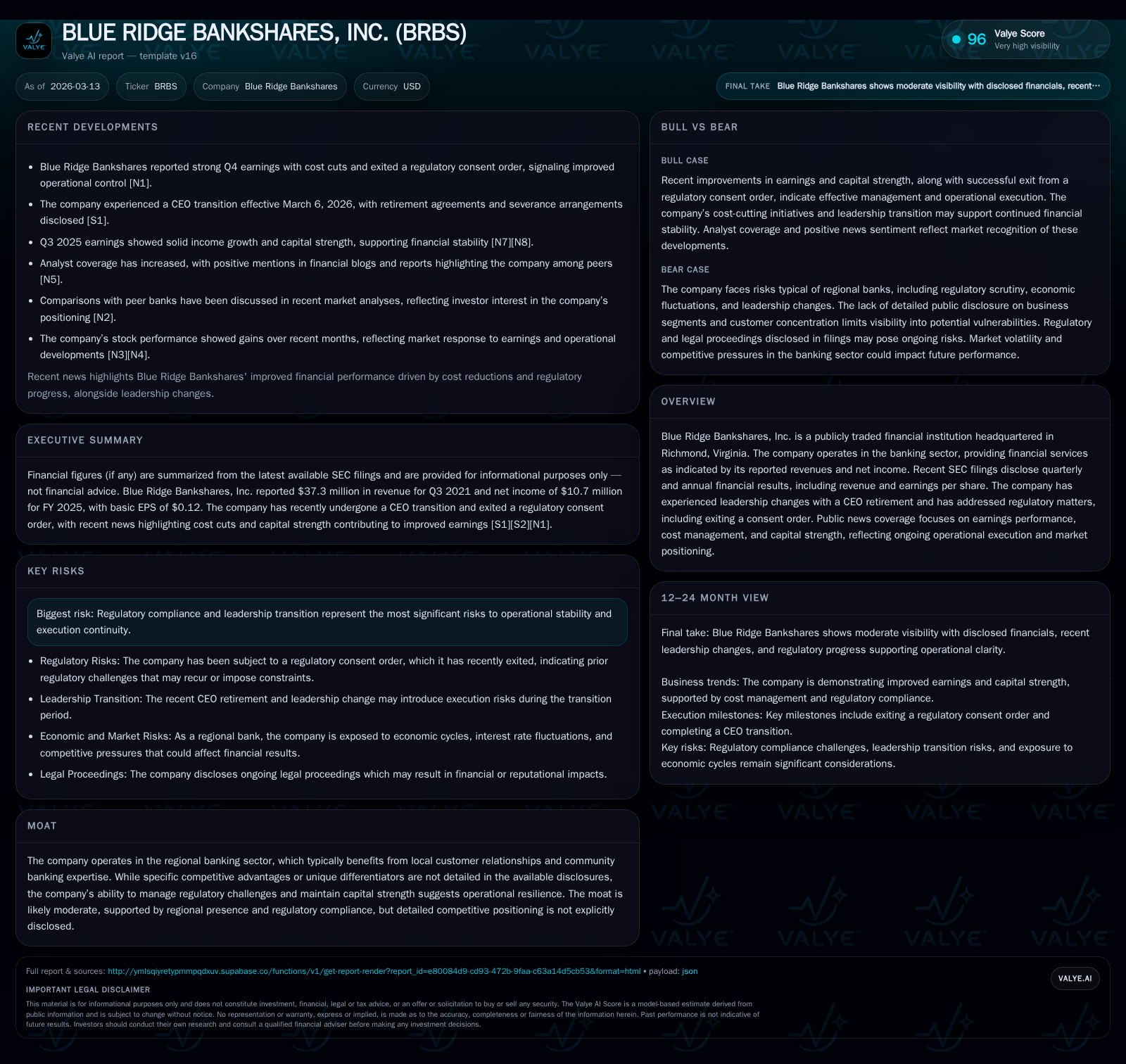

Blue Ridge Bankshares Rebounds: From Sharp Losses to Regulatory Exits and Cost Management Wins

A detailed review of Blue Ridge Bankshares’ financial recovery, leadership transitions, and operational improvements amid regulatory challenges.

Blue Ridge Bankshares, Inc. emerged from multi-year heavy losses with a notable turnaround to profitability in 2025, driven by improved cost management and successful resolution of a regulatory consent order. The recent retirement of CEO Billy Beale and appointment of credit veteran Harry Golliday as interim CEO marks a pivotal leadership shift with implications for ongoing credit risk oversight. The company’s balance sheet shows strengthening capital buffers post-clearance from regulatory constraints, while early signals from dividend declarations and cash flow improvements suggest cautious capital return efforts. Monitoring the permanent CEO search and continued regulatory climate will be essential in assessing future earnings momentum.

From Significant Losses to Profitability: Tracking Blue Ridge’s Financial Reversal

Blue Ridge Bankshares has traversed a volatile financial terrain over recent years, marked by sharp earnings declines followed by an encouraging rebound. The bank registered deep net losses of approximately -$51.8 million in fiscal year (FY) 2023 and a residual loss of about -$15.4 million in FY 2024, painting a challenging backdrop for regional banking operations amid macroeconomic pressures and internal adjustments [F1]. This trajectory sharply reversed in FY 2025, culminating in positive net income of $10.7 million — a remarkable swing of over $26 million compared to the previous year.

Revenue growth over this period was also striking; the firm more than doubled revenues between FY 2019 ($49.7 million) and FY 2020 ($111.3 million), with more stable levels reported thereafter leading into the turnaround year [F1]. Operating cash flows mirrored this pattern with FY 2023 enjoying strong inflows ($44 million), deteriorating sharply into a $-6.3 million outflow by FY 2024, then rebounding robustly to nearly $13.6 million positive cash flow in FY 2025 [F1]. Capital expenditures (Capex) also rose in that turnaround year to $1.68 million from under $600k the prior year, reflecting selective reinvestment within controlled budgets.

This erratic financial performance underscores a phase of credit portfolio normalization and adjustments typical for banks emerging from asset quality headwinds — though specific nonperforming asset data is not detailed here. The net income improvement suggests substantial operational leverage was captured upon stabilizing loan loss provisions and aligning expense structures with underlying business volumes.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 11 | 14 | 1679000 | +169.6% |

| 2024 | -15 | -6 | 588000 | +70.3% |

| 2023 | -52 | 44 | 961000 | -398.7% |

| 2022 | 17 | 94 | 455000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 12 |

| 2024 | -7 |

| 2023 | 43 |

| 2022 | 93 |

Source: SEC companyfacts cache [F1].

Table: Summary financial trends for Blue Ridge Bankshares showing key metrics derived from available data [F1].

Cost Discipline and Exit from Regulatory Oversight: Operational Drivers Behind the Turnaround

A defining component of the company's recovery was regaining operational freedom following exit from an OCC consent order on November 13, 2025—a formal regulatory sanction entered into on January 24, 2024 due to concerns about supervisory deficiencies [N1][S15]. Consent orders often constrain banks’ strategic initiatives by imposing strict capital planning requirements and mandating remediation steps across compliance and risk frameworks.

Blue Ridge's termination of this order signals effective compliance remediation and improved risk governance—critical achievements that enhance managerial latitude for capital deployment decisions including dividends or reinvestments [N1][S15]. Indeed, news reports highlight targeted cost reductions as a key lever supporting earnings resilience heading into late 2025 quarters, affirming disciplined expense management alongside revenue stabilization [N1].

Such cost discipline aligns with industry best practices under heightened regulatory scrutiny where banks calibrate personnel expenses, technology budgets, and discretionary spending to preserve capital while advancing compliance.

Leadership Transition: Implications of CEO Retirement and Credit Officer Appointment

Leadership dynamics took center stage recently when President & CEO G. William "Billy" Beale retired effective March 6, 2026 after several years at the helm during turbulent periods [S3][S14]. His departure coincided with his resignation from all board seats and officer positions.

The Board appointed Harry Golliday—previously Executive Vice President and Chief Credit Officer—as interim CEO simultaneously [S14]. Mr. Golliday brings considerable expertise from over three decades spanning CapitalOne Bank (including senior credit roles) plus tenures at SunTrust and Wachovia Banks focused on commercial banking and credit risk oversight.

This succession underscores prioritization of steady executive stewardship particularly around credit risk management—a critical facet given prior regulatory attention to asset quality issues that contributed materially to earlier losses [S4][S5]. Golliday’s background suggests a continuation of prudent loan portfolio monitoring strategies amid evolving market conditions, aiming to sustain progress made on provisioning adequacy while balancing growth opportunities.

Balance Sheet Health and Capital Strength After Regulatory Challenges

Blue Ridge’s equity base expanded significantly from about $92 million at end-2019 to almost $249 million as of end-2022 before moderating somewhat thereafter, reflecting capital injections parallel with loss-absorbing needs amid the troubled years [F1]. Although more recent pure equity figures for FY25 are not explicitly stated, calculated return on equity based on reported net income against prior equity approximates around 4.3%, indicative of cautious but improving capital efficiency during recovery phases [F1].

Multiple filings throughout late-2025 detail ongoing liquidity maintenance activities ensuring adherence to regulatory minimums while supporting loan demand fulfillment . The clearance from the consent order removes prior constraints on Tier 1 capital ratio targets, enabling normalized capital planning calibrated toward competitive positioning.

The bank likely continued building loan loss reserves tailored to observed asset quality trends as part of dynamic risk-adjusted balance sheet management common among regionals recovering post-stress episodes.

Capital Allocation Priorities: Dividends and Investment Trends

The Board declared a special cash dividend of $0.25 per share payable November 21, 2025—the first meaningful distribution since emerging from regulatory restrictions—reflecting incremental confidence in sustainable free cash flow generation consistent with prudent capital allocation philosophy [S20][F1].

Free cash flow computed as operating cash flow minus Capex stood near $11.95 million for FY25 (13.63m -1.68m), demonstrating tangible liquidity available beyond operational needs which could support ongoing dividends or opportunistic buybacks if aligned with shareholder value objectives [F1].

Investment in capital expenditures increased notably in FY25 compared to prior years, indicating selective reinvestment aimed at supporting operational enhancements amid disciplined cost management efforts reported by company communications [F1][N1].

Details on share repurchases are not prominently disclosed; however, given the recent emergence from regulatory constraints, measured approaches toward capital returns appear consistent with maintaining adequate buffers.

Outlook: Key Considerations Moving Forward

While no explicit forward guidance has been issued post-FY25 results [N1][S3], pertinent factors include:

- Completion timing of permanent CEO appointment following interim leadership,

- Sustained execution on cost containment balanced with revenue growth,

- Vigilance regarding evolving regulatory expectations impacting capital planning,

- Ongoing monitoring of credit quality trends amid economic uncertainties.

These elements will critically influence Blue Ridge’s ability to maintain earnings momentum established in FY25 while navigating competitive regional banking dynamics.

This analysis is based solely on publicly available information as cited herein without projecting or advising investment actions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments