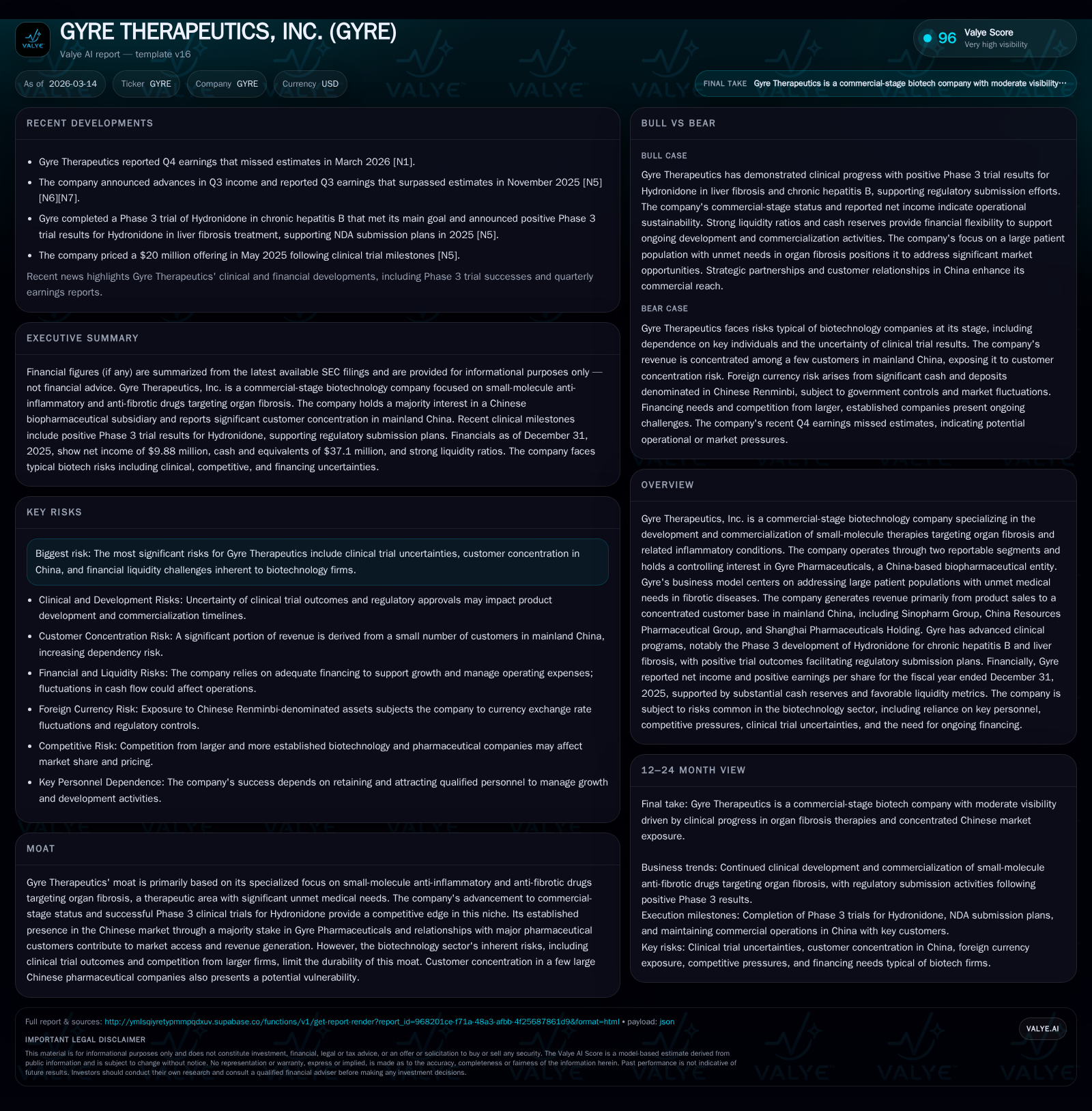

GYRE Therapeutics Boosts Profitability on China Pulmonary Fibrosis Sales with Pipeline Expansion Under Regulatory Scrutiny

GYRE’s revenue growth and Phase 3 liver fibrosis candidate propel financial turnaround, while customer concentration and multi-jurisdictional approvals remain key challenges.

Gyre Therapeutics operates as a commercial-stage biotech company with a strong foothold in the Chinese pulmonary fibrosis market alongside an expanding pipeline, including a promising Phase 3 candidate for liver fibrosis. Its financials show a turnaround from losses to profitability by 2025, driven by increasing revenues concentrated among key pharmaceutical customers. Future growth depends on regulatory approvals beyond China and successful product portfolio expansion, balanced against risks related to clinical trial outcomes, customer concentration, and liquidity. Capital allocation prioritizes R&D and commercial infrastructure without dividends or share repurchases.

Company Overview

Gyre Therapeutics, Inc. is a commercial-stage biotechnology firm specializing in small-molecule therapies for organ fibrosis and inflammatory diseases that address complex biological pathways involved in fibrotic progression. The company operates primarily through its majority-owned subsidiary Beijing Continent Pharmaceuticals Co., Ltd. (Gyre Pharmaceuticals) based in the People’s Republic of China (PRC), alongside U.S. operations headquartered in San Diego, California [S1]. Gyre has established a commercial presence with ETUARY® (pirfenidone), an approved treatment for pulmonary fibrosis marketed predominantly within China.

Historical Financial Performance

Gyre demonstrated a marked financial turnaround by FY2025 after several years of losses. Total revenue increased approximately 36.6% year-over-year to $127 million, reflecting growing sales of its marketed products primarily through three major Chinese pharmaceutical distributors: Sinopharm Group Co., Ltd., China Resources Pharmaceutical Group Ltd., and Shanghai Pharmaceuticals Holding Co., which together accounted for over 75% of total revenue [F1][S4][S5].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 10 | 1 | 11 | 1 | -44.8% |

| 2024 | 18 | -4 | 16 | 2 | +120.9% |

| 2023 | -85 | 26 | -67 | 9 | -937.1% |

| 2022 | -8 | -33 | -9 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 0 | 9.3 |

| 2024 | -6 | 28.3 |

| 2023 | 17 | 540.1 |

| 2022 | -34 | 38.0 |

Source: SEC companyfacts cache [F1].

The decline in operating income compared with FY2024 reflects increased general & administrative and selling expenses associated with international expansion and clinical development investments despite higher revenues [S23]. Net income decreased due partly to non-cash warrant liability adjustments [S25]. Positive operating cash flow after prior years' investment-heavy cycles signals improving operational efficiency; however, free cash flow remains slightly negative due to ongoing capital expenditures supporting R&D and production scale-up [F1][S24]. The company's equity base strengthened significantly via public equity offerings supporting operational continuity and pipeline advancement [F1][S21].

Pipeline and Growth Outlook

Gyre’s lead clinical asset Hydronidone (F351), targeting liver fibrosis—a condition prevalent particularly among Asian populations—has shown promising Phase 3 trial results that underpin planned regulatory submissions with the National Medical Products Administration (NMPA) in China. Parallel development efforts continue toward U.S. regulatory approval [S1][N1]. Expansion of indications for ETUARY® into additional fibrotic diseases represents another growth vector aimed at diversifying revenue streams.

Regulatory approval outside China remains uncertain with potentially protracted reviews; competitive dynamics include larger biopharma companies targeting fibrosis therapeutics globally. Clinical trial risks inherent to translational medicine could also impact product launch timelines or success rates [S1].

Capital Allocation and Financial Returns

With a return on equity estimated around 9.3% based on FY2025 net income relative to equity levels [F1], Gyre currently prioritizes reinvestment over distributions. There have been no recent dividends or share repurchase programs disclosed [S26]. Capital expenditures have moderated compared to prior years but remain necessary for advancing late-stage clinical programs and scaling manufacturing capacity [F1][S23][S24]. Equity financing activities have bolstered liquidity amid these expansion initiatives.

Liquidity remains robust with cash and equivalents totaling approximately $37 million at year-end 2025 plus substantial short- and long-term bank deposits exceeding insured limits under both U.S. FDIC and PRC Deposit Insurance System frameworks; this supports operational stability despite sector volatility [F1][S6][S7].

Market Positioning and Risks

Gyre’s specialized focus on organ fibrosis through small-molecule drugs addresses significant unmet needs but faces challenges including client concentration risk given reliance on three main customers dominating Chinese pharmaceutical distribution channels [S4][S5]. The company also faces standard biopharmaceutical risks such as clinical trial uncertainties, regulatory hurdles across multiple jurisdictions, competitive pressures from larger firms with broader portfolios, and dependency on sustained capital access.

Strategic Initiatives

Gyre announced a merger agreement with Cullgen Inc., intended to expand its capabilities; however, consummation is subject to shareholder approvals and regulatory conditions which may affect timing or realization of expected synergies [S1].

Conclusion

Gyre Therapeutics demonstrates a credible path toward sustainable growth balancing established commercial operations within China with advancing late-stage pipeline candidates addressing large-scale fibrotic diseases globally. Its financial trajectory shows significant improvement culminating in profitability supported by concentrated but stable revenues. The company maintains prudent capital allocation emphasizing reinvestment over distributions while managing liquidity prudently amid sector risks. Upcoming milestones include regulatory submissions for Hydronidone in China alongside efforts to broaden ETUARY® indications — pivotal events shaping Gyre's future competitive positioning.

This report is based solely on publicly available information as of March 2026 and does not constitute investment advice or recommendations regarding Gyre Therapeutics or any securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments