Genvor Inc’s AI-Driven Peptide Platform Faces Scale-Up and Commercialization Challenges

Genvor Inc leverages proprietary AI technology to develop sustainable agricultural peptides but remains in early financial stages with key regulatory and partnership milestones ahead.

Genvor Inc pioneers AI-accelerated peptide discovery targeting crop protection, yield enhancement, and animal health through a licensing-driven business model focused on sustainability. Despite a compelling technology platform validated by USDA collaborations and peer-reviewed publications, the company has generated no revenue to date and operates with persistent operating losses and negative equity. Future growth hinges on regulatory approvals, strategic partnerships, and broad adoption of its novel peptide solutions amid a competitive landscape of biological crop protection innovators.

Historical Performance

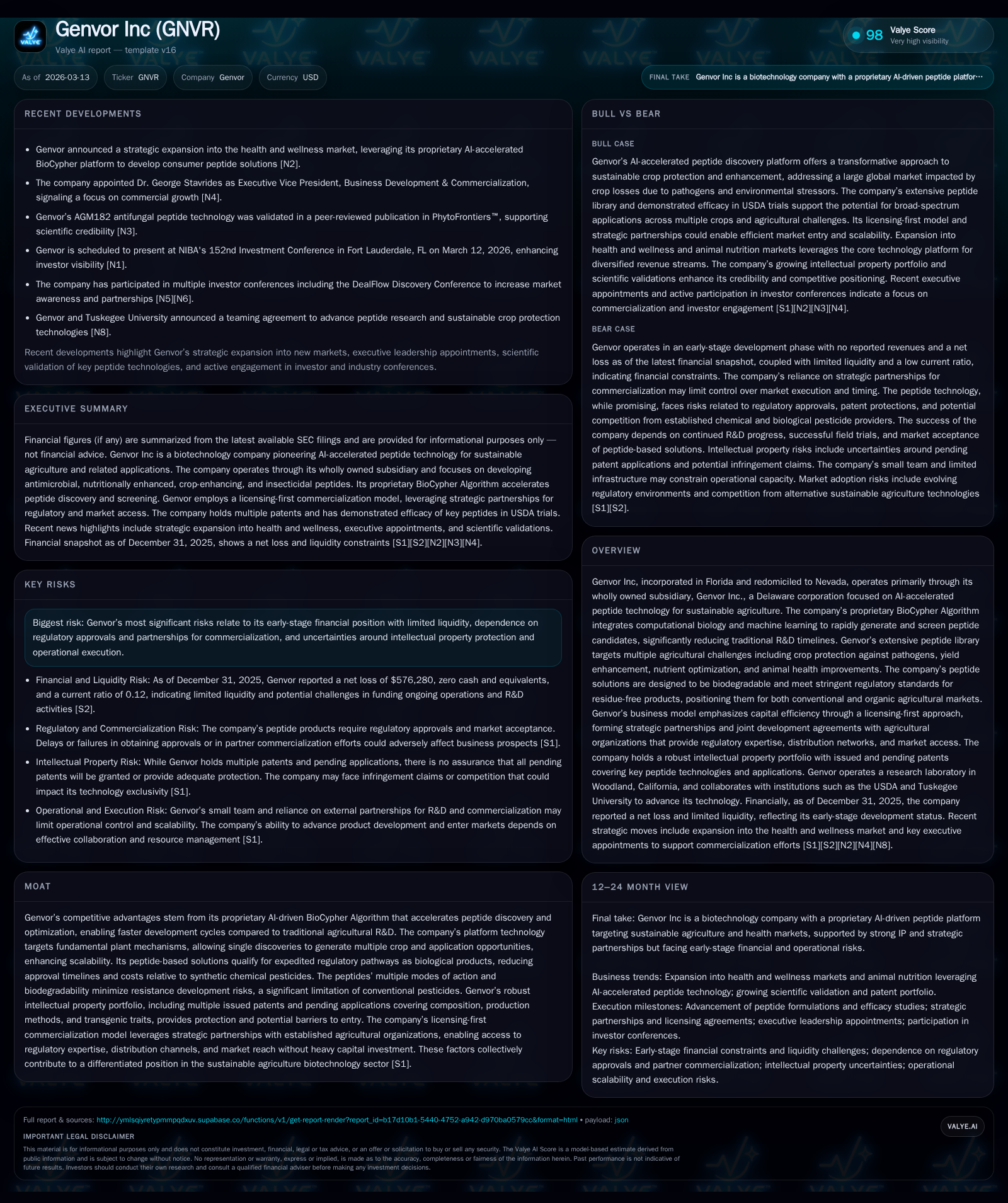

Genvor Inc is an early-stage biotechnology company focused on AI-driven peptide technology for sustainable agriculture, operating primarily through its wholly owned Delaware subsidiary [S1][S3]. Since inception, the company has not recorded any revenue, reflecting its pre-commercial stage. According to the latest reported figures as of September 30, 2025, Genvor’s revenues remain at zero [F1]. Over the past four fiscal years (FY2022–FY2025), operating losses have steadily increased—from approximately -$1.44 million in FY2023 to nearly -$6.41 million (TTM) in FY2025—indicating accelerating investment in R&D and operations without offsetting monetization [F1]. Net losses mirror this trajectory, with FY2025 net income at approximately -$5.59 million, a nearly 94% increase in absolute losses compared to prior year [F1]. Operating cash flow is also negative but slightly improved year over year (-$555k CFO in FY2025 vs. -$976k prior year), possibly reflecting tighter cost controls or timing differences. The company’s balance sheet reflects ongoing liquidity challenges; current assets totaled just $146k against current liabilities of over $1.2 million as of December 31, 2025—a current ratio of 0.12—indicating limited short-term financial flexibility [F1][S18]. Equity is negative at approximately -$1.31 million [F1], underscoring accumulated losses exceeding invested capital.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -6 | -555717 | -6 | -93.7% |

| 2024 | -3 | -975641 | -3 | -69.0% |

| 2023 | -2 | -871734 | -1 | +59.7% |

| 2022 | -4 | -553236 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 425.9 |

| 2024 | 168.3 |

| 2023 | 100.1 |

| 2022 | 304.1 |

Source: SEC companyfacts cache [F1].

Table: Key financial metrics from FY2022 to FY2025 latest available quarterly data as reported [F1]

Technology Platform and Business Model

Genvor’s core innovation lies within its proprietary BioCypher Algorithm—a machine learning driven computational biology platform integrating over 9,000 synthetic antimicrobial peptides alongside natural AMP data to accelerate peptide discovery and design [S11][S13]. This approach enables rapid in silico generation and screening of over 100,000 candidate peptides with predictive scoring algorithms that reduce laboratory validation work by over three orders of magnitude versus traditional methods [S11][S13]. The peptide library targets multiple critical agricultural domains:

- Antimicrobial peptides (AMPs) combat broad-spectrum fungal (e.g., Aspergillus flavus, Botrytis cinerea), bacterial and viral pathogens threatening crops worldwide.

- Nutritionally Enhanced Peptides (NEPs) aim to improve nutrient uptake and utilization enhancing yields while potentially reducing fertilizer needs.

- Crop Enhancing Peptides (CEPs) improve plant resilience to abiotic stressors such as drought.

- Animal health peptides targeting improved feed conversion ratios in poultry, swine and aquaculture sectors [S11][S16].

Genvor develops these peptides as both transgenic seed traits—embedding AMPs directly into plant genomes—and topical foliar sprays classified as biological pesticides which benefit from expedited regulation pathways versus chemical pesticides [S10][S16][S26]. This bifurcated approach offers near-term entry via foliar biofungicides alongside longer-term potential from integrated seed traits with broader crop coverage.

The company employs a capital-efficient licensing-first business model that leans on strategic partnerships with established agricultural entities possessing regulatory expertise and distribution networks rather than direct commercialization [S3][S10]. Collaboration under Cooperative Research and Development Agreements (CRADAs) with the U.S. Department of Agriculture substantially reduces R&D overhead by leveraging public labs for field trials and regulatory data generation; notably Genvor’s AGM182 transgenic corn peptide reduced aflatoxin contamination by up to 98% in USDA trials—a key validation milestone [S11][S16][S19]. Partnerships thus enable Genvor to outsource expensive field testing and complex registrations while concentrating internal efforts on platform advancement.

Competitive Positioning

Within the burgeoning agricultural biologicals market—valued near $9.5 billion in 2019 growing toward $20 billion by mid-decade—Genvor’s platform stands out due to several competitive advantages:

- Proprietary AI-enabled discovery compresses development cycles radically below industry norms where seed trait launches typically require upwards of eight years and over $136 million capital investment absent CRADA support [S13][S19].

- Peptide solutions feature multiple modes of action combined with biodegradability that mitigate resistance development common in chemical pesticide classes.

- Issued patents protecting composition of matter covering critical disease-targeting peptides as well as production methods reinforce IP moat across key jurisdictions including the U.S., Canada Mexico and China with patent expiries through 2038 [S14][S24].

- Registered trademarks solidify brand identity (“GENVOR PEPTIDES BY DESIGN®”) signaling technological sophistication in the marketplace.

Competitors such as Vestaron Corporation also develop peptide-based bioinsecticides but generally lack Genvor’s breadth across fungal pathogens or the integrated AI platform behind candidate generation. Others focus narrowly on single crop or pest targets rather than Genvor’s multipronged cross-crop approach covering both seed traits and spray formulations [S4][S14].

Growth Prospects and Risks

Growth Drivers:

- Advancing greenhouse and field trials toward regulatory submission remains pivotal for near-to-mid-term commercialization potential; strong antifungal efficacy data supports imminent EPA biological pesticide filings expected within coming quarters [N3][S18][S20].

- USDA CRADA extension facilitates further refinement of next-generation AMPs such as GNV-185 and GNV-187 aimed at enhancing commercial viability by cost-effective scale manufacturing [S5][N3].

- Expansion into consumer health peptides leveraging BioCypher’s AI platform signals strategic diversification beyond agriculture which may open adjacent markets for peptide applications though remains early-stage [N1].

- License deal announcements or joint ventures with agricultural conglomerates will be key indicators signaling transition from R&D focus toward revenue generation [N2][S3].

Constraints & Risks:

- Financially constrained with minimal current assets against sizable liabilities necessitating imminent capital raises or partnership deals to avoid liquidity crises before generating revenue streams [F1][S18].

- Heavy reliance on external partners’ regulatory competence delays direct control over market entry timing; failed or delayed approvals could severely dampen growth prospects.[S17][S23]

- Intellectual property risks include pending patent applications where prosecution outcomes could influence breadth of protection[N4]; also risk of litigation from IP infringements inherent in biotech space remains non-trivial.

- Execution risk looms related to scaling manufacturing processes for novel peptides at commercial volumes cost-effectively—particularly delicate given low headcount concentrated principally at Woodland California lab under Bayer-supported lease through mid-2026[S12][S22]. -Negative equity position entails investor dilution risk if substantial new share issuances are employed to fund working capital needs.[F1]

Capital Allocation & Returns

Genvor currently does not distribute dividends nor engage in share repurchase programs consistent with standard biotech commercialization timelines focused on reinvestment over shareholder returns at this stage of development.[S6][F1] Capital allocation emphasizes funding internal R&D activity (~under $700k contributed annually toward USDA projects), leveraging third-party resources via CRADAs and partnerships to maintain lean overhead.[S5][S19]

With cumulative net losses increasing sharply reflecting steepening operating expenses from intensified trial activities and platform development,[F1] free cash flow remains negative albeit modestly improving from prior years narrowing losses by approximate operating cash flow figures (-$556k CFO in FY2025). The company has minimal physical assets but valuable intangible assets represented by IP portfolio underpinning future monetization opportunities.[F1]

Return on equity calculated loosely from the latest annual net loss divided by negative equity yields anomalous figures (+425%) which merely reflect the accounting effect of accumulated deficits.[F1] Genuine economic returns await successful product launch phases yet to materialize.

Key Upcoming Milestones & Monitoring Points

Investors following Genvor should track important forthcoming developments including:

- Progress reports from ongoing greenhouse and field efficacy trials for both seed traits (e.g., AGM182 derivatives) and topical biopesticides,

- Regulatory submissions notably EPA registration filings for biofungicide sprays allowing commercial sales,

- Announcements regarding expanded CRADA agreements or similar government partnerships enhancing research bandwidth,

- Strategic licensing agreements or joint ventures accelerating market reach,

- Any liquidity events such as equity financings aimed at bolstering working capital,

- Updates on patents granted or contested shaping competitive barriers,

- Commercial rollout plans post-regulatory approval focusing on customer adoption scenarios,

- Expansion updates related to consumer peptide segment introduced early March 2026[N1].

Conclusion

Genvor Inc sits at an early yet critical stage within the specialized niche of AI-driven sustainable agricultural biotechnology. Its pioneering BioCypher Algorithm delivers a compelling solution to longstanding challenges afflicting global food security through multifunctional peptide platforms protecting crops and enhancing yields sustainably. Despite significant scientific validation including peer-reviewed publications and USDA collaborations demonstrating promising antifungal results powering confidence in commercial applicability,the company currently operates without revenue amidst growing operating deficits compounded by tight liquidity positions.

The chosen capital-efficient licensing model leverages partnerships reducing overhead but introduces execution dependencies on external regulatory expertise and distribution infrastructures ahead of inevitable scale-up hurdles typical for disruptive biotech firms transitioning toward commercial maturity. Intellectual property protections further defend its innovations although patent application uncertainties persist alongside latent litigation risks embedded in high-tech life sciences sectors.

Ultimately,Genvor’s trajectory depends heavily on successful navigation through regulatory approval gates coupled with timely strategic partnerships facilitating commercialization rollout across large row crop markets globally.The planned expansion into peptide applications targeting consumer health presents optionality diversifying long-run opportunity set though remains preliminary.Investors should watch closely upcoming trial results,cash flow development,and alliance activity which will collectively govern progression from pure R&D innovator toward viable agribiotech commercial entity.

This analysis is intended solely for informational purposes based on publicly available data as of March 2026.It does not constitute an investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments