CO2 Energy Transition Corp.’s Financial Position Hinges on Successful Business Combination Execution

As a blank check company targeting the energy transition sector, CO2 Energy Transition Corp. remains reliant on completing a strategic merger within regulatory timelines.

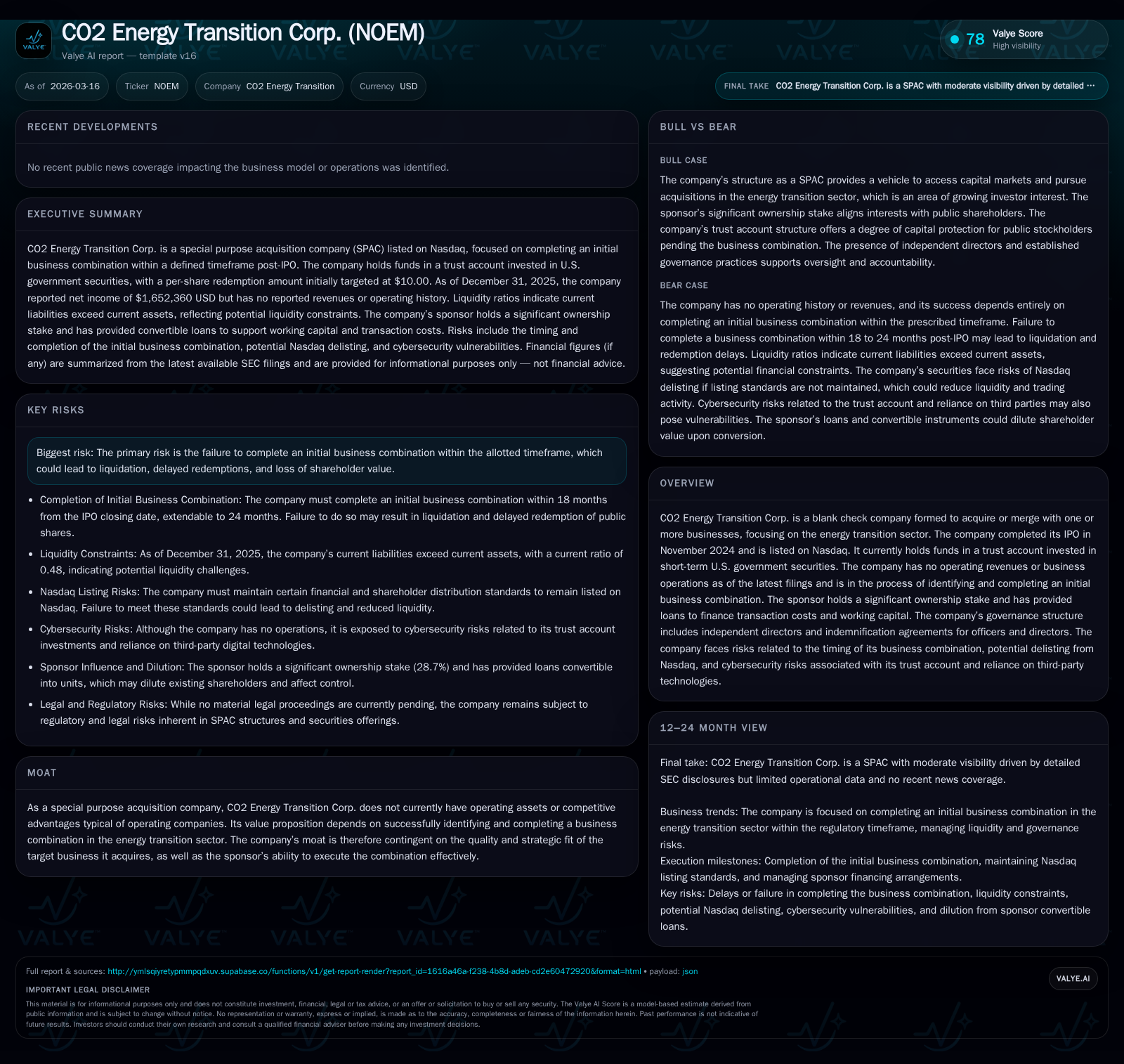

CO2 Energy Transition Corp. (NOEM) is a special purpose acquisition company (SPAC) focused on the energy transition industry. Since its November 2024 IPO, it has generated no operating revenues and operates primarily through funds held in a trust account alongside sponsor-provided working capital loans. The company's future depends entirely on identifying and consummating an initial business combination by May 2026 or within an extended window through November 2026. Failure to do so risks liquidation and shareholder value erosion. Financial results through 2025 reflect operating losses and negative cash flow, underscoring the SPAC’s status as a holding entity rather than an operating company.

Company Overview and Business Model

CO2 Energy Transition Corp., trading under ticker NOEM, is a special purpose acquisition company formed with the mandate to identify and acquire one or more businesses within the energy transition sector. The company’s IPO closed on November 22, 2024, raising proceeds that currently reside in a trust account invested primarily in short-term U.S. Treasury securities with maturities under 185 days. As of early 2026, NOEM holds no operating assets, generates no revenues, and has yet to complete its initial business combination [S1].

The SPAC model depends on consummating a merger or acquisition that results in a viable public operating company. NOEM's value creation hinges on securing such a target positioned within the energy transition sector—a market characterized by accelerating global policy momentum toward decarbonization.

Historical Financial Performance

As expected for a blank check company, NOEM's financials show no operational activity but reflect costs incurred during its formation phase. Operating losses increased from approximately $246k in fiscal year 2024 to about $646k in fiscal year 2025—primarily due to administrative overhead related to legal, accounting, and organizational efforts including due diligence for potential acquisitions [F1].

Net income swung positively from near break-even ($2.6k) in 2024 to $1.65 million in 2025, likely driven by non-operating items such as remeasurement gains rather than profits from operations [F1]. Operating cash flow remained negative at around $745k in 2025, more than doubling compared to the prior year as expenses mounted without offsetting revenues.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 1652360 | -745359 | -646306 | +62679.6% |

| 2024 | 2632 | -305589 | -246139 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -92.4 |

| 2024 | -0.2 |

Source: SEC companyfacts cache [F1].

This snapshot typifies a SPAC in its pre-combination phase—costs are front-loaded into finding targets without operational revenues.

Capital Structure and Sponsor Involvement

The sponsor holds roughly 28.7% ownership post-IPO through founder shares and private placement units purchased at IPO pricing totaling $2.65 million [S3][S16]. These units include shares plus warrants exercisable at $11.50 per share following specified post-merger timing constraints.

Sponsor financing includes unsecured promissory notes initially capped at $800k (mostly repaid upon IPO closing except minor outstanding amounts) and a Working Capital Note allowing up to $1.5 million for transaction costs or working capital needs [S3][S6][S12]. As of December 31, 2025, only $11.7k was outstanding under this facility.

The Working Capital Note can convert into units identical to private placement units at $10 per unit. NOEM carries no interest-bearing debt apart from these related-party facilities structured as interim funding until completion of the initial business combination.

Risks and Governance Considerations

Key risks include failure to close an initial business combination within prescribed deadlines—May 22, 2026 (18 months post-IPO) or November 22, 2026 if extended by six months—which triggers mandatory liquidation where public shareholders receive pro rata redemption proceeds from trust account holdings but may face delays due to legal compliance requirements under Delaware law [S1][S4].

Conflicts of interest arise as management balances commitments across entities; sponsors may prioritize affiliated deals; officers may negotiate post-merger compensation linked directly to deal outcomes potentially biasing decisions [S1][S20]. Additional risks involve potential Nasdaq delisting if listing standards are not maintained until transaction closure; cybersecurity threats related to safeguarding trust account funds; and dilution from prospective PIPE financings post-merger which could disadvantage existing shareholders financially [S4][S9][S22].

NOEM maintains independent directors per Nasdaq rules overseeing governance including reimbursement approvals for sponsors’ or officers’ expenses related to deal activities; indemnification agreements protect insiders but entail financial considerations borne by the combined entity after closing [S9][S20].

Future Growth Prospects

NOEM's prospects depend entirely on sourcing attractive targets within the evolving energy transition ecosystem—spanning renewable power technologies, clean fuels development, carbon capture innovations, or energy efficiency solutions. Successful execution could catalyze value creation amid secular tailwinds favoring sustainable energy infrastructure investment.

Failure or suboptimal deal selection risks shareholder dilution from necessary follow-on financings (PIPEs), prolonged holding periods awaiting redemption distributions if liquidation occurs, and continued overhead burdens stemming from ongoing SPAC maintenance expenses.

No explicit milestone guidance or identified prospective targets have been publicly disclosed as of March 2026; proxy materials related to any announced transactions will provide insights into valuation assumptions when available.

Returns and Capital Allocation Strategy

NOEM does not pay dividends nor conduct share repurchases at this stage; reported operating losses solely relate to overhead expenses rather than productive cash flow generation [F1][S9].

For fiscal year ended December 31, 2025:

- Approximate ROE is around -92%, reflecting net income relative to negative equity balances primarily due to formation costs accrued before recognizing deferred equity contributions from founder shares and warrants [F1].

- Operating cash flow remains negative indicating cash resource use absent completion of business combinations or additional capital raises beyond IPO proceeds.

Capital allocation prioritizes meeting administrative cost requirements while preserving resources for eventual transaction closing expenses through careful cash management.

Summary Analysis

CO2 Energy Transition Corp exemplifies a typical SPAC designed specifically to capitalize on investor enthusiasm around climate transition technologies without standalone operations. Its financial profile matches expectations: operating losses driven by administrative costs; lack of revenue generation; reliance on sponsor loans; concentrated voting control among founders; significant risks tied to deal execution timelines.

Investors should recognize that returns depend exclusively on identifying suitable target companies aligned with energy transition strategies—and completing acquisitions within strict regulatory windows set by SEC rules governing SPACs. Potential dilution effects from follow-on financings post-merger warrant consideration.

Current evidence as of early 2026 indicates:

- Capital structure strongly influenced by sponsor stakes with convertible debt facilities supporting near-term deal funding.

- Governance frameworks aimed at mitigating conflicts despite inherent limitations common among SPAC sponsors.

- Redemption rights provide some protection if transactions fail timely but introduce delay risk dependent on judicial dissolution proceedings.

- Market conditions affecting yields on Treasury investments backing the trust account could marginally erode shareholders’ eventual redemptions if adverse rate environments persist.

Ultimately CO2 Energy Transition Corp operates as a financial vehicle until announcing an approved business combination targeting specific entities within the energy transition arena.

Disclaimer: This report presents factual information derived from publicly filed SEC documents as of March 16, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments