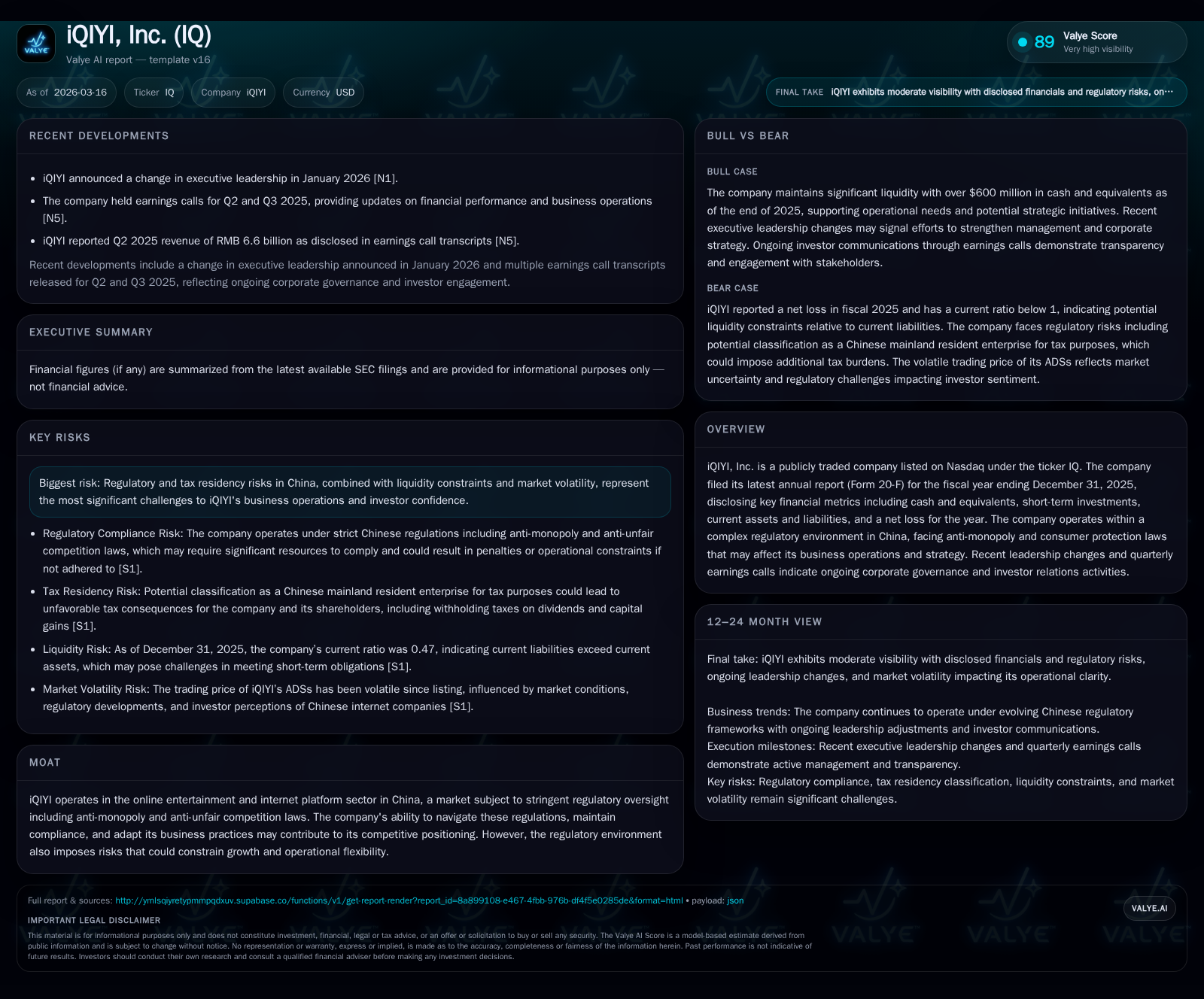

iQIYI's Financial Volatility Reflects Regulatory Strains and Business Model Evolution

iQIYI reported sharply reduced operating income in 2025 amid a challenging regulatory environment and strategic shifts toward diversified monetization.

iQIYI experienced a severe downturn in operating income and net profits in 2025 after steady growth over prior years, driven by regulatory pressures and the need to recalibrate its business model. Its core video streaming remains bolstered by AI and original content, but heavy regulatory scrutiny and constraints on cross-border finance impose growth limits. The company is modestly cash flow positive but remains unprofitable overall, with capital allocation decisions subject to structural complexities of its China-based operations. Future milestones to watch include regulatory compliance outcomes, monetization of experience businesses like iQIYI LAND, and navigating evolving foreign exchange mechanisms.

Past Growth and Historical Performance

iQIYI's financial trajectory through 2022–2024 reflected strong operational scaling with steadily rising operating income — increasing from $190.3 million in 2022 to a peak of $421.1 million in 2023 before retreating significantly in 2024 to $248.1 million [F1]. Net income also followed a similar pattern but with high volatility: from a net loss position of $19.7 million in 2022 to a robust $271.2 million profit in 2023, then dropping sharply to around $104.7 million profit in 2024.

The fiscal year ended December 31, 2025, saw operating income collapse by approximately 87% year-over-year to just under $33 million, coupled with a net loss of nearly $29.5 million—despite positive operating cash flows [F1]. Operating cash flows fell precipitously from $289.1 million in 2024 to just over $15.1 million last year, reflecting significant operational challenges possibly linked to regulatory constraints and market adjustments. iQIYI's capex increased moderately by about 26% year-over-year but remained relatively modest at $13.7 million [F1], indicating controlled investment spending.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -30 | 15 | 33 | 14 | -128.2% |

| 2024 | 105 | 289 | 248 | 11 | -61.4% |

| 2023 | 271 | 472 | 421 | 5 | +1473.2% |

| 2022 | -20 | -10 | 190 | 25 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1 | -1.6 |

| 2024 | 278 | 5.7 |

| 2023 | 467 | 15.8 |

| 2022 | -35 | -2.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not explicitly reported; focus is on profitability metrics per available filings [F1].

Business Model Drivers

iQIYI operates predominantly as an online entertainment platform anchored by an extensive content library featuring over 40,000 professionally produced long-form titles as of the end of fiscal year 2025 including dramas, films, variety shows, children’s content and animations [S19]. Original productions constitute the bulk of premium content supply—accounting for over 90% of newly released drama series rated highly on its proprietary popularity index.

Monetization stems chiefly from membership services offering ad-free premium experiences supported by subscription fees as well as brand advertising leveraging both traditional agency-sold campaigns and performance-based programmatic advertising driven by real-time bidding algorithms that optimize advertising effectiveness through user behavior analytics [S5][S11].

Complementing streaming revenue are diversified ancillary offerings: IP licensing agreements enabling third-party video recreations; distribution partnerships across Chinese mainland and overseas platforms; theatrical film releases; online game distribution with virtual item sales; talent agency services managing entertainers’ brand endorsements; and an expanding experiential business leveraging intellectual property through offline IP-themed venues—iQIYI launched its flagship iQIYI LAND amusement park focused on immersive VR-based attractions early in February 2026 aiming to build additional revenue streams beyond digital content monetization [S8].

Technological innovations underpinning these offerings include advanced AI integration—for example the Screenplay Studio AI system identifies promising scripts for production investment while interactive AI assistants enhance user experience via personalized recommendations and conversational plot insights [S19].

Regulatory Environment Impact

iQIYI faces significant headwinds stemming from tightening regulatory regime within China's internet platform economy sector. Amendments effective since mid-2022 strengthened the Anti-Monopoly Law’s enforcement scope with harsher penalties for abuse of market dominance—particularly related to discriminatory pricing tactics using big data analytics; exclusivity coercion with business partners; technology-based competitor interface blocking; forced bundling schemes; and excessive user data collection without consent [S4][S6][S10][S23].

Following intensive regulatory self-examination requirements issued collectively by the State Administration for Market Regulation (SAMR), Cyberspace Administration of China (CAC), and tax authorities starting in early-2021—and ongoing inspections—iQIYI has undertaken necessary rectifications including corporate restructuring efforts and review of past merger notifications impacting its investment strategy [S6][S7][S23]. Failure or insufficiency in compliance could lead to fines based on previous years’ sales revenue or even required divestitures.

Compounding these legal challenges is iQIYI's variable interest entity (VIE) corporate structure used for mainland China operations—a common workaround employed by internet firms restricted from foreign ownership—to manage compliance risks around control rights enforceability under PRC regulations [S4]. The company discloses explicit risks related to potential governmental reclassification or invalidation of its contractual business control arrangements which could severely impair operational continuity or asset ownership.

Furthermore the company's offshore holding entity must navigate uncertain rules pertaining to cross-border financing flows—the People's Bank of China’s (PBOC) Notice No.9 introduced complex risk-weighted loan limits tied to subsidiary net asset bases which remain subject to ongoing regulatory interpretation potentially constraining intragroup capital loans or equity injections critical for sustaining Chinese subsidiaries' liquidity and growth investments [S1][S12][S13][S15][S20].

Capital Allocation and Financial Health

iQIYI’s reported cash balance at the end of fiscal year 2025 stands robust at approximately $622.7 million in cash and equivalents; however current liabilities totaled roughly $3.16 billion versus current assets near $1.47 billion yielding a current ratio below unity at approximately .47 — signaling short-term liquidity tightness that warrants attention given contractual liabilities including lease obligations and debt maturities approaching imminently within next calendar year [F1][S17].

Significant debt obligations include convertible senior notes first issued in late-2020 with principal maturities due December-2026 amounting over $1 billion along with additional secured notes payable due in early 2028 raised from investor PAG Group that carries a higher coupon reflecting refinancing cost pressures amid volatile credit conditions for Chinese ADR issuers post regulatory clampdowns [S17]. Prior tender offers have reduced some note principal outstanding yet substantial refinancing or repayment solutions appear necessary within twelve months.

Subsidiary financial statements reflect accumulated losses across wholly owned mainland China entities preventing currently any dividend upstreaming based on PRC law requiring at least positive retained earnings plus allocable statutory reserves before distributions can be made—meaning shareholder returns remain on hold pending return-to-profit scenarios domestically [S9][S21]. Dividends are therefore discretionary by board resolution factoring ongoing operational needs alongside capital expenditure commitments primarily focused on infrastructure such as servers involved behind streaming service delivery.

Capital contributions to Chinese mainland subsidiaries must comply with registration requirements while loans are capped either by registered capital differences or risk-weighted asset limits under PBOC Notice No.9 mechanisms subject to SAFE registration or filing procedures—these controls shape the company's internal treasury management policy governing intercompany fund transfers tightly [S1][S9][S12][S13][S15].

Future Growth Prospects

iQIYI’s medium-term top-line growth hinges upon several interrelated factors:

- Continued success expanding original content franchises supported by proprietary AI-driven production efficiencies;

- Monetization ramp-up of newly developed consumer experiences like iQIYI LAND which represents both retail merchandise channels and immersive themed entertainment designed for repeat engagement;

- Expansion into overseas markets for Asian content leveraging local partnerships able to market culturally resonant programming;

- Optimization of advertising revenues via sophisticated performance-based bidding models unlocking enhanced yield from converging media consumption patterns;

- Effective navigation through evolving PRC platform economy regulations ensuring uninterrupted corporate operations;

- Management of foreign exchange controls related to repatriation rules that affect offshore funding flexibility.

However growth may be capped or uneven due to:

- Heightened anti-monopoly regulation risks potentially limiting aggressive market expansion or acquisition opportunities;

- Volatile credit markets challenging timely refinancing amid upcoming convertible note maturities;

- Uncertain enforcement trajectories regarding VIE legality impinging long-term strategic continuity;

- Possible further clampdowns on data privacy/use standards constraining personalized marketing practices;

- Competition intensifying both among domestic peers leveraging similar integrated content-IP ecosystems as well as global streaming giants expanding local-language offerings.

Milestones / What To Watch (Analysis)

In absence of explicit company guidance disclosed for future periods beyond early quarterly updates:

- Regulatory filings detailing progress or findings related to anti-monopoly inspections remain crucial indicators for risk management efficacy;

- Upcoming debt maturity dates within next calendar year will test capital structure resilience via refinancing announcements or repayment plans;

- Operational progress reports around expanded iQIYI LAND sites beyond initial launch will demonstrate effectiveness of experiential business diversification strategy;

- Subscriber metrics trends linked with premiere original content reception provide insight into membership revenue sustainability;

- Developments around cross-border financing policies post-PBOC Notice No.9 clarifications expected later may impact internal cash flow management.

Returns / Capital Allocation Review

iQIYI’s approximate return-on-equity was negative at about -1.6% for fiscal year ending December 31, 2025 reflecting ongoing unprofitability despite positive cash generation at operating level indicating continued reinvestment into growth initiatives or cost absorption related to regulatory compliance expenses [F1]. Free cash flow was marginally positive near $1.4 million after subtracting capex from operating cash flow—a narrowing gap signaling cautious spending aligned closely with operating inflows.

The board retains full discretion over dividend payments which have not been declared given loss positions across subsidiaries restricting upstream dividends pursuant to PRC laws mandating reserve fund accumulation prior distributions; share repurchase programs are similarly unconstrained formally but practically limited given liquidity pressures [S9][S18][S21]. Internal treasury controls tightly govern funds transfers between Cayman Islands holding entity and mainland subsidiaries ensuring compliance with SAFE registration requirements mitigating foreign exchange risk exposure but also limiting capital agility.

Conclusion

iQIYI navigates a uniquely challenging intersection of rapid digital entertainment evolution amid intense regulatory scrutiny shaping its operational landscape within China’s platform economy space. The dramatic earnings volatility witnessed up to fiscal year-end December 31, 2025—marked by steep declines following years of growth—reflects shifting dynamics influenced heavily by government enforcement priorities surrounding anti-monopoly laws and data governance.

Operationally diversified into original video content dominance complemented by emerging experiential IP merchandising ventures such as iQIYI LAND shows clear strategic intent towards multi-modal revenue generation beyond pure streaming subscriptions or advertisements.

Capital structure management emerges as another focal area amidst looming high nominal debt maturities demanding refinancing within restricted cross-border financing frameworks implemented under recent PBOC policies.

Future performance will depend substantially on iQIYI’s adaptability not only technologically—to sustain superior user engagement through AI enhancements—but also institutionally—to maintain alignment with rapidly changing PRC legal frameworks while preserving investor confidence across global capital markets.

This analysis is based on company-reported data as filed with the SEC up through March 16th, 2026 ([F1], [S#]) without speculative forecasting or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments