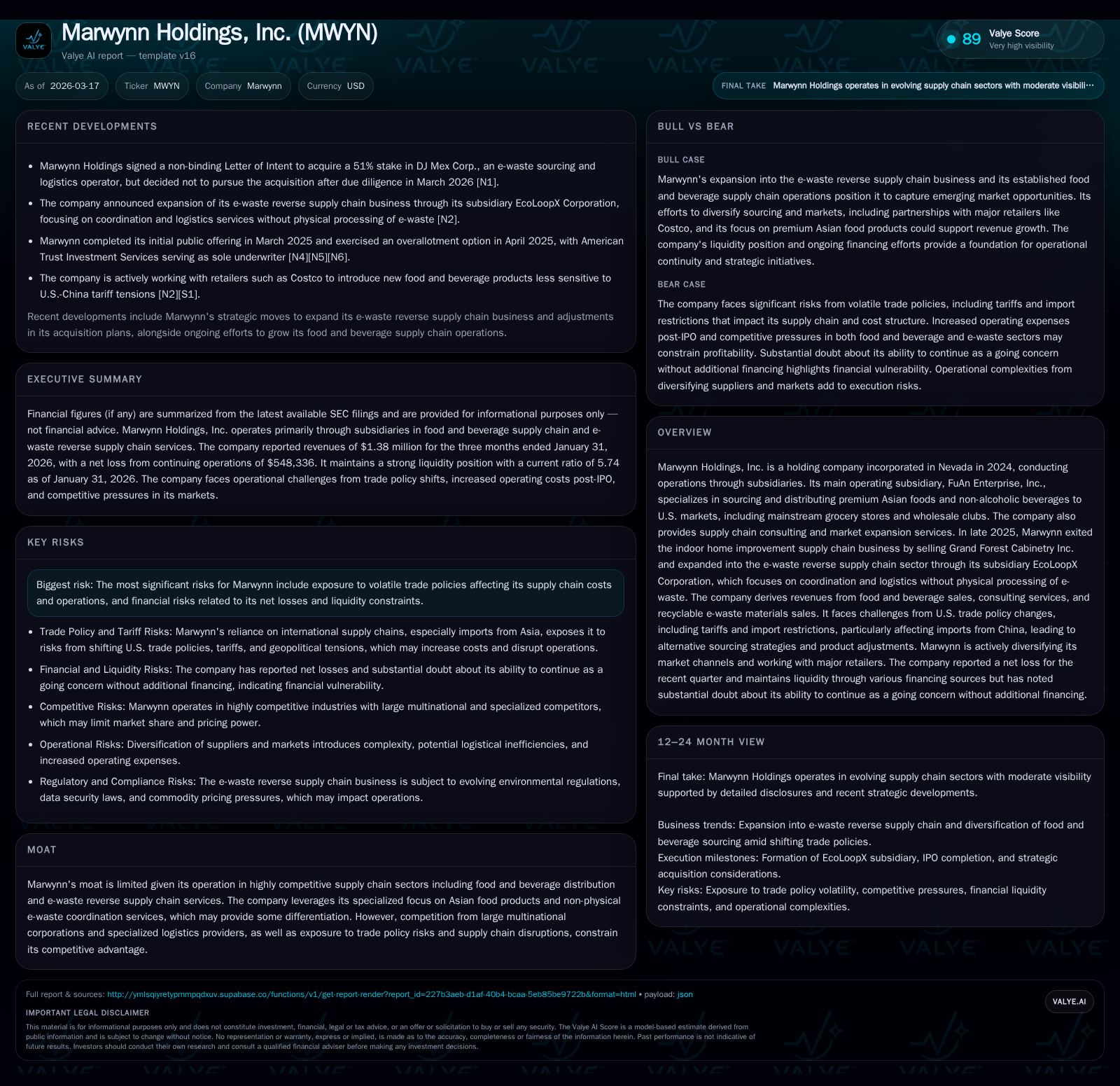

Marwynn Holdings’ Shift into E-Waste and Asian Food Supply Chains Tests Profitability Amid Rising Costs

Marwynn Holdings has restructured its operations toward recyclable e-waste coordination and Asian food distribution, driving revenue gains but widening net losses.

Marwynn Holdings, Inc., a holding company primarily operating through its subsidiary FuAn Enterprise, specializes in Asian food sourcing and distribution while recently expanding into e-waste reverse supply chain coordination via EcoLoopX. Revenues nearly doubled in the nine months ended January 31, 2026 compared to the prior year, driven mainly by a new e-waste materials sales segment with low gross margins. Elevated operating expenses caused net losses to widen to $4.16 million. Strategic divestitures like the sale of Grand Forest Cabinetry seek to streamline operations, but liquidity remains constrained amid continued negative operating cash flow.

Company Background and Operating Segments

Marwynn Holdings was incorporated in Nevada in February 2024 and operates primarily through subsidiaries including FuAn Enterprise (Asian food import/distribution) and EcoLoopX Corporation (e-waste reverse supply chain services). The company divested its indoor home improvement unit Grand Forest Cabinetry in late 2025 to concentrate on higher-growth segments [S2][S3][N1].

FuAn Enterprise sources premium Asian foods and non-alcoholic beverages targeting U.S. grocery stores and wholesale clubs while also providing supply chain consulting and market expansion support tailored for Asian branded goods [S2][S6].

EcoLoopX began operations in January 2026 focusing on reverse logistics coordination of discarded electronics without engaging in physical processing or recycling. Its value proposition centers on vendor coordination, compliance facilitation during evolving environmental regulations, documentation handling, and supporting circular economy platforms [S2][S7][S12].

Historical Performance Drivers

Although Marwynn's consolidated reporting is recent reflecting incorporation timing, quarterly data illustrate key trends:

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

*Annual figures from latest available annual snapshot [F1]

For the nine months ended January 31, 2026, revenues nearly doubled (+93%) versus prior-year periods largely due to new sales from recyclable e-waste materials totaling approximately $1 million [S6]. Sales from food and beverage declined about $285K during tariff-driven import challenges [S6][S14]. Consulting service revenues remained relatively steady but minor [S6].

Despite top-line growth driven by expansion into e-waste coordination services starting in early 2026 with low gross margins (~2.9%), overall gross profit declined nearly half year-over-year due to margin compression from this segment combined with reduced margins in food & beverage—from above 40% down to about 20%—impacted by loss of major retail accounts like Costco [S9][S14][S17].

Operating expenses surged: selling expenses rose over fourteen-fold due mainly to marketing campaigns and consulting engagements supporting business development across segments [S15][S17]. General & administrative expenses more than doubled driven by professional fees for financial advisory and legal matters related to disposals, new office rent costs, director compensation increases, and higher insurance expenses including directors & officers coverage—typical for newly public small companies [S11].

Consequently, net losses widened sharply to $4.16 million for the nine months ended January 31, 2026 compared with about $0.42 million last year—an almost tenfold increase primarily driven by rising operating costs exceeding gross profit gains [S19].

Future Growth Prospects

Marwynn's near-term growth depends on scaling its core Asian food supply chain services while expanding presence within the electronic waste reverse supply-chain ecosystem.

FuAn Enterprise: In response to U.S.-China trade policy volatility causing tariff uncertainties that have dampened some branded product imports especially for mass-market channels such as Costco, FuAn targets diversification through ethnic supermarket chains perceived as less tariff-sensitive markets. Vendor relationships with major food distributors have been established offering potential reach expansion if executed effectively [S6][S14].

EcoLoopX: The e-waste reverse supply chain is gaining importance amid tightening global regulations on discarded electronics’ environmental impacts. EcoLoopX focuses on logistics coordination and compliance support without physical recycling infrastructure investment but faces competition from large integrated waste management firms as well as specialized niche providers [S7][S14]. Growth will require deeper market penetration and capturing fee streams amid increasing legislative compliance demand.

In February 2026 Marwynn signed a non-binding Letter of Intent to acquire a majority stake in DJ Mex Corp., a U.S.-based electronic waste operator aimed at expanding EcoLoopX’s platform capabilities—signaling intent for inorganic growth though integration risks remain [N1].

Financial Expectations & Milestones

No explicit forward guidance is provided; governance commentary highlights prioritizing revenue growth at FuAn via channel expansion alongside business development initiatives supporting EcoLoopX including acquisition activities [N1][S2][S3]. These align with strategic divestitures like Grand Forest Cabinetry’s sale executed late last year intended to focus resources on higher-margin areas.

Key metrics include monitoring quarterly revenue ramp from ethnic supermarket penetration for Asian foods alongside vendor contract expansions at EcoLoopX plus margin improvements if cost synergies materialize post-acquisition.

Attention should also be given to evolving U.S. trade policies affecting tariffs directly influencing FuAn’s sourcing costs and pricing strategies [S12][S14], as well as regulatory developments impacting e-waste handling potentially affecting EcoLoopX’s operational model.

Returns & Capital Allocation Review

Marwynn has reported consistent net losses since listing—with an approximate return on equity of -88.5% based on latest annual data—reflecting early-stage expansion investments required for scaling operations [F1]. Net cash used in operations was about $1.3 million for the nine months ended January 31, 2026 creating liquidity pressures despite financing inflows exceeding $1.6 million likely from stock issuances or related party borrowings [F1][S4][S10].

Cash balances were roughly $0.30 million at period end with working capital positive at approximately $2.15 million supported by modest current liabilities indicating dependence on fresh equity or debt alongside operational improvements for sustainability [F1][S4]. No dividends or share repurchases have been declared or are feasible given cash constraints.

Competitive Position & Moat Analysis

Marwynn operates amid intense competition: large multinational distributors dominate mainstream Asian food imports while dedicated players compete aggressively for retail shelf space across consumer segments [S7][S14]. The reverse e-waste logistics field includes major solid waste companies integrating recycling solutions with proprietary logistics platforms alongside regional niche operators focused on compliance contracts.

Marwynn’s competitive differentiation lies partly in exclusive focus on premium Asian foods combined with an asset-light approach in its e-waste segment avoiding costly physical processing infrastructure while investing in coordination capabilities—a strategic tradeoff limiting capital expenditure risk but compressing margins [N1][S7]. Success depends heavily on execution agility amid regulatory changes and effective vendor network scaling.

Risks Highlighted by Management

Management identifies significant risks from volatile trade tariffs affecting import pricing structures that impair reliable cost forecasting impacting competitiveness of their Asian food segment products [S7][S12]. Liquidity risk is material due to persistent negative operating cash flows coupled with rising expenses associated with Nasdaq listing including audit fees and compliance costs [S8][S10]. Environmental regulation shifts around electronic waste add complexity exposing EcoLoopX operations to compliance costs or volume limitations if licensing requirements tighten unexpectedly.

Conclusion & Monitoring Points (Analysis)

Marwynn Holdings stands at an inflection point balancing aggressive repositioning within two highly competitive verticals: specialty Asian food import/distribution challenged by geopolitical tariff volatility; and a nascent non-asset-intensive reverse e-waste coordination business seeking market traction against established recyclers.

Near-term financials indicate substantial cash burn risking solvency pressure absent successful revenue ramping combined with tight cost control measures going forward. Key operational milestones include expanded ethnic supermarket partnerships at FuAn plus commercial progress post-DJ Mex acquisition within EcoLoopX.

Investors should monitor:

- Quarterly revenue composition shifts particularly ethnic channel growth versus legacy mass market exposures.

- Margin trends reflecting dilution from low-margin recyclable material sales.

- Cash flow dynamics alongside any announced equity or debt financing aimed at relieving liquidity strains.

- Regulatory developments affecting cross-border tariffs alongside evolving electronic waste standards.

- Integration progress of acquisitions enhancing multi-service circular economy platforms.

This strategic recalibration offers synergy potential but faces execution risks with elevated costs depressing profitability metrics requiring rigorous oversight.

This analysis is based solely on reported company filings and publicly available information as of March 2026; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments