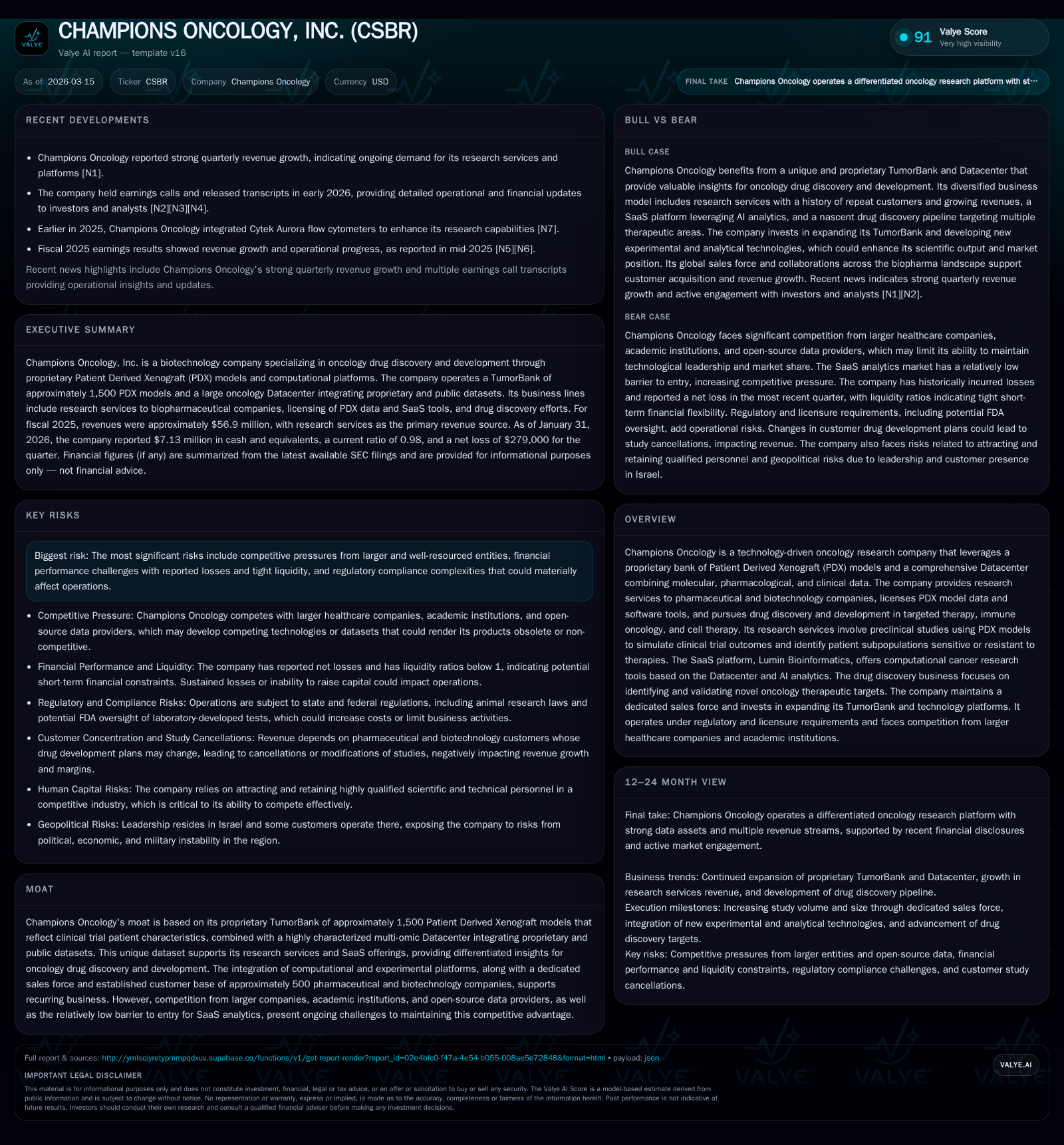

Champions Oncology Advances Proprietary PDX TumorBank and AI Platforms Amid Profitability Recovery

Champions Oncology leverages its unique Patient Derived Xenograft model bank and integrated Datacenter to serve biopharma with oncology research services and SaaS tools, while gradually advancing drug discovery pipelines.

Champions Oncology, Inc. has returned to profitability in fiscal 2025, primarily driven by growth in its research services utilizing a proprietary TumorBank of approximately 1,500 PDX models. The company's integrated Datacenter and artificial intelligence-powered SaaS platform support both experimental and computational oncology research for pharmaceutical and biotech clients worldwide. Despite competitive pressures from well-resourced incumbents and open-source alternatives, Champions continues to invest in expanding its TumorBank, enhancing analytical platforms, and advancing novel drug discovery efforts in targeted therapy, immune oncology, and cell therapy. Operating cash flows have improved substantially, supporting a positive free cash flow profile as product offerings scale, though liquidity remains a key watch area going forward.

Business Model and Core Assets

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 5 | 7 | 5 | 0 | +164.6% |

| 2024 | -7 | -6 | -7 | 1 | -36.4% |

| 2023 | -5 | 4 | -5 | 3 | -1073.5% |

| 2022 | 1 | 6 | 1 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 7 | 124.6 |

| 2024 | 634000 | -7 | 382.3 |

| 2023 | 74000 | 1 | -115.1 |

| 2022 | 4 | 6.0 |

Source: SEC companyfacts cache [F1].

Champions Oncology operates at the nexus of experimental oncology research services, computational biology SaaS products, and emerging drug discovery initiatives. At its core lies an extensive Patient Derived Xenograft (PDX) TumorBank comprising roughly 1,500 tumor models derived from late-stage, pretreated metastatic cancer patients [S1][S7]. This living TumorBank is unique due to its depth of molecular (genomics, transcriptomics), phenotypic, and pharmacological characterization coupled with ongoing re-characterization efforts [S20][S25]. The TumorBank underpins all facets of Champions’ businesses.

The company licenses access to this rich dataset through its Lumin Bioinformatics SaaS platform that incorporates approximately 3,500 proprietary molecular datasets alongside roughly 20,000 publicly available datasets [S7]. Lumin provides computational tools utilizing AI analytics for hypothesis generation around biomarkers, therapeutic resistance mechanisms, and patient stratification strategies.

Research services account for the majority of current revenue streams by conducting in vivo and ex vivo preclinical studies using PDX models implanted into mice to simulate clinical trial outcomes [S7][N1]. Typical study sizes range from $125k to potentially over $500k in regulatory compliant environments. Over the past decade Champions has served ~500 biopharma clients globally with growing repeat business [S25].

Drug discovery is a nascent but strategic avenue leveraging Champions’ combined experimental platforms and computational insights targeting oncology therapeutic modalities: targeted therapies such as antibody-drug conjugates (ADCs), immunotherapies, and cell therapies [S7]. The company maintains segregated scientific teams dedicated to discovery programs with multiple targets progressing along validation stages.

Historical Financial Performance

Champions Oncology has experienced a volatile financial trajectory culminating in a profitable fiscal year ending April 2025 [F1]. A summary of key annual financials follows:

| FY | Rev | OpInc | Net | CFO | Capex | Buybacks | OpInc YoY % | Net YoY % | CFO YoY % |

|---|---|---|---|---|---|---|---|---|---|

| 2025 | - | 4553000 | 4701000 | 7386000 | 389000 | 0 | +161.9% | +164.6% | +220.4% |

| 2024 | - | -7356000 | -7276000 | -6137000 | 836000 | 634000 | |||

| 2023 | - | -5256000 | -5335000 | 3972000 | 2872000 | 74000 | |||

| 2022 | - | 607000 | 548000 | 6497000 | 2384000 |

Note: Revenue figures were not explicitly provided; narrative focuses on profitability trends based on available data.

The fiscal year ended April 2025 marks a clear inflection: operating income swung from a loss exceeding $7 million in FY2024 to a positive $4.55 million [F1]. Net income similarly rebounded from losses near $7.3 million to $4.7 million positive. Operating cash flow also surged dramatically by over 220%, reaching approximately $7.39 million [F1]. Capital expenditures decreased materially as major investments in infrastructure and capabilities plateaued.

This financial improvement aligns with reported revenue growth driven by expanded adoption of research services leveraging the proprietary platforms [N1][S7]. Despite lacking exact topline disclosures post-2019 ($2.9M then), operational enhancements suggest scale benefits are manifesting.

Drivers of Past Growth

Key factors underpinning Champions Oncology's historical performance include:

- TumorBank Expansion: Continuous addition of tumor models derived both through hospital partnerships facilitated by a medical affairs team and legacy Personalized Oncology Services clients has broadened model variety including resistant phenotypes [S6][S25].

- Datacenter Development: Integration of proprietary multi-omic data with thousands of public datasets created a differentiated foundation for computational analysis [S7][S11].

- Research Service Salesforce: A dedicated sales force (~35 personnel) targeting biopharmaceuticals globally supports high customer retention and expanding spend per client through education of platform value [S7].

- Technology Augmentation: Investments in sophisticated pharmacology platforms alongside analytical software enhance depth/speed of experimental insights [S6][S16][S20].

- Computational Innovation: Advancements in AI-driven analytics within Lumin developed by bioinformaticians position Champions competitively despite open-source alternatives [S5][S11].

Future Growth Prospects

Champions’ growth outlook pivots on several interrelated factors:

- TumorBank Enrichment: Further growing model numbers especially rare or resistant tumor subtypes can enhance dataset comprehensiveness driving value for customers seeking biologically relevant models [N2][S25].

- Software Adoption: Increasing recurring revenue from SaaS subscriptions depends on demonstrating unique analytics value vs free public resources along with continual updates to analytical workflows leveraging AI advances [N2][S5][S11].

- Drug Discovery Pipeline Progress: Validation milestones for novel targets within ADCs, immune-oncology agents, or cell therapies could unlock licensing or partnership opportunities fueling upstream revenue streams [N2][S7].

- Market Expansion: Wider penetration among pharmaceutical/biotech customers globally via enhanced sales efforts or collaborations.

- Operational Leverage: Scaling experimental throughput without proportional cost increases could expand margins.

Constraints include intense competition from large CROs with greater resources using alternative technologies; risks that emerging computational methods erode the uniqueness of Champions’ SaaS platform; volatility in pharma R&D spending impacting study bookings; regulatory compliance burdens; and geopolitical risks related to leadership based in Israel [S4][S8][N2].

Forecasts and Key Milestones to Monitor

The company has not publicly issued specific guidance but recent commentary highlights:

- Continued quarterly revenue growth momentum evidenced by latest quarterly reports [N1]

- Ongoing expansion of both TumorBank size and molecular characterization depth [N2]

- Progression of select drug discovery candidates through target validation phases aiming toward preclinical development [N2]

- Growth trajectory for Lumin SaaS user base underpinning subscription revenues [N2]

From an analyst perspective one should track upcoming quarterly metrics including bookings for new studies versus cancellations due to customer pipeline shifts (not uncommon per risk disclosures). Approval or licensing deals emanating from early-stage pipeline candidates will be material value inflection events.

Returns and Capital Allocation Dynamics

The company’s approximate return on equity calculated from FY2025 net income ($4.7M) against equity ($3.77M) reflects around a very high nominal ROE near ~125%, partly due to historically depressed equity values during loss periods that have now reversed somewhat given recent profit generation [F1]. This metric should be monitored over multiple periods for stability.

Operating cash flow improved considerably to approximately $7.39 million while capex was modest at about $389k enabling free cash flow close to $7 million annually – highlighting improving operational efficiency balancing reinvestment needs versus liquidity preservation [F1].

No share repurchases occurred during fiscal year 2025 after small buybacks in earlier years; additionally the company has never paid dividends preferring to reinvest earnings towards platform growth initiatives consistent with early stage innovation companies [F1][S26]. Liquidity remains adequate but tight given current liabilities slightly exceed current assets (current ratio ~0.98) as of January 2026 quarter end – requiring ongoing monitoring especially if broader market conditions tighten capital access [F1][N1].

Competitive Landscape Analysis (Domain Insight)

Oncology research services operate within intense competitive environments dominated by large contract research organizations (CROs) offering broad services including early-stage preclinical work often integrated with clinical trial operations. Champions' distinct advantage derives from their proprietary TumorBank linked deeply characterized biological data sets presented within an AI-supported ecosystem—an increasingly rare combination providing more predictive translational insights than traditional cell line or generic xenograft models.

Nonetheless large CROs benefit from scale advantages allowing multi-modality service bundles which can appeal broadly despite less specialized modeling fidelity. Separately academia/public consortia improve data accessibility via open sources potentially undermining exclusive value propositions tied solely to data ownership unless continuously enhanced by proprietary algorithms as Champions attempts via Lumin.

Equally critical is securing leading-edge talent capable of advancing both wet lab discoveries and sophisticated bioinformatics underpinned by modern machine learning frameworks—a known strategic constraint reflected industry-wide tightening life science hiring markets [S14][S15].

Risks Summary Highlighted by SEC Filings

Key risk considerations include:

- Dependency on continued capital availability if profitability falters given historical losses and operating cash fluctuations [S1][F1]

- Regulatory scrutiny over laboratory practices including animal testing regulations potentially increasing compliance costs or limiting operations [S8][S14]

- Customer project cancellations linked to pharma R&D budget shifts causing revenue variability [S4]

- Intellectual property vulnerabilities as key TumorGraft techniques remain trade secrets rather than patented technology exposing know-how leakage risks [S21]

- Cybersecurity threats threatening data integrity critical for SaaS credibility amid rising geopolitical cyber risks including CEO residing abroad impacting business continuity concerns [S19][S22]

- Competitive pressure from better-capitalized entities or technological obsolescence risking erosion of market share or pricing power [S5][S12]

- Leadership concentration risks with management controlling majority voting shares affecting corporate governance dynamics influencing stockholder interests indirectly [S26]

Conclusion

Champions Oncology stands at an inflection point having demonstrated robust operational recovery underpinned by differentiated scientific assets highlighted by its expansive PDX TumorBank coupled with cutting-edge AI analytics embedded within its SaaS platform Lumin. The company’s heterogeneous business model spanning research services revenue plus nascent but promising drug discovery pipelines creates optionality for future value capture if execution hurdles are navigated successfully.

While liquidity appears sufficient through mid-2026 bolstered by positive operating cash flows generating free cash flow surplus after modest capex reinvestment, ongoing vigilance toward managing regulatory compliance overheads and competitive responses is essential. The absence of dividend distribution or buybacks aligns with reinvestment priorities typical among emerging biotechnology technology providers navigating complex commercialization pathways.

Investors monitoring Champions Oncology should focus closely on quarterly study bookings trends amidst pharma industry cyclicality, SaaS subscriber base expansion pacing relative to open-source alternatives, strategic license deals linked to validated drug targets nearing clinical stages, cost control discipline sustaining margin expansion curves beyond recent turnarounds, as well as any updates regarding geopolitical risk exposures related to executive leadership domiciles.

This report summarizes publicly available information as of March 15, 2026 regarding Champions Oncology Inc., relying exclusively on cited filings ([F1], [N#], [S#]). It does not offer investment advice or forecasting beyond factual analysis drawn from provided data sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments