Calavo Growers Inc. Signals Earnings Rebound with Strategic Acquisition and Supply Chain Maneuvers

Calavo’s recent financial turnaround aligns with its pending acquisition by Mission Produce amid operational headwinds.

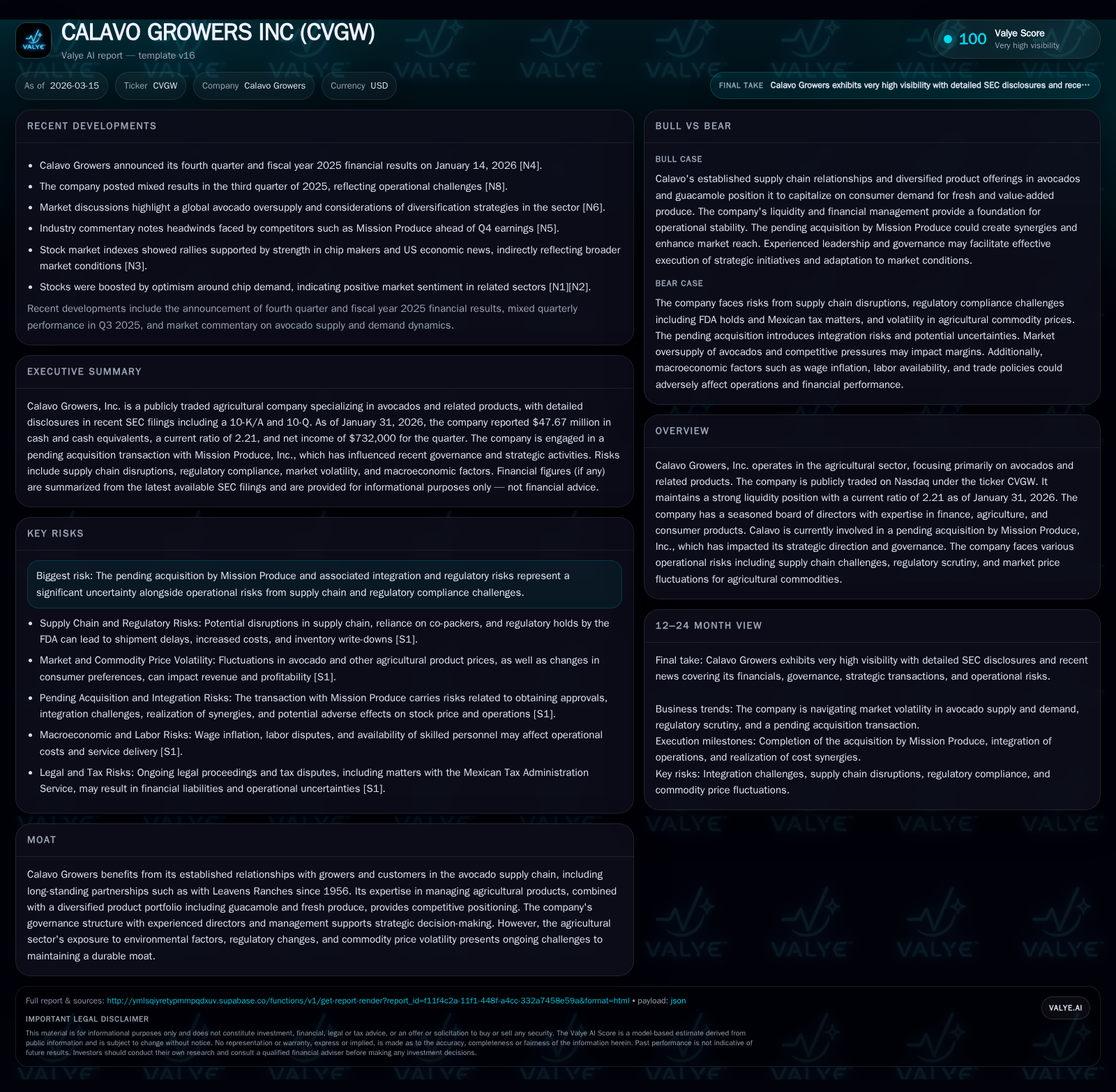

Calavo Growers has reversed prior losses, delivering positive net income and operating income in FY2025, supported by core avocado products and broadened offerings like guacamole. The company’s strong liquidity and capital structure provide a stable platform during its pending acquisition by Mission Produce, though regulatory and supply chain challenges weigh on operating margins. Investors should monitor integration progress and regulatory approvals as key milestones for future value realization.

From Losses to Profit: Charting Calavo’s Recent Financial Evolution

Calavo Growers has exhibited a marked financial transition culminating in an earnings rebound in fiscal year 2025. After net losses of approximately -$8.3 million in FY2023 and -$1.1 million in FY2024, the company recorded net income of about $19.8 million in FY2025 [F1], highlighting improved operational execution. Operating income rose to $19.6 million in FY2025 from $0.43 million in FY2023 and $16.7 million in FY2024 [F1].

Revenue has remained stable around $1.09 billion since FY2017 ($1.08 billion) through FY2018 [F1], with moderate year-over-year growth.

Operating cash flow was positive at $21.5 million for FY2025 despite a slight decline from $24.4 million in FY2024, while capital expenditures decreased to $2.15 million, reflecting a more capital-efficient approach [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 20 | 22 | 20 | 2 | +1939.8% |

| 2024 | -1 | 24 | 17 | 3 | +87.1% |

| 2023 | -8 | -14 | 0 | 11 | -33.5% |

| 2022 | -6 | 50 | 6 | 10 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 14 | 19 |

| 2024 | 9 | 22 |

| 2023 | 10 | -25 |

| 2022 | 5 | 40 |

Source: SEC companyfacts cache [F1].

Note: Revenue has been stable around ~$1 billion with a clear profit turnaround evident in recent years [F1].

Revenue Streams and Market Drivers: What Catalyzed Growth?

Calavo’s resilience is rooted in its vertically integrated avocado supply chain combined with a diversified product portfolio that includes guacamole and fresh-cut produce lines [S1]. These expansions help mitigate commodity-price exposure typical within agricultural operations.

Long-term partnerships support sourcing stability while innovation through branded products enhances consumer relevance and helps buffer revenue fluctuations amid macroeconomic uncertainties [S1].

The Mission Produce Deal: Strategic Implications and Future Pathways

The pending acquisition by Mission Produce is structured as a stock-and-cash merger providing approximately $14.85 per share alongside Mission shares [S11], targeting market scale synergies across marketing, distribution, IT systems, and procurement.

Shareholders face execution risks including government approvals, potential antitrust considerations given overlapping produce portfolios, and integration complexities across workflows and cultures [S6][S8][S10]. Management attention diverted toward transaction processes may temper near-term operational agility.

Regulatory authorities’ approval timelines remain critical milestones to watch [S6][S8][S10].

Operating Margins Under Pressure: Supply Chain and Regulatory Challenges

Margins face pressure from several fronts typical of the agricultural sector [S5][S7][S9]. Perishable logistics involve high handling costs exacerbated by FDA inspections that can cause shipment detentions requiring third-party testing or spoilage write-downs.

Price volatility due to seasonality or climatic disruptions impacts input costs unpredictably while USMCA-related tariffs introduced additional expenses that were not fully passed onto customers [S26]. Labor market tightness further inflates packaging and fulfillment costs.

Managing these supply chain complexities remains challenging given external factors beyond company control.

Liquidity and Capital Structure: Strength Amidst Transaction Uncertainties

Calavo maintains a solid liquidity profile with a current ratio of about 2.21 as of January 31, 2026, supported by current assets of approximately $153 million against current liabilities near $69 million [F1][S4].

Cash and equivalents stood at roughly $47.7 million supporting daily operations and providing leverage through the deal review process [F1][S7]. Equity reached nearly $207 million by fiscal year-end 2025 underpinning creditworthiness with minimal debt influence noted [F1].

Shareholder Returns: Dividends, Repurchases, and Return on Equity

Capital allocation reflects consistent dividend growth totaling about $14.3 million paid in FY2025 compared with approximately $8.9 million in FY2024; share repurchases have been negligible recently amid strategic uncertainties [F1][S12][S13].

Return on equity is estimated near 9.6% for FY2025 based on reported net income relative to equity base size, indicating healthier profitability trends within the agribusiness sector context [F1]. Executive compensation is aligned with financial performance metrics reinforcing governance focus on value creation [S12].

Key Milestones Ahead: What Investors Should Monitor

Investors should observe:

- Completion of regulatory approvals necessary for merger closing,

- Progress on integration plans including IT system consolidation,

- Customer retention or expansion post-announcement,

- Resolution timelines on litigation or tax issues affecting cash flow assumptions,

- Supply chain stabilization amid evolving FDA protocols impacting shipments [S3][S6][S8].

These milestones will be pivotal in validating the strategic benefits underlying the acquisition rationale.

Building Resilience: Agricultural Sector Risks in Focus

Calavo faces systemic risks common to agriculture including climate variability affecting avocado yields; phytosanitary regulations enforced by USDA-APHIS impacting import/export throughput; labor market tightness driving wage inflation; and logistics bottlenecks increasing spoilage risks if suboptimally managed [S5][S9].

Despite strong grower relationships that form part of Calavo’s competitive advantages, these exogenous factors require adaptive strategies rooted in sector expertise.

This analysis uses disclosed company data up to early-2026 filings without projections beyond reported figures or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments