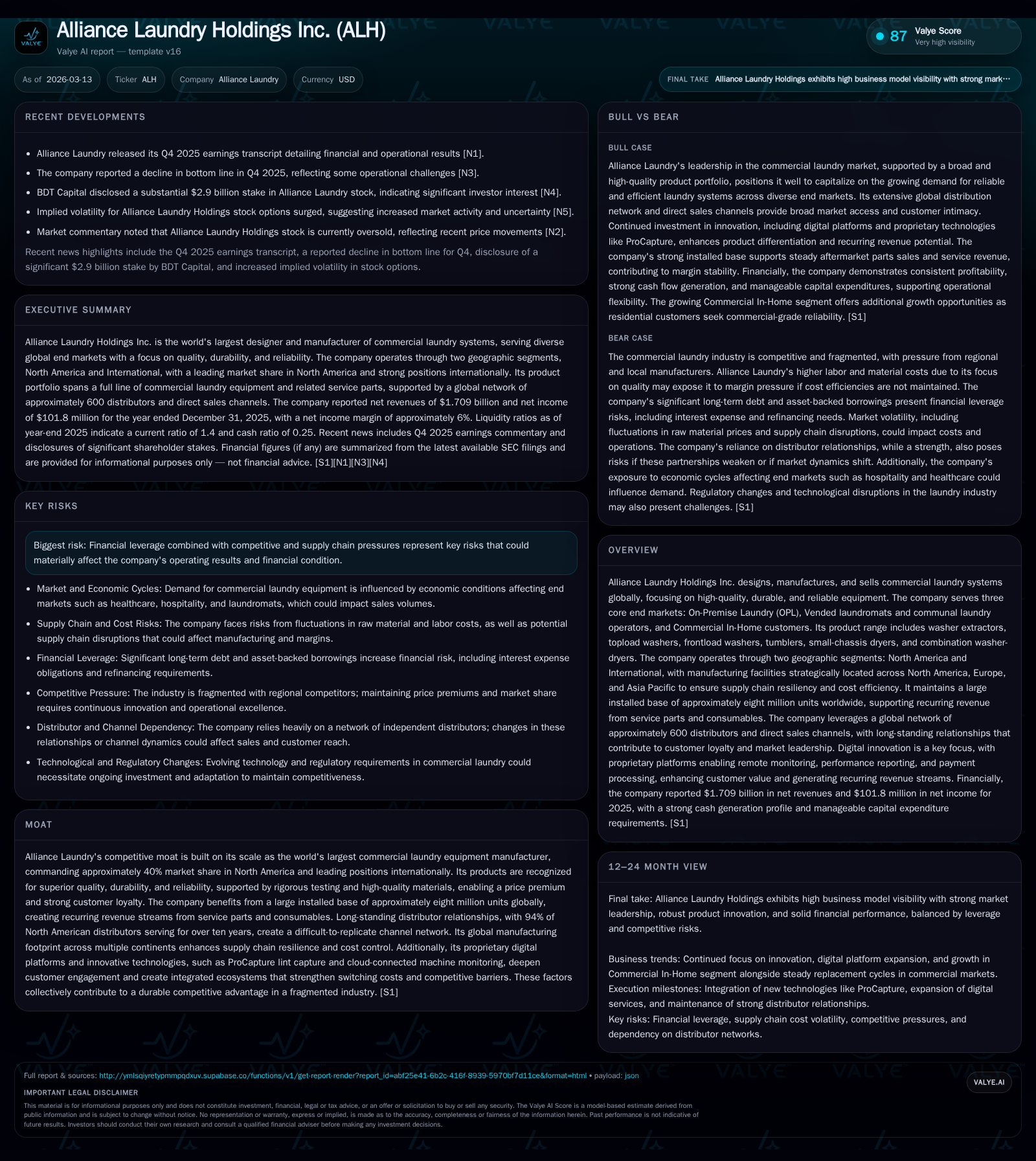

Alliance Laundry’s Market Power Drives Durable Growth and Capital Discipline

Alliance Laundry leverages its dominant market position, extensive installed base, and operational rigor to sustain consistent growth while strategically managing leverage and capital allocation.

Alliance Laundry Holdings benefits from its commanding ~40% North American market share and an installed base of approximately eight million units worldwide, which underpin predictable replacement demand. While competitive pressures and supply chain challenges compressed margins in 2025, the company’s diversified end-market exposure and global manufacturing footprint provide resilience. Significant debt reduction alongside disciplined reinvestment signals a balanced capital approach. Future growth depends on continued innovation, expansion into developing markets, and leveraging digital platforms to maximize aftermarket opportunities.

Historical Growth Anchored on Replacement Demand and Market Leadership

Alliance Laundry Holdings (ALH) has built a strong track record by capitalizing on regular replacement cycles associated with its expansive global installed base estimated at eight million commercial laundry units. This figure assumes an average ten-year useful life per machine, aligning with industry longevity norms for capital equipment in mission-critical applications like healthcare and hospitality [S1][S22]. The company holds approximately 40% share of the North American commercial laundry market, a cornerstone of its sustained demand profile and competitive advantage.

The company reported operating income of $317.4 million in fiscal 2025 alongside net income of $101.8 million [F1]. Figure 1 below provides a concise overview of key financial metrics from fiscal years 2023 through 2025.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Replacement demand linked to the aging equipment base remains a reliable revenue driver. ALH's incumbency advantage is reinforced by customers’ preference for proven durability, evidenced by premium pricing capabilities supported by high-quality materials usage and rigorous testing processes [S1][S22]. This combination drives both new unit sales aligned with lifecycle upgrades as well as sustained aftermarket revenue potential.

Diverse End-Market Exposure Mitigates Volatility and Fuels Continued Expansion

ALH's revenue streams benefit from broad end-market diversification across three core segments: On-Premise Laundry (OPL), Vended laundromats including communal facilities, and Commercial In-Home customers [S1]. This mix cushions business cycle impact as investment dynamics rarely align contemporaneously across these segments.

The OPL vertical serves specialized applications — ranging from hospital linens requiring sterilization to firefighting gear maintenance — reflecting complex user requirements that have historically limited commoditization [S1]. The vended segment experiences growth driven by mature market transitions toward commercially professional laundromat investments in the US & Western Europe combined with demographic trends expanding communal laundry acceptance in emerging regions. This heterogeneity balances cyclical exposure tied to real estate costs or regulatory changes affecting new site development.

Selective penetration into residential markets demanding commercial-grade reliability provides an emerging avenue for incremental expansion [S1]. Overall, this multifaceted approach helps ALH manage revenue volatility effectively while providing multiple levers for sustained growth.

Recent Earnings Snapshot: Margin Compression Amid Competitive and Supply Chain Pressures

Despite maintaining robust top-line stability in Q4 2025, ALH experienced operating margin pressures attributable to inflationary input costs and intensifying competition [N1][N3]. Cost inflation particularly affected procurement supply chains despite proactive supplier relationships aimed at stabilizing raw material prices [S17].

Management commentary highlighted ongoing initiatives to restore margins through operational efficiency gains coupled with selective pricing adjustments where justified [N1]. These near-term headwinds underscore the delicate balance between sustaining premium product positioning and responding to rising cost structures in a capital-intensive sector.

Strategic Outlook: Investing in Innovation, Expanding Footprint, Navigating Market Drivers

ALH plans capital expenditures around $60 million in fiscal year 2026 compared to $53.7 million spent in 2025 [F1][S8][S26]. Investments focus on capacity expansion, engineering advancements including proprietary filtration technologies reducing maintenance burdens (e.g., ProCapture Cyclonic Filtration), and enhanced digital platforms enabling remote machine monitoring for vended laundromat operators.

Manufacturing operations span six strategically located facilities across North America, Europe (Czech Republic), China, and Thailand—a "local-for-local" production strategy affording supply chain resilience against geopolitical or logistic disruptions [S22]. AI-powered defect detection systems reinforce quality while supporting continuous improvement programs essential to retaining technology leadership.

Growth catalysts include penetrating underdeveloped end-markets modernizing laundry infrastructures toward developed-market standards—a trend especially salient in Asia-Pacific regions where investment appetite and hygiene standards are rising [S1][N1].

Capital Structure Evolution: Significant Debt Reduction and Liquidity Position

A notable highlight for ALH’s capital discipline is meaningful deleveraging over the twelve months ending December 31, 2025. Total long-term debt reduced from approximately $2 billion at year-end 2024 down to roughly $1.35 billion at the close of 2025—a nearly one-third reduction catalyzed primarily by voluntary prepayments funded through IPO proceeds as well as free cash flow generation [F1][S4][S14][S21].

Cash and cash equivalents stood at $123 million as of December 31, 2025 [F1], supporting a current ratio around 1.4 which underpins near-term liquidity comfort amid scheduled interest payments estimated at approximately $79 million over the next year [F1][S11]. The credit facility includes a term loan maturing August 2031 plus revolving credit lines providing flexible liquidity options [S4][S14].

Capital Allocation Priorities: Growth Investment Versus Debt Paydown

Management adheres to a prudent capital allocation framework balancing reinvestment needs against aggressive debt reduction goals. No dividends have been declared or distributed since IPO, reflecting an intentional strategy geared toward strengthening balance sheet health before considering shareholder returns via dividends or buybacks [S1].

The company achieved an approximate return on equity of about 26%, signaling efficient utilization of equity capital amid ongoing leverage reduction [F1]. Free cash flow generated (~$158 million) provides substantial internal funding capacity enabling simultaneous funding of capex expansion alongside principal debt repayments without external financing dependency [F1][S8][S18].

This dual focus seeks to optimize financial flexibility while preserving competitiveness through innovation-led growth initiatives.

Recurring Revenues from Installed Base: A Moat-Defining Asset

Central to ALH’s enduring competitive moat is its global installed base approaching eight million machines deployed across roughly 150 countries—an ecosystem unmatched by competitors domestically [S22]. This sizable footprint cultivates sticky customer relationships anchored on system reliability criticality especially in healthcare settings or multi-location laundromats where downtime risks carry substantial operational penalties.

This installed base not only drives predictable hardware replacement demand but also generates recurring revenues via service parts and consumables sales—components representing a meaningful portion of total addressable market beyond initial equipment sales [S23]. Proprietary digital tools enabling remote management enhance aftermarket engagement strengthening lock-in effects by simplifying maintenance forecasting.

Together these factors consolidate barriers to entry while supporting premium pricing and steady cash flow visibility beyond pure unit volumes.

Risks to Monitor: Financial Leverage, Regulatory Hurdles, Macro-Economic Headwinds

While ALH enjoys robust structural advantages, it faces ongoing risks warranting vigilant oversight. Elevated financial leverage remains a key exposure particularly should macroeconomic headwinds impede EBITDA generation needed for covenant compliance or discretionary capital spending flexibility [S1]. Despite recent debt reduction success, geopolitical tensions or tightening credit conditions could elevate refinancing risks.

Increased regulatory burdens such as expanded permits or zoning requirements impact new laundromat construction timelines—a vital pipeline element for vended laundry system demand growth—and may introduce delays or increased project costs limiting near-term demand traction [S1]. Competitive intensity requires continual innovation investment lest price erosion accelerate.

Industry cyclicality tied to real estate costs, labor availability for laundromat operations, or shifts in consumer behavior remain externally uncontrollable variables necessitating adaptive management strategies.

This analysis is based solely on publicly available data including SEC filings ([F1],[S#]) and verified news sources ([N#]). It aims to provide an informed summary capturing Alliance Laundry Holdings’ performance dynamics without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments