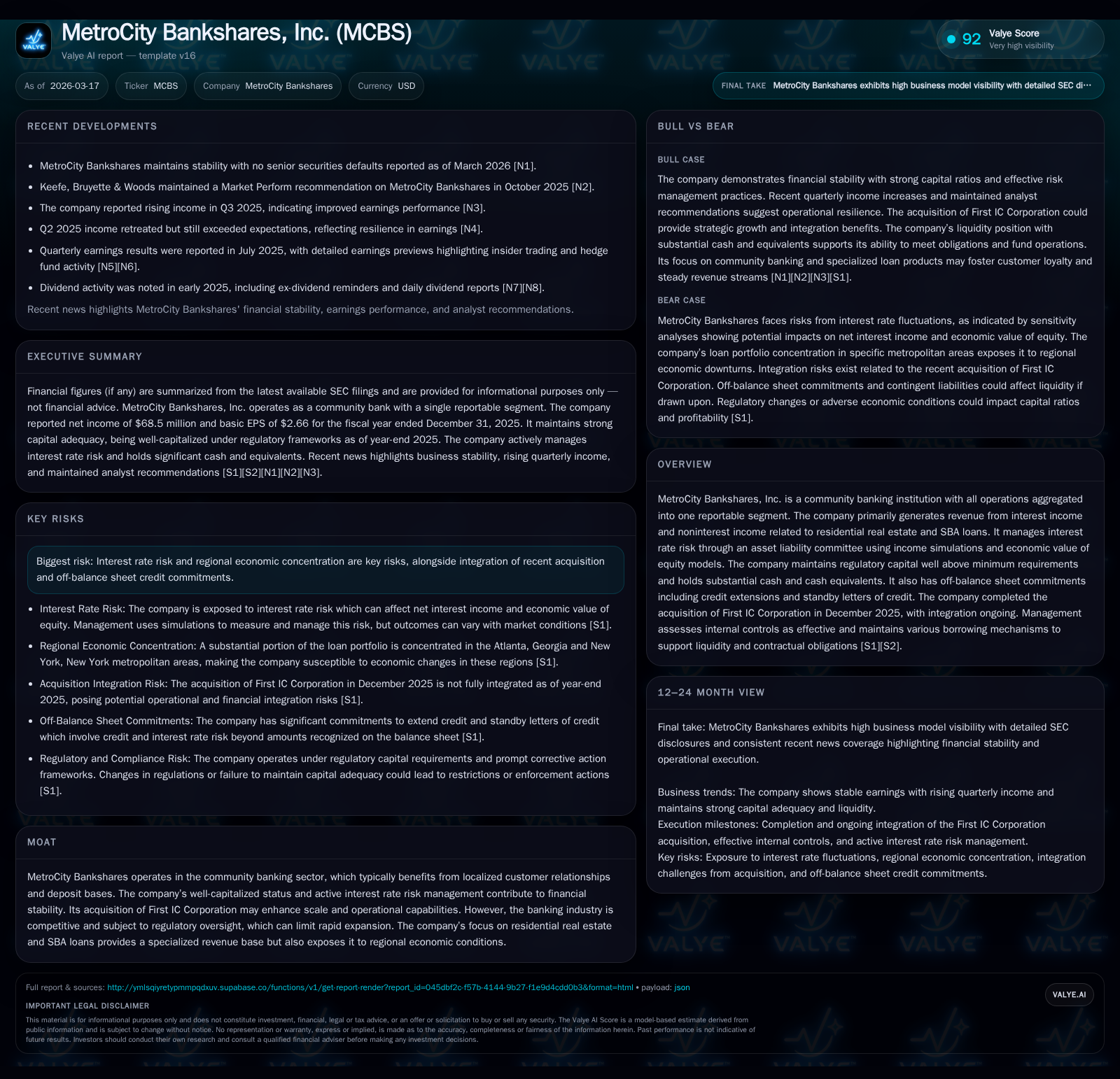

MetroCity Bankshares Solidifies Capital Strength After First IC Acquisition

MetroCity Bankshares combines robust capital adequacy with strategic acquisition integration to enhance its community banking position.

MetroCity Bankshares, a community-focused bank, reported steady net income growth in 2025 after acquiring First IC Corporation in December 2025, while managing interest rate and regional concentration risks through disciplined asset-liability management and regulatory capital buffers. Operating cash flow declined notably, reflecting integration and balance sheet shifts, but equity expansion supports an ROE near 12.6%. The company maintains ample liquidity, off-balance sheet commitments have increased, and cybersecurity governance remains a priority amid this growth phase.

Historical Financial Performance: Income and Cash Flow Trends

MetroCity Bankshares reported net income of $68.5 million for fiscal year 2025, marking a 6.2% increase over the prior year’s $64.5 million [F1]. This growth in profitability contrasts with a notable decline in operating cash flow (CFO), which dropped sharply by approximately 40.6% from $63.5 million in FY2024 to $37.7 million in FY2025. The reduction in cash flow reflects working capital adjustments likely associated with the recent acquisition alongside shifts in asset composition and derivative activity.

Capital expenditures also contracted significantly by nearly half (-47.6%), down to $674,000 in FY2025 from $1.29 million the previous year, indicating a more conservative spending posture concurrent with integration efforts [F1]. Meanwhile, shareholders’ equity expanded robustly from $421 million to $544 million, underpinning a strengthened capital base that supports an approximate return on equity (ROE) of 12.6% — a respectable figure within community banking benchmarks.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 69 | 38 | 1 | +6.2% |

| 2024 | 65 | 64 | 1 | +25.0% |

| 2023 | 52 | 82 | 5 | -17.6% |

| 2022 | 63 | 135 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 25 | 3 | 37 |

| 2024 | 21 | 0 | 62 |

| 2023 | 18 | 2 | 77 |

| 2022 | 15 | 8 | 132 |

Source: SEC companyfacts cache [F1].

Table: MetroCity Bankshares annual financials illustrate steady net income growth matched with declining operating cash flow amid equity expansion supporting ROE.

Acquisition of First IC Corporation: Impact and Integration Progress

The strategic acquisition of First IC Corporation finalized in December 2025 marks a pivotal development for MetroCity Bankshares’ scale and operational scope. Management reports ongoing integration efforts focused on merging operational platforms and aligning credit evaluation processes across the combined entity [S1][S2]. Although the acquisition’s immediate contribution to revenue streams is yet to be fully quantified publicly, it inherently introduces complexity due to business combination accounting practices including recognition of purchased credit deteriorated (PCD) loans and purchased seasoned loans (PSL).

Credit risk evaluation during this phase is critical because these loan categories typically require dedicated allowance calculations for losses recognized at acquisition date rather than through regular loan loss provisioning cycles [S2]. The company acknowledges this as an area under active scrutiny.

Off-balance sheet credit commitments have risen materially—commitments to extend credit jumped from approximately $47 million at end-2024 to over $120 million at year-end 2025, while standby letters of credit more than doubled to nearly $14.5 million—reflecting expanded capacity and client servicing breadth linked partly to the acquisition [S6][S9]. This escalation elevates contingent liquidity considerations during integration.

Interest Income and Loan Portfolio: Core Revenue Drivers

MetroCity Bankshares emphasizes residential real estate and Small Business Administration (SBA) loans as principal drivers of its interest income streams within its single operating segment framework [S1]. The loan portfolio grew substantially alongside acquisition-related scale effects—from approximately $3.17 billion in total loans at end-2024 to over $4 billion by end-2025—with significant portions concentrated in residential mortgages ($2.38 billion) and commercial real estate ($1.56 billion) as of year-end 2025 [S15].

SBA lending exposure includes both direct loans held for investment as well as servicing assets embodying anticipated servicing fees tied to these government-guaranteed sectors—a niche that tends to offer stable yield profiles but entails sensitivity to regional economic cycles.

Underwriting standards remain rigorous with ongoing portfolio monitoring designed to limit nonperforming exposures; reported substandard loans remain minimal relative to total balances [S15].

Managing Interest Rate Risk Through Asset Liability Strategies

Proactive interest rate risk mitigation is embedded into MetroCity’s risk governance via its Asset Liability Committee (ALCO), which utilizes comprehensive income simulation models coupled with Economic Value of Equity (EVE) analysis to anticipate impacts under various rate environments [S1]. This dual approach captures both earnings volatility effects on short-term margin as well as longer-term capital erosion sensitivities.

To complement these quantitative mechanisms, the bank has engaged multiple interest rate derivatives including forward-starting caps and swaps—the notional value exceeding several hundred million dollars—to hedge deposit costs indexed to Federal Funds rates [S10][S20]. These hedges are classified as effective cash flow hedges with no ineffectiveness recognized since inception.

Collateralization practices linked to derivative counterparties include restricted cash deposits held for unrealized gains on swaps providing an additional layer of credit protection embedded within balance sheet liquidity reserves [S7].

Capital Adequacy and Regulatory Compliance Profiles

MetroCity maintains capital well above regulatory minimums, as evidenced by Tier 1 Capital ratios consistently near or above the high-teens percentage range relative to risk-weighted assets—for example, consolidated Tier I Capital was approximately $474 million representing a ratio around 15.9% at December 31, 2025 [S1]. Similarly strong CET1 ratios affirm Basel III compliance comfortably exceeding minimum requirements including capital conservation buffers.

The FDIC officially classifies the bank as "well-capitalized" under prompt corrective action regulations, implying unrestricted access to brokered deposits or capital distributions subject only to normal supervisory review [S1][S19]. This status provides operational flexibility during ongoing expansion phases including post-acquisition scaling.

Management highlights readiness for potential extended recessions but acknowledges future periods could see pressure on reported capital ratios depending on macroeconomic developments or regional downturns affecting collateral values [S19].

Liquidity Position and Off-Balance Sheet Commitments

As of late-2025, MetroCity's liquidity reserves include $383.7 million in cash and cash equivalents—a sizable buffer relative to total assets that aids day-to-day operational requirements as well as stress scenarios [F1]. Additional backstops consist of multi-hundred-million-dollar borrowing capacity from Federal Home Loan Bank advances ($510 million outstanding at year-end), federal funds lines (~$52 million available), and unused loan commitments exceeding $120 million—a figure elevated considerably over prior year reflecting expanded client draw rights post-acquisition [S4][S6][S11].

Standby letters of credit likewise climbed substantially to nearly $14.5 million serving commonly accepted guarantees for client transactions within prudent underwriting guidelines [S6]. These contingent liabilities underscore the necessity for robust collateral evaluations given their analogous risk profile to direct lending exposures.

A geographic concentration remains apparent—significant lending activity is anchored within Atlanta, Georgia, and New York City metropolitan statistical areas—heightening sensitivity not only around real estate cycles but also local regulatory or competitive market dynamics that can influence deposit growth or credit quality [S19][N1].

Future Growth Prospects and Regional Economic Risks

Growth prospects hinge significantly on tailoring residential real estate financing solutions responsive to local market conditions coupled with strategically leveraging SBA loan services which historically provide diversified revenue buffers during economic fluctuations [N1][S1]. Post-acquisition integration efficiency will dictate how soon scale benefits translate into margin expansion or cost synergies.

However, regional economic concentration imposes inherent limitations; localized downturns could reverberate disproportionately on loan performance given MetroCity’s high exposure within two urban centers—Atlanta and New York—which face distinct market pressures such as housing affordability constraints or commercial real estate occupancy trends.

Competitive dynamics typical of community banks emphasizing relationship-based service models require continuous adaptation in digital capabilities alongside traditional customer engagement methods—factors likely influenced by First IC's operational fit into MetroCity’s platform.

Capital Allocation: Dividends, Buybacks, and Shareholder Returns

Consistent with conservatively managed community banks deploying capital prudently amid growth phases, MetroCity incrementally raised dividends from $21 million paid in FY2024 to roughly $24.8 million in FY2025 representing progressive payout policies aligned with earnings improvement trends [F1]. Buyback activity remains modest yet resumed more actively post-acquisition with nearly $2.7 million repurchased shares compared to nominal prior outlays [$10k FY24], reflecting enhanced free cash flow generation but cautious capital stewardship priorities.

Together these actions support an approximate annual ROE near mid-teens percentages when considering net income relative to amplified equity levels—demonstrating balance between rewarding shareholders while retaining earnings for organic growth and regulatory compliance cushions.

Governance in Cybersecurity and Operational Controls

Cybersecurity oversight is clearly delineated within MetroCity’s governance framework featuring an Information Security Officer responsible for enterprise-wide cybersecurity program management encompassing risk assessment, vulnerability scanning, incident detection plus response & remediation efforts critical in financial institutions facing evolving cyber threats [S1].

The bank’s Information Technology Committee exercises direct oversight including chartered responsibilities like reviewing cybersecurity risks quarterly alongside full board updates ensuring top-level awareness aligns resource allocation effectively toward minimizing operational disruptions or data breaches.

Such structured governance aligns with best practices frequently adopted within mid-sized banks maintaining complex technology infrastructures balancing legacy systems integrations alongside emerging digital service offerings.

Key Milestones to Watch: Integration Outcomes and Credit Quality

While explicit forward-looking guidance remains absent concerning precise synergy targets or timeline completion parameters post-First IC acquisition, management signals focus areas around seamless operational unification particularly concerning loan servicing platforms and credit assessment consistency across combined portfolios [N1][S2]. Close monitoring of allowance levels tied to PCD loans acquired under business combination accounting will act as a bellwether for underlying credit quality trajectory.

Investors should also track quarterly disclosures related to total off-balance sheet exposures since these contractual obligations materially affect liquidity planning especially if drawn upon during stress periods.[N1] Monitoring emerging delinquency metrics across core SBA/residential real estate segments remain essential given their outsized portfolio representation influencing loss provisions moving forward.

Disclaimer: This analysis is for informational purposes only presenting factual details derived exclusively from provided company filings and news sources without any investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments