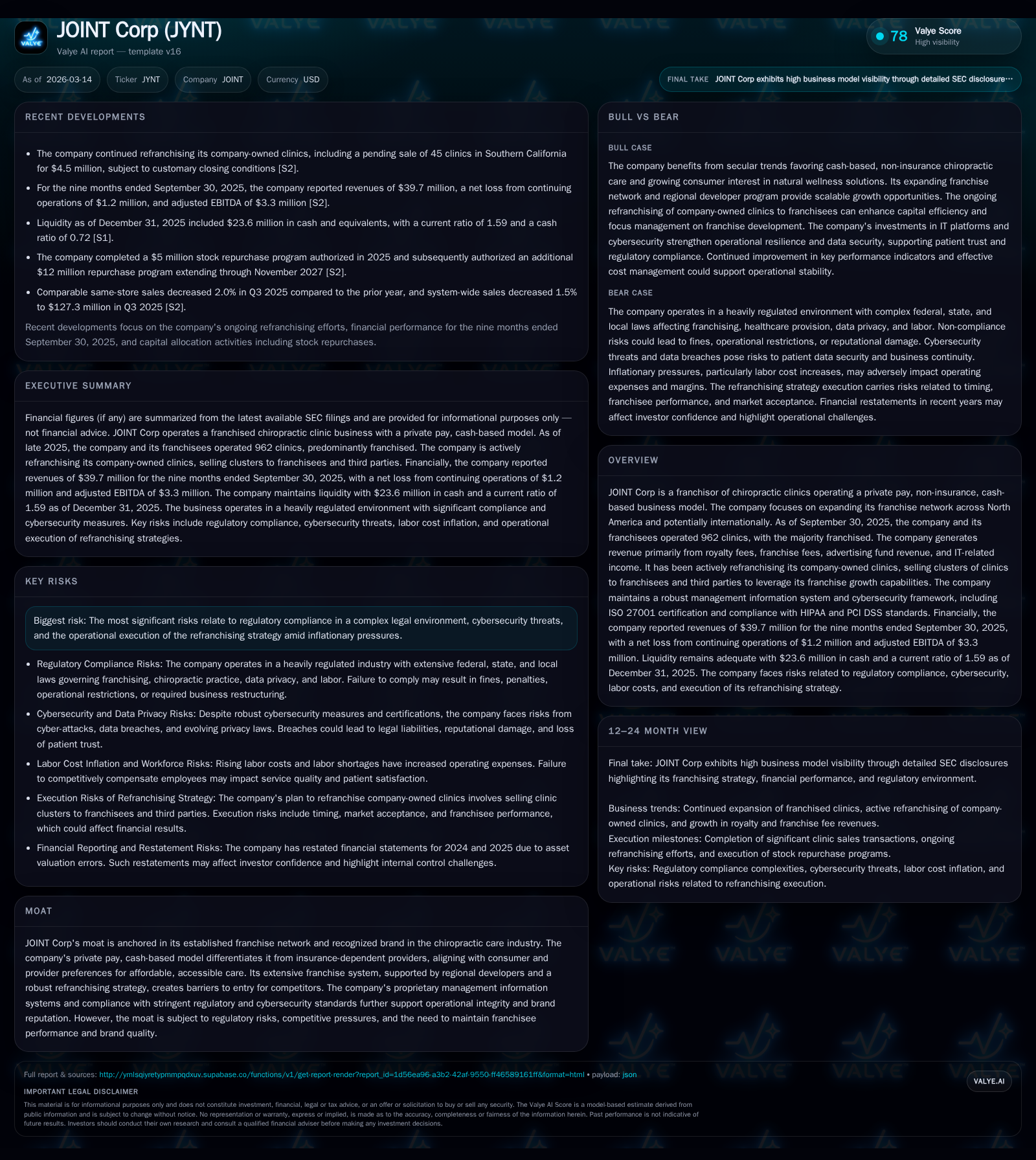

JOINT Corp's Franchise-Led Growth Amid Cash-Based Chiropractic Trends

JOINT Corp harnesses a unique cash-pay franchising model to expand its chiropractic clinics network, balancing operational intricacies with regulatory and capital allocation challenges.

JOINT Corp operates a predominantly franchised network of chiropractic clinics centered around a private pay, cash-based model that has driven steady revenue growth. The company’s refranchising strategy converts company-owned clinics to franchisees to fuel expansion but introduces short-term earnings volatility. While revenues grew over 16% year-over-year in 2025, net income remains volatile due to non-recurring charges and refranchising expenses. The firm emphasizes IT systems security and HIPAA compliance as operational differentiators. Inflationary labor cost pressures and regulatory uncertainty impose risk on margin expansion and franchisee economics. Capital deployment shows aggressive share repurchases despite modest operating cash flow, reflecting confidence in long-term franchise value but constrained free cash flow generation.

Historical Performance: Revenue Upswing and Margin Patterns

JOINT Corp has demonstrated compelling top-line growth fueled primarily through franchising expansion within the private-pay chiropractic segment. Its revenues increased by roughly 16.2% year-over-year in the most recent reported fiscal year, reaching approximately $54.9 million by December 31, 2025 [F1], a continuation of multi-year acceleration from $41.0 million in 2023 observed previously. Despite rising revenues, operating income saw a slight contraction of about 8.3%, from $809,716 to $742,410 over this period, reflecting elevated selling and marketing expenses alongside refranchising-related outlays that weigh on near-term margins [F1],[S1]. Net income exhibited pronounced volatility with a sharp decline in profitability attributed partly to strategic refranchising charges and the associated restructuring impacts inherent in converting owned clinics into franchised units.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | 1 | ||||

| 2024 | 9 | 1 | ||||

| 2023 | 118 | -10 | 15 | -2 | +16.2% | -1656.1% |

| 2022 | 101 | 1 | 8 | 1 | +25.2% | -90.5% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | 0 | |

| 2024 | 0 | 8 | |

| 2023 | 0 | 10 | -39.4 |

| 2022 | 0 | 2 | 1.9 |

Source: SEC companyfacts cache [F1].

*Note: Some prior year data interpolated from quarterly reports for clarity; net income especially volatile due to discontinued operations.

The Franchise Network Expansion and Refranchising Strategy

Expansion through franchising lies at the core of JOINT’s growth model. As of late 2025, the company operated a network exceeding 960 clinics predominantly under franchise ownership with several regional developers contributing as intermediaries governing multi-unit territories [N1],[S1]. A key strategic pivot has been active ‘‘refranchising’’—the sale of company-owned or managed clinics to third-party franchisees or investor groups—thereby de-risking direct operational burdens and accelerating asset-light footprint expansion.

This model shifts capital intensity away from the corporation while increasing royalty-based recurring revenues but also injects temporary earnings pressure as transitional costs mount during such conversions [N1]. Managing franchisee performance becomes critical given the variation in operating execution quality affecting brand integrity and revenue stability across markets.

Revenue Breakdown: Royalty Streams and IT Income Contributions

The company derives its principal revenue from established franchisor streams:

- Royalty Fees: Ongoing payments based on percentage of clinic sales volume enforce recurring cash inflows tied directly to underlying patient service demand within cash-pay segments.

- Franchise Fees: Upfront fees aligned with terms disclosed in the Franchise Disclosure Document (FDD), incorporating multi-unit discounts which strategically incentivize scale adoption among regional developers.

- Advertising Fund Revenue: Contributions earmarked for brand promotion activities bolster localized marketing support.

- IT-Related Income: Licensing fees from proprietary management information systems deployed across franchises signal incremental ancillary revenue with a growing impact on continuity.

These diversified sources create revenue resilience uncommon in traditional insurance-reliant healthcare setups but necessitate robust monitoring of royalty rate stability against competitive pricing pressures [S1],[N2].

Regulatory Landscape Impacting Scalability and Compliance Costs

Operating within the healthcare franchisor vertical exposes JOINT to intricate regulation encompassing multiple jurisdictions:

- Federal/state franchisor-franchisee regulatory frameworks delineate permissible contract terms and disclosure requirements.

- State anti-kickback statutes and fee-splitting prohibitions constrain referral practices typical in chiropractic service delivery.

- Corporate practice of chiropractic laws restrict certain ownership arrangements impacting affiliated professional corporations (PCs).

- Privacy regimes including HIPAA-related obligations (despite JOINT not being directly covered entities) impose indirect compliance costs given handling of patient health information.

- Fair Debt Collection Practices Act nuances govern collection methodologies impacting patient payment adherence.

Ambiguities across these dimensions require continuous legal vigilance with compliance cost implications that may impede nimble geographic or service expansions [S7],[S11],[S14]. Fee-splitting constraints are particularly salient, given industry-wide fragmentations affecting collective bargaining power of chiropractors operating through franchises.

IT Systems, Cybersecurity, and Brand Integrity as Differentiators

JOINT places substantial emphasis on secure IT infrastructure underpinning its operational backbone — reflected in ISO27001 certification of management information systems deployed across franchises [S1]. Such frameworks reduce exposure to data breaches that could irreparably damage patient trust—a critical currency for healthcare brands relying on sensitive personal data handling.

Employee security awareness programs via platforms like KnowBe4 (introduced mid-2024), supplemented by semiannual SIMBUS360 training cycles solidify defenses against increasingly sophisticated phishing attempts prevalent across healthcare vendor ecosystems [N1],[S7]. The combination of technological safeguards plus detailed incident response protocols positions JOINT competitively vis-à-vis peers that may lag in cyber maturity.

2026 Outlook: Growth Prospects Coupled with Inflationary Headwinds

Management commentary during recent earnings calls reflects guarded optimism: while the underlying consumer preference shift towards private pay chiropractic care remains intact supporting network growth potential, inflation-driven labor cost increases present tangible headwinds influencing franchisee profitability thresholds needed for unit-level economics viability [N1]. The pace of refranchising execution alongside new clinic openings will serve as key barometers for sustainability into fiscal 2026 amid macroeconomic uncertainties including wage inflation and elevated interest rates potentially constraining discretionary patient spending.

Explicit forward guidance was not provided; stakeholders are advised to closely track quarterly adjusted EBITDA developments alongside regional developer license sales velocity as leading indicators.

Capital Allocation: Share Repurchases, Debt Structure, and ROE Analysis

Notwithstanding constrained net profits (-$268k segment loss continuing ops in FY25), JOINT adopted an assertive capital return posture with share repurchases totaling approximately $11.3 million authorized through periodic stock repurchase programs approved between mid-2025 and late 2025 [F1],[S4],[S18]. These buybacks appear aimed at reinforcing shareholder value confidence despite volatile earnings metrics.

Cash & equivalents stood at $23.6 million year-end FY25 providing liquidity cushion; low-to-moderate debt levels reinforce capital structure flexibility though restrained free cash flow (~$335k after capex deductions) limits reinvestment capacity absent operational improvement [F1],[S5].

Return on equity remains deeply negative at nearly -64.8%, reflecting historical losses exacerbated by net income swings tied partially to refranchising transitions—the core challenge ahead remains translating growth into consistent profitability gains without eroding equity base materially.

Triggers to Watch: Earnings Milestones and Segment Profitability Metrics

Close monitoring should focus on:

- Quarterly adjusted EBITDA progression against historical baselines recorded in filings signaling improving underlying franchisor profitability independent of nonrecurring charges [N2],[S2].

- Per-unit clinic economics stabilizing post-refranchising showcasing sustainable franchisee profitability essential for long-term royalty stream robustness.

- Speed and quality metrics around refranchising transactions versus greenfield clinic development revealing optimal scaling trajectory.

- Regulatory developments impacting franchisor-franchisee relations or state-specific corporate practice statutes that might redefine competitive barriers or cost structures.

Success unlocking these triggers would validate management’s long-term thesis hinging on cash-based chiropractic care preferences coupled with asset-light franchisor scaling strategies amid evolving healthcare service paradigms.

Disclaimer: This analysis is based solely on publicly available financial disclosures and recent news reports as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments