Corvus Pharmaceuticals Advances Immune-Targeted Therapies Despite Ongoing Losses

The clinical-stage biopharmaceutical company balances intensified R&D and collaboration-driven innovation against sustained financial deficits in 2025.

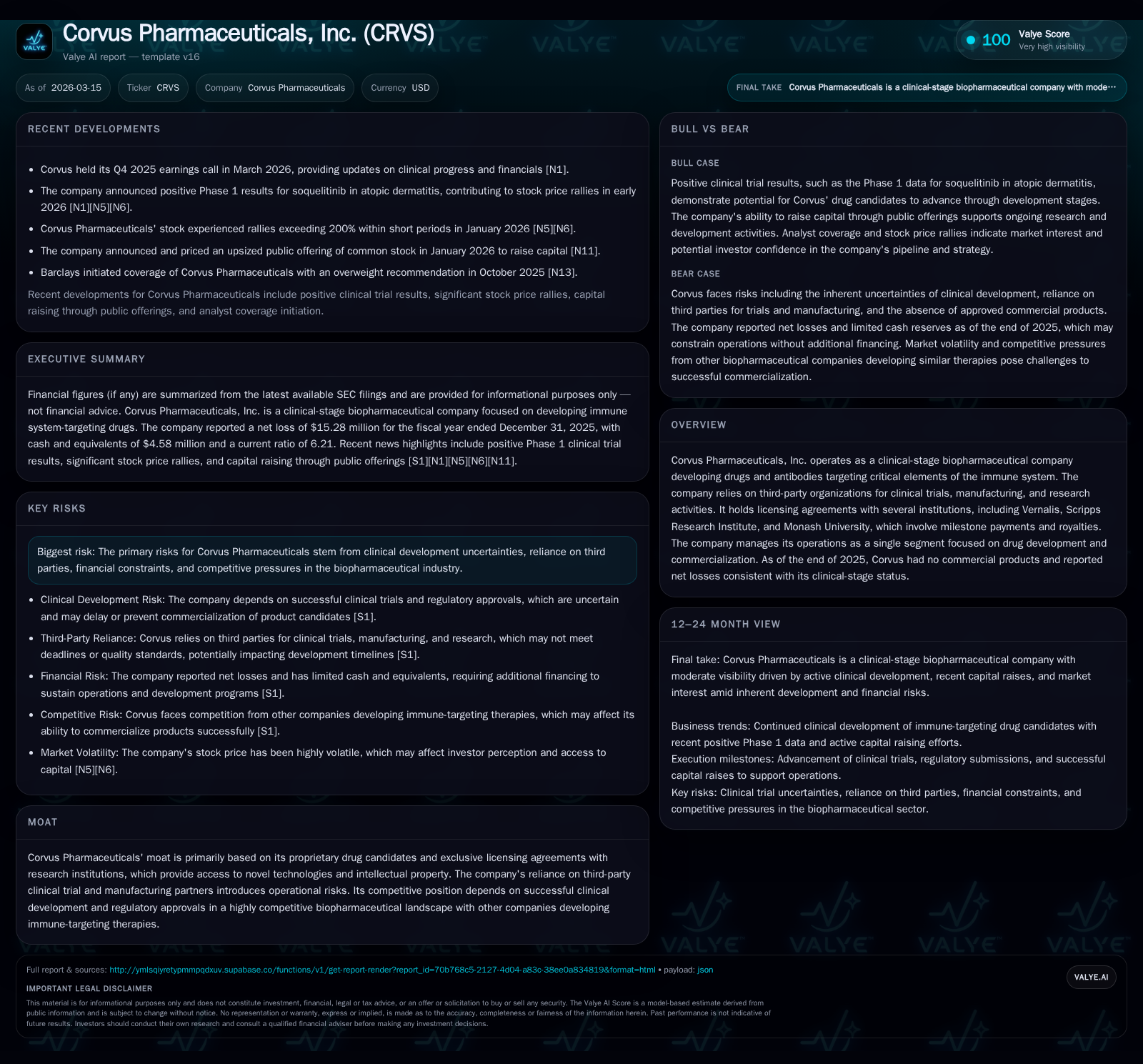

Corvus Pharmaceuticals remains firmly in clinical-stage development with no commercial products as of 2025, focusing on immune-targeted therapies through internal R&D and external licensing arrangements. Despite a near 56% increase in operating losses year-over-year, the company has strengthened its liquidity position, maintaining a current ratio above six through significant cash and marketable securities. Critical upcoming milestones include continued clinical trial progress for key candidates like ciforadenant and mupadolimab, while the strategic amended sales agreement with Jefferies boosts capital raising flexibility amid competitive market pressures.

Trend Analysis of Corvus’ Operating and Net Losses Over Recent Years

Corvus Pharmaceuticals remains a clinical-stage biopharmaceutical entity focused exclusively on drug development without any commercial products yet to generate revenue [S1]. The company's historical income statement highlights significant operating losses that reflect both intensive R&D expenditures and accounting impacts related to licensing milestone payments. In FY2025, Corvus reported an operating loss of approximately -$42.97 million, representing nearly a 56% deepening versus the prior year’s -$27.55 million [F1]. This sharp increase underscores growing operational expenditures likely tied to advancing multiple clinical programs.

Interestingly, net income improved notably from a -$62.29 million loss in FY2024 to -$15.28 million in FY2025 [F1]. This discrepancy between operating losses and net income reflects non-operational factors such as changes in warrant liabilities or reverse milestone payment effects impacting overall profitability.

Despite continuing negative cash flows from operating activities, which worsened by circa 29% year-over-year to -$32.79 million in FY2025 [F1], Corvus has managed to contain capital expenses at relatively low absolute levels (about $174,000) though rising over fourfold from prior years [F1]. This spending profile is consistent with outsourcing clinical trial execution rather than heavy fixed asset accumulation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -15 | -33 | -43 | 174000 | +75.5% |

| 2024 | -62 | -25 | -28 | 34000 | -130.5% |

| 2023 | -27 | -24 | -23 | 34000 | |

| 2021 | -41 | -27 | -33 | 269000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -33 | -25.0 |

| 2024 | -25 | -191.3 |

| 2023 | -24 | -69.9 |

| 2021 | -27 | -73.6 |

Source: SEC companyfacts cache [F1].

Operating leverage is evident as increased R&D spend and milestone-related payments swell operating losses despite some improvement in net outcomes[F1].

Third-Party Collaborations and Licensing: Pillars of Innovation and Risk Management

Corvus’s operational model is heavily dependent on sophisticated third-party collaborations that provide critical access to proprietary immuno-oncology technology platforms while outsourcing costly clinical trials and manufacturing processes [S1][N1]. Among its most strategically important license agreements are those with Vernalis plc for adenosine receptor antagonists particularly ciforadenant; Scripps Research Institute; and Monash University [S14][S15]. These agreements grant Corvus exclusive global rights subject to upfront fees, milestone payment obligations, royalties on sales ranging from low single digits up through certain sublicensing revenues at double-digit percentages initially [S14].

Milestone payments represent key contingent liabilities impacting operating results unpredictably depending on clinical trial progress or licensing events achieved [N1][S14]. For example, no milestones owing to Monash were triggered in 2025 though aggregate potential milestones stood at $45.1 million at year-end [S14]. The reliance on outside parties for manufacturing and clinical research also introduces risks around timing delays or quality control failures that could disrupt development timelines considerably.

This partnership-centric strategy positions Corvus competitively by leveraging cutting-edge immune system targets without incurring fixed infrastructure burdens but also compounds exposure to execution risks endemic within outsourced biopharma development [S15].

Clinical Trial Progress and Its Impact on Growth Prospects

Corvus's therapeutic focus centers on modulating critical immune pathways implicated in oncology. Key candidates include soquelitinib—a kinase inhibitor; ciforadenant—an orally administered selective A2A receptor antagonist intended for solid tumor therapies; and mupadolimab—a humanized monoclonal antibody targeting CD73 implicated in tumor-induced immunosuppression [S2][N1].

The clinical-stage characterization reflects that none of these therapies has received final regulatory approval; each remains subject to complex phased testing under stringent FDA oversight prior to commercialization eligibility [S14]. Recent quarterly disclosures emphasize ongoing patient enrollment expansions and regulatory interactions designed to refine efficacy endpoints [N1][S2]. Successful progression through Phase II/III studies would open pathways toward potential revenue generation but faces inherent biological uncertainties common across immuno-oncology drug development.

Corvus also aims to differentiate via molecular specificity within the adenosine signaling pathways—a competitive niche explored by others such as Arcus Biosciences and AstraZeneca's anti-CD73 programs—which heightens the urgency regarding intellectual property protections linked to licensed compounds [S15][S25].

Pipeline Bottlenecks and Industry Competition Influencing Future Development

Regulatory approval uncertainties create fundamental bottlenecks that may delay milestone realization or lead to program terminations if safety or efficacy targets are unmet [S14][S15]. Competition from larger peers wielding greater capital resources not only raises challenges around patent enforcement but also intensifies race conditions within overlapping immuno-oncology indications where speed-to-market is a key determinant.

Investors should note disclosure warnings about possible patent litigation scenarios or invalidation risks that could curtail exclusivity periods overall diminishing long-term returns even if clinical successes materialize [S15]. Moreover, crowded trial landscapes necessitate robust design innovations including adaptive protocols or biomarker stratification techniques increasingly becoming standard practice within successful cancer immunotherapy developers.

Financial Health Snapshot: Liquidity, Capital Structure, and Risk Exposure

As of December 31, 2025, Corvus reported total current assets of $58.21 million against $9.38 million in current liabilities indicating a sturdy current ratio approximating 6.21x—comfortably exceeding typical liquidity thresholds for biotech firms at similar maturity stages [F1][S4][S7]. This strong liquidity buffer primarily comes from cash and marketable securities aggregating roughly $57.4 million combined with nominal accounts receivable balances primarily related to related party transactions [S20][S26].

Total liabilities were relatively low at approximately $8.7 million underscoring modest debt footprint and limited leverage exposure relative to equity base measured at $61.2 million as of year-end [F1][S4]. Nonetheless the company’s negative free cash flow (-$32.98 million derived CFO minus capex) evidences ongoing capital consumption consistent with advanced stage R&D programs underway [F1].

The recent amended Open Market Sale Agreement executed with Jefferies LLC enhances flexibility for equity issuance enabling opportunistic capital raises aligned with market conditions – a critical instrument given absence of significant recurring revenues presently and dependence on funding continuity for operational sustainability [N1][S3].

Evaluating Capital Allocation: Investment in R&D Versus Returns to Shareholders

R&D expenditure constitutes the dominant use of Corvus’s financial resources with capex remaining minimal at under $200k annually—typical for clinical-stage biotech deploying third-party manufacturing rather than facility build-outs [F1][S24]. This indicates efficient capital deployment focused on advancing drug candidates through trials rather than asset-heavy investments.

Dividend distributions or share repurchases are absent reflecting prudent retention strategy to conserve cash amid continued operating losses coupled with modest equity base growth over time [F1]. Return on equity stands negative at roughly -25%, illustrating typical biopharmaceutical startup conditions pre-commercialization where losses dominate until product approvals unlock scalable returns.

Operational leverage remains a central theme — larger investments currently translate into expanded exploratory activity but exacerbate reported losses before eventual product maturation alters financial trajectories radically.

Analyst Perspectives: Milestones to Monitor Following Q4 2025 Earnings

Post-Q4 discussions spotlight several pivotal near-term catalysts: data readouts linked to Phase II trials particularly ciforadenant’s efficacy signatures across solid tumors; milestone advancements triggering license fee payments; regulatory interactions clarifying potential accelerated approval pathways; plus expanding patient recruitment metrics crucial for maintaining trial timelines [N1][N2].

Market watchers emphasize sensitivity around potential delays or adverse findings which would materially depress valuation prospects whereas positive surprises could de-risk pipeline substantially attracting partnership interests or acquisition dialogues.

Strategic Implications of the Amended Open Market Sale Agreement with Jefferies LLC

The amended ATM sale agreement reconfigured terms allowing Corvus increased flexibility in raising common stock proceeds incrementally tied closely to stock price movements via Jefferies' placement capabilities without immediate dilutive bulk offerings [N1][S3]. This mechanism can serve as a tactical cash management tool buffering against unexpected R&D overruns or extended trial durations.

While this facility broadens fundraising options supporting operational continuity over coming quarters it may impose an overhang on share price performance if material drawdowns occur unexpectedly thus demanding careful communication management towards investors regarding funding needs.

Disclaimer: This analysis is provided for informational purposes only based on available public disclosures as of March 15, 2026. It does not constitute investment advice nor recommendations regarding buying or selling securities of Corvus Pharmaceuticals or any other entity. Readers should perform their own due diligence before making financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments