Esquire Financial Holdings' Litigation-Focused Banking Yields Strong Returns with Technology-Driven Growth

The company’s niche in litigation-related lending and payment processing underpins superior profitability and client retention amid concentrated credit risks.

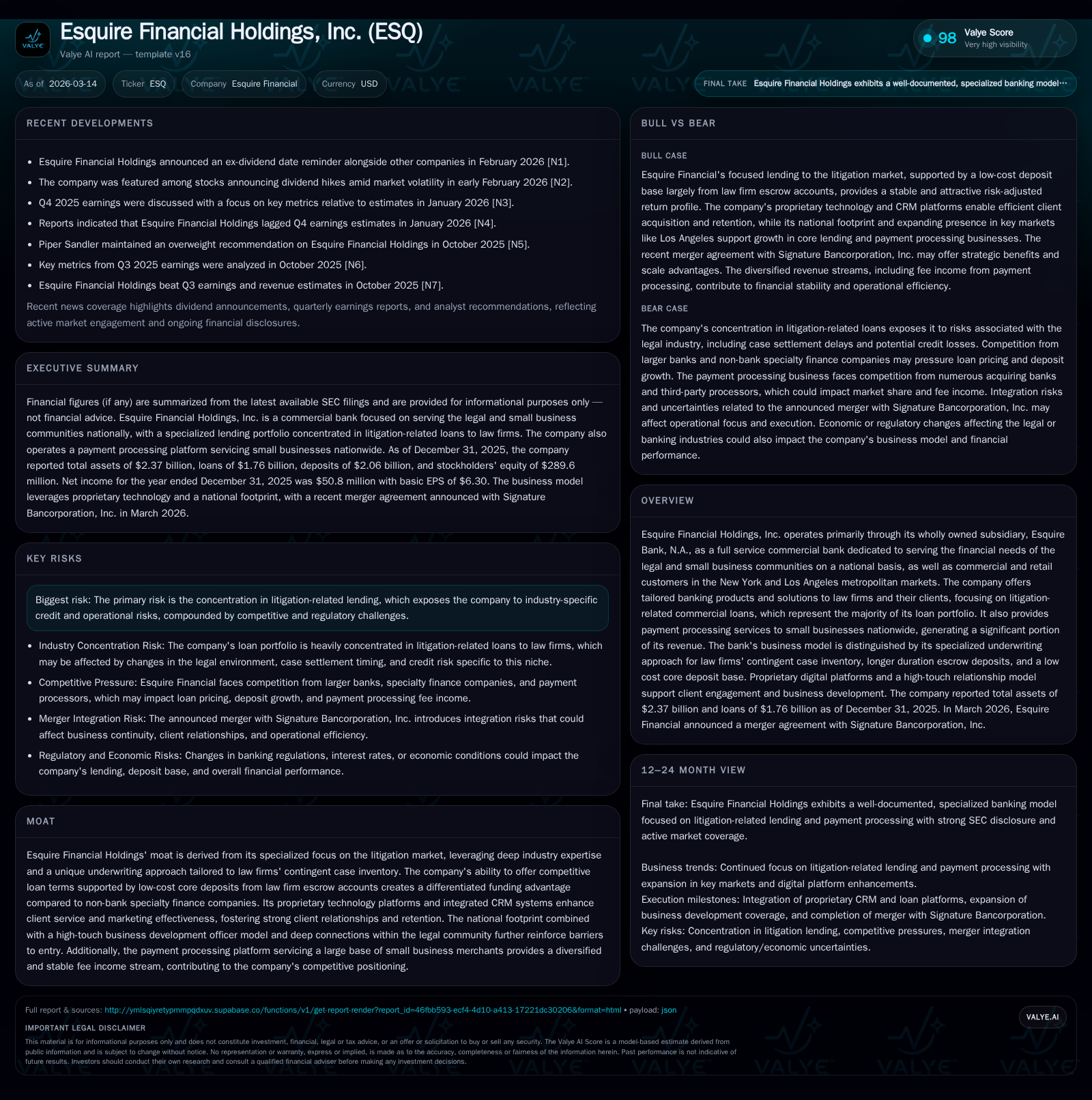

Esquire Financial Holdings, operating primarily through Esquire Bank, distinguishes itself by specializing in litigation market lending and small business payment processing. The firm's unique underwriting of law firms’ contingent case inventory, combined with a low-cost deposit base from escrow accounts, supports strong margins and returns. With net income growing 16.4% in 2025 to $50.8 million [F1], Esquire leverages proprietary digital platforms and a high-touch business development model to deepen client relationships nationwide. However, its concentrated exposure to the litigation sector elevates credit and operational risk profiles, necessitating close monitoring of loan quality and regulatory developments.

Company Overview

Esquire Financial Holdings, Inc., through its wholly owned subsidiary Esquire Bank, operates as a full-service commercial bank with a highly specialized lending focus on the legal community across the United States. The firm targets law firms engaged predominantly in litigation, providing tailored credit products that emphasize underwriting based on contingent case inventory — a distinctive feature that governs the majority of its loan portfolio.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 51 | 60 | 3 | +16.4% |

| 2024 | 44 | 42 | 1 | +6.5% |

| 2023 | 41 | 42 | 1 | +43.8% |

| 2022 | 29 | 39 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 286000 | 57 |

| 2024 | 5 | 286000 | 41 |

| 2023 | 4 | 286000 | 42 |

| 2022 | 2 | 567000 | 39 |

Source: SEC companyfacts cache [F1].

Besides lending, Esquire has developed a substantial payment processing platform serving approximately 93,000 small business merchants nationally, contributing significant fee income to revenue streams.

The company’s operational backbone includes proprietary digital platforms powered by advanced CRM technologies on Salesforce and nCino foundations that facilitate highly personalized client outreach supported by business development officers embedded regionally around key markets like New York and Los Angeles.

Historical Performance

Esquire's financial trajectory has been marked by consistent growth driven by expansion within its core litigation lending segment alongside diversification into payment processing services. Between fiscal years 2022 and 2025, net income advanced from approximately $28.5 million to $50.8 million — a compound annual growth rate reflecting operational leverage amid expanding loan balances and stable margins [F1]. Operating cash flow followed an accelerating trend into late 2025 with a notable rise of nearly 42% year-over-year.

| FY | Net Income ($M) | Operating Cash Flow ($M) | Capex ($M) | Equity ($M) | Dividends Paid ($M) |

|---|---|---|---|---|---|

| 2022 | 28.52 | 38.80 | 0.07 | 158.16 | 2.15 |

| 2023 | 41.01 | 42.40 | 0.61 | 198.56 | 3.72 |

| 2024 | 43.66 | 42.21 | 0.71 | 237.09 | 4.85 |

| 2025 | 50.82 | 59.84 | 3.16 | 289.60 | 5.86 |

Operating efficiency remains robust as reflected by an industry-leading net interest margin reported around 6%, paired with a commendable efficiency ratio near mid-40%s reflecting cost discipline especially given the investment into technology platforms enhancing scaling opportunities [S6].

Business Model Nuances & Loan Portfolio

The litigation-related commercial loans account for approximately two-thirds (67%) of the total loan portfolio as of December 31, 2025 [S6][S8]. This category includes working capital lines of credit (66%), case cost lines of credit (18%), and term loans (16%) extended primarily to law firms nationwide with concentrations in California (20%), New York (17%), and Texas (14%) [S7][S8][S10].

What differentiates Esquire's approach is integrating traditional commercial underwriting with asset-based assessments framed against law firms’ contingent case inventories — claims expected to resolve generally within two to four years — allowing them to price accordingly for longer durations than typical receivables financing [S7]. Furthermore, their cost of funds benefits significantly from low-rate escrow deposits where law firms act as trustees for claimant settlement funds amounting to approximately $1.23 billion or about 60% of total deposits carrying pass-through FDIC insurance benefits at claimant levels rather than the trust account level itself [S7][S16].

Alongside this specialized lending sphere, real estate loans representing roughly 28% of loans focus mostly on conservative multifamily assets within New York metropolitan corridors with fixed amortizing terms enhancing stability amidst potential economic fluctuations [S8].

The payment processing segment complements lending activities by generating stable fee income (~14% of revenues) derived from thousands of merchants acquired mainly through third-party ISOs leveraging an acquiring bank model that mitigates merchant credit risk through multiple reserve mechanisms [S9][S16]. The platform processes approximately $40 billion annually across roughly half a billion transactions demonstrating scale potential.

Growth Prospects and Strategic Initiatives

Future expansion hinges prominently on deepening penetration within underserved regions beyond existing hubs like New York City, Los Angeles, and Texas leveraging enhanced digital marketing tools including AI-driven personalization integrated into CRM systems propelling lead generation effectiveness for their BDO network nationally [S6][S13][S16].

Expansion of payment processing volumes through further ISO partnerships presents additional avenues for recurring fee income growth supported by unique service offerings tailored toward small business needs across verticals.

Notably, Esquire announced a merger agreement with Signature Bancorporation in early March of 2026 which could reshape scale dynamics and geographic reach depending on integration execution; details remain forthcoming but represent a key milestone for investors to monitor closely regarding strategic fit and regulatory approvals [N1][S11].

Risks and Constraints

Chief among risks is the concentrated exposure to the litigation market which inherently entails credit risk tied to legal industry cycles plus regulatory complexities governing trust accounts and contingent claim financing—areas where new entrants find formidable barriers but also where adverse outcomes or slowing lawsuit activity could impact asset quality materially [S14][S15].

Competition arises not only from traditional community banks but also increasingly aggressive specialty finance companies targeting similar clientele albeit often lacking banking licenses which constrains their product suite compared to Esquire’s full-service offerings including deposit services that non-banks cannot replicate easily [S15].

Economic conditions influencing real estate valuations—especially within multifamily segments dominating their collateral pool—also impose concentration risk factors requiring ongoing vigilance.

Capital Allocation and Returns

Esquire delivers healthy returns exemplified by an approximate return on equity nearing 17–18% in fiscal year ending December 31, 2025 derived from strong net income relative to shareholder equity totaling $289.6 million at year-end [F1].

Free cash flow generation remains robust at around $56.7 million after accounting for modest capital expenditures focused mainly on technological enhancements scaling from prior years’ investments [F1]. Strong operating cash flows support increasing dividends which have risen consistently from $2.15 million in FY2022 to almost $6 million in FY2025 reflecting management’s commitment to returning capital while cautiously maintaining balance sheet strength amid growth phases [F1][N2][N3]. Share repurchases are minimal but steady at low hundreds of thousands per annum indicating prioritization of dividend yield plus organic reinvestment over aggressive buybacks currently.

What to Watch

Absent explicit forward guidance in filings or announcements beyond the merger agreement, key milestones would include regulatory clearance timing for the Signature transaction along with quarterly updates on loan portfolio performance particularly delinquency trends within litigation-related credits amid any changing judicial climates or macroeconomic pressures.

Payment processing adoption rates vis-à-vis merchant churn metrics coupled with incremental contributions from newly onboarded ISOs also warrant attention as indicators of sustainable fee income growth.

Finally, management’s ability to leverage proprietary digital initiatives effectively while maintaining credit discipline will be critical to uphold historical profitability levels given sector concentration risks.

This analysis synthesizes publicly available SEC filings up through early March 2026 alongside recent news reports reflecting analyst perceptions without making investment recommendations or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments