Karat Packaging’s Shift to Import-Led Distribution Supports Margin Expansion Amid Industry Fragmentation

Karat Packaging drives growth through supply chain diversification, eco-friendly products, and expanding distribution, while navigating competitive and regulatory pressures.

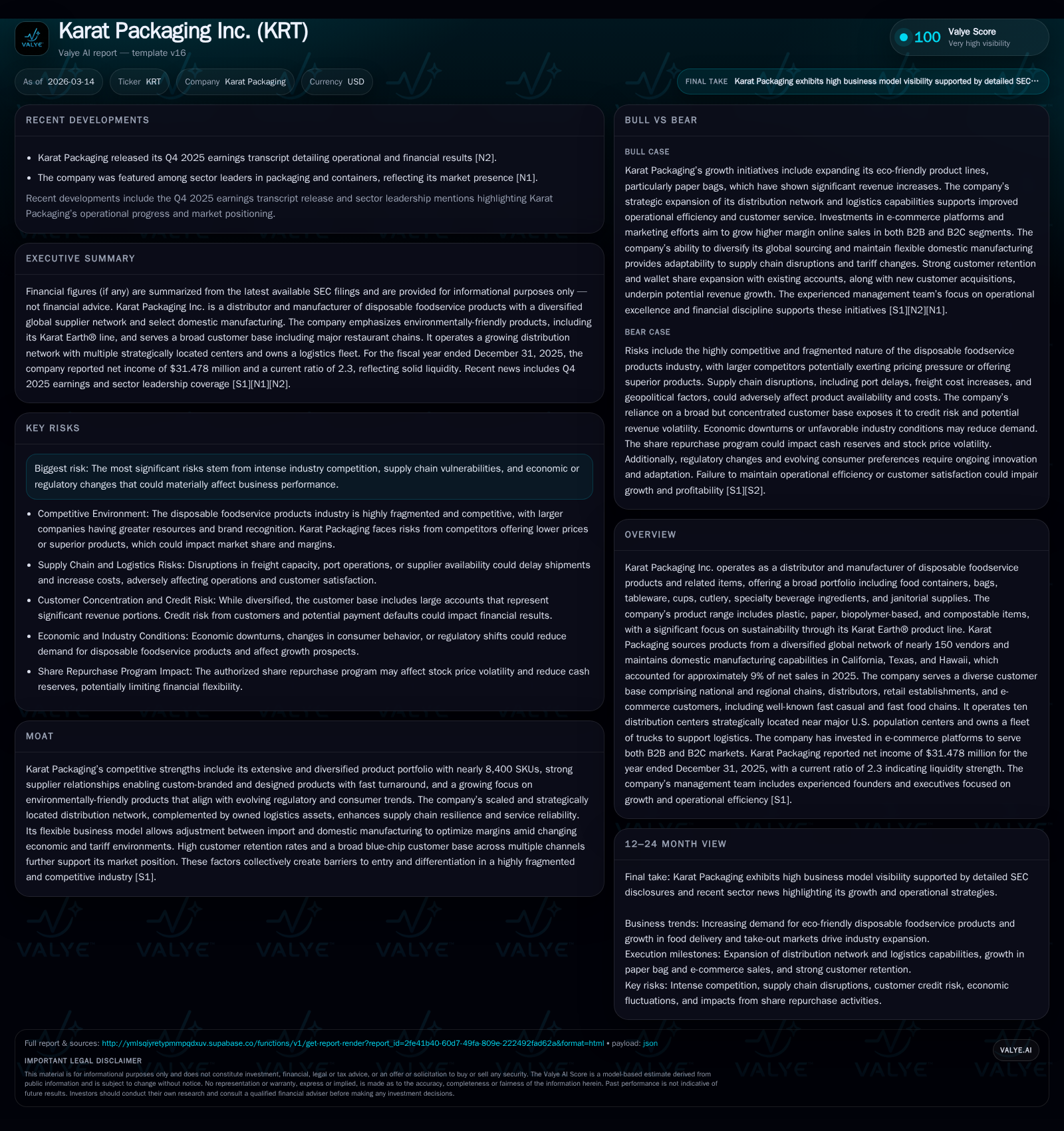

Karat Packaging Inc. (KRT) operates a broad portfolio of disposable foodservice products, blending global sourcing with domestic manufacturing and a multi-channel distribution network. Over recent years, the company has grown steadily by enhancing its supplier diversity, expanding distribution centers, and emphasizing sustainable product lines such as Karat Earth®. In 2025, operating income rose nearly 10% year-over-year, supported by strategic shifts toward import-heavy operations to mitigate costs amid volatile tariffs and labor expenses. Looking ahead, growth hinges on expanding the paper bag business, broadening e-commerce channels, and extending geographic reach. The capital structure remains manageable though leverage covenants impose some operational constraints. Key risks include intense competition, supply chain disruption, raw material inflation, and regulatory changes governing single-use disposables.

Company Overview

Karat Packaging Inc. (ticker: KRT) stands as an integrated distributor and manufacturer specializing in disposable foodservice products ranging from containers to specialty beverage ingredients. The company’s diversified offering spans plastic, biopolymer-based compostable items (under the Karat Earth® brand), paper products including recently expanded paper bags, and janitorial supplies. Its revenue model primarily derives from distributing sourced goods through a vast global supplier base near 150 vendors complemented by manufacturing operations located in California, Texas and Hawaii — contributing roughly 9% to net sales for fiscal year 2025 [S6][S8][F1]. Karat targets multiple customer channels such as national/regional restaurant chains (e.g., Applebee’s, Chili’s), distributors serving diverse foodservice outlets, retail specialty beverage shops, and growing e-commerce clientele.

Historical Performance and Drivers

The company's financial trajectory over recent years reflects steady profitability enhancement alongside controlled capital spending. Operating income rose to approximately $41.4 million in FY2025 from $37.8 million the prior year—marking a solid 9.7% year-over-year increase; net income similarly increased by about 5%, reaching $31.5 million. These gains were realized against a backdrop of rising supply chain complexity offset by strategic shifts toward import-led sourcing that trimmed manufacturing contribution from 11% to around 9% of revenues [F1][S8]. Operating cash flow declined almost 30% year-over-year to $33.8 million—reflective largely of working capital adjustments—but remained robust against minimal capital expenditure of $0.76 million in FY2025 as the firm adopted a more asset-light footprint [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 31 | 34 | 41 | 1 | +5.0% |

| 2024 | 30 | 48 | 38 | 1 | -7.7% |

| 2023 | 32 | 53 | 42 | 3 | +37.3% |

| 2022 | 24 | 29 | 30 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 33 | 21.1 |

| 2024 | 47 | 19.3 |

| 2023 | 51 | 21.1 |

| 2022 | 27 | 16.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue explicit values are unavailable for disclosure; the focus is on profit and cash flow trends.

Business Model Dynamics

Karat operates uniquely across direct imports and selective domestic manufacturing—a balance allowing nimbleness amid global logistic uncertainties and tariff environments [S8]. From its founding co-founders Alan Yu and Marvin Cheng’s vision over two decades ago through current management led by Chief Revenue Officer Daniel Quire and CFO Jian Guo, the company has engineered flexible sourcing strategies coupling vendor diversification with geographically positioned warehouses to optimize inventory velocity.

Its ability to offer customized packaging solutions including custom printing and design emphasizes value-add beyond commodity product distribution [S6][S11]. The scalable logistics network featuring ten warehouses—including recent additions—and owned trucking assets bolsters delivery reliability especially important to fast casual restaurants who rely on quick replenishment for takeout/delivery volumen growth [S7][S9][S10].

Growth Prospects

Looking forward, Karat identifies several structural growth catalysts:

- Eco-Friendly Product Expansion: Sales from Karat Earth® products formed over a third (34%) of total sales in FY25 with investments ongoing toward innovation meeting tightening regulations requiring compostable materials [S18].

- Paper Bag Business: A major strategic focus started in mid-2025 landed material contracts valued around $17 million in annualized revenue with plans to scale further—a segment seen as a key driver over next two-three years [S18][S22].

- E-commerce Scaling: The firm continues growing its omnichannel presence via Amazon, Walmart, TikTok storefronts while increasing direct fulfillment efficiency since scaling back third-party e-fulfillment in late 2024 leading to better margins online [S13]. B2C penetration is an emerging vector complementing traditional B2B customers.

- Distribution Network Enhancement: Adding warehouse space near key metro hubs plus fleet expansion supports both volume growth and service quality improvements likely to drive retention plus new client wins within saturated competitive landscape [S9][S7].

- New Market Penetration: Expanding beyond restaurant chains into sectors like airlines and entertainment venues may widen addressable market.

However, these opportunities coexist with headwinds such as increased competition from larger conglomerates with legacy scale advantages, continuing raw material fluctuations impacting prices of plastic/paper inputs redirecting margin pressures even though Karat tries passing costs downstream rapidly [S1][S14].

Financial Expectations & Milestones

No explicit forward guidance has been disclosed post-FY25 earnings release yet indications from Management's Discussion underscore continued prioritization of supply chain resilience measures—diversifying Asian supplier geographies towards Malaysia/Vietnam which collectively grew their sourcing share nearly twofold between FY24-25—and expanding selective domestic production capabilities balanced with asset-light import reliance to protect margins against tariff variation [N2][S8]. Watch for:

- Quarterly sales proportion shifts between imports vs domestically produced goods,

- Growth rate acceleration in eco-friendly product lines,

- Paper bag contract renewals/expansions reflecting progress on that front,

- Operating margin trends reflecting freight cost volatility impact.

Returns & Capital Allocation

Return metrics portray solid profitability: approximated ROE stood at roughly 21% for FY25 (net income/equity ratio using reported figures), illustrating effective use of equity capital amidst moderate growth investments [F1]. Free cash flow remains positive at approximately $33 million after capex which stays subdued reflecting lean infrastructure additions mainly dedicated to distribution centers rather than heavy manufacturing equipment investment.

Capital deployment has included moderate share repurchases under Board-approved program ($15 million total authorization started November ’25; $12 million remaining end FY25) providing some return to shareholders while balancing liquidity needs for organic expansion or strategic acquisition opportunities as they arise[S2][S23]. Dividends are not mentioned indicating reinvestment focus or buyback preference currently.

Competitive Position & Risks

Karat Packaging occupies a defensible niche built on breadth/depth of SKUs (~8,400 distinct items), flexibility between import/manufacturing channels mitigating supply shocks/tariffs, expansive multi-modal logistics assets enabling high service levels uncommon among smaller distributors; plus responsive customization capability enhancing client stickiness[S6][S7][S24]. Customer concentration remains low —no individual client accounting for more than 10% revenue reducing counterparty risk—and major customer retention at near perfect levels underscores satisfaction[S13][S22].

Nonetheless risks loom:

- Commodity input inflation or disruptions could compress margins if costs cannot be passed through swiftly enough.

- Regulatory landscapes demanding more eco-compliant packaging may force ongoing product reformulation/investment.

- Supply-chain fragility given reliance on international suppliers exposed to geopolitical tensions/labor issues.

- Intense competition from larger incumbents or aggressive pricing tactics impacts market share gain potential[S1][S17][S20].

- Integration risks if pursuing acquisitions given limited merger experience might strain resources or distract management.[S17]

Conclusion

Karat Packaging Inc.’s strategy leverages growing consumer demand for sustainable disposable foodservice products alongside an adaptable supply model combining global sourcing with U.S.-based finishing/manufacturing capabilities supported by a robust distribution network concentrated near population centers nationwide. Management’s efforts driving margin improvement via shifting toward import-led models coupled with investments expanding e-commerce infrastructure underline commitment to both financial discipline and growth orientation.

The business appears financially healthy with consistent profits, strong cash generation despite some operating cash flow variability year-over-year due mainly to working capital effects rather than operational deterioration.

Monitoring upcoming earnings announcements for revenue breakdown evolution between product segments (particularly paper bags/eco-friendly lines) alongside margin trends will provide insight into execution success across critical initiatives against macroeconomic challenges shaping this dynamically evolving sector.

This analysis is informational only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments