Ascend Wellness Holdings' Growing Footprint Faces Regulatory and Profitability Challenges

A vertically integrated cannabis operator with strong retail presence navigates market constraints and operational losses.

Ascend Wellness Holdings, Inc. (AAWH) operates a multi-state vertically integrated cannabis business focused on adult-use markets in limited-license states across seven U.S. states. The company’s growth has been fueled by acquisitions, retail expansion, and product diversification, but recent financial results show a topline decline with ongoing operating losses. While Ascend benefits from regulatory licensing barriers and flagship retail locations, the complex U.S. cannabis regulatory environment, combined with persistent net losses and increasing competitive pressures, represent significant growth and profitability challenges going forward. Capital allocation remains focused on steady retail expansion, cultivation capacity enhancement, and omni-channel customer engagement.

Company Overview

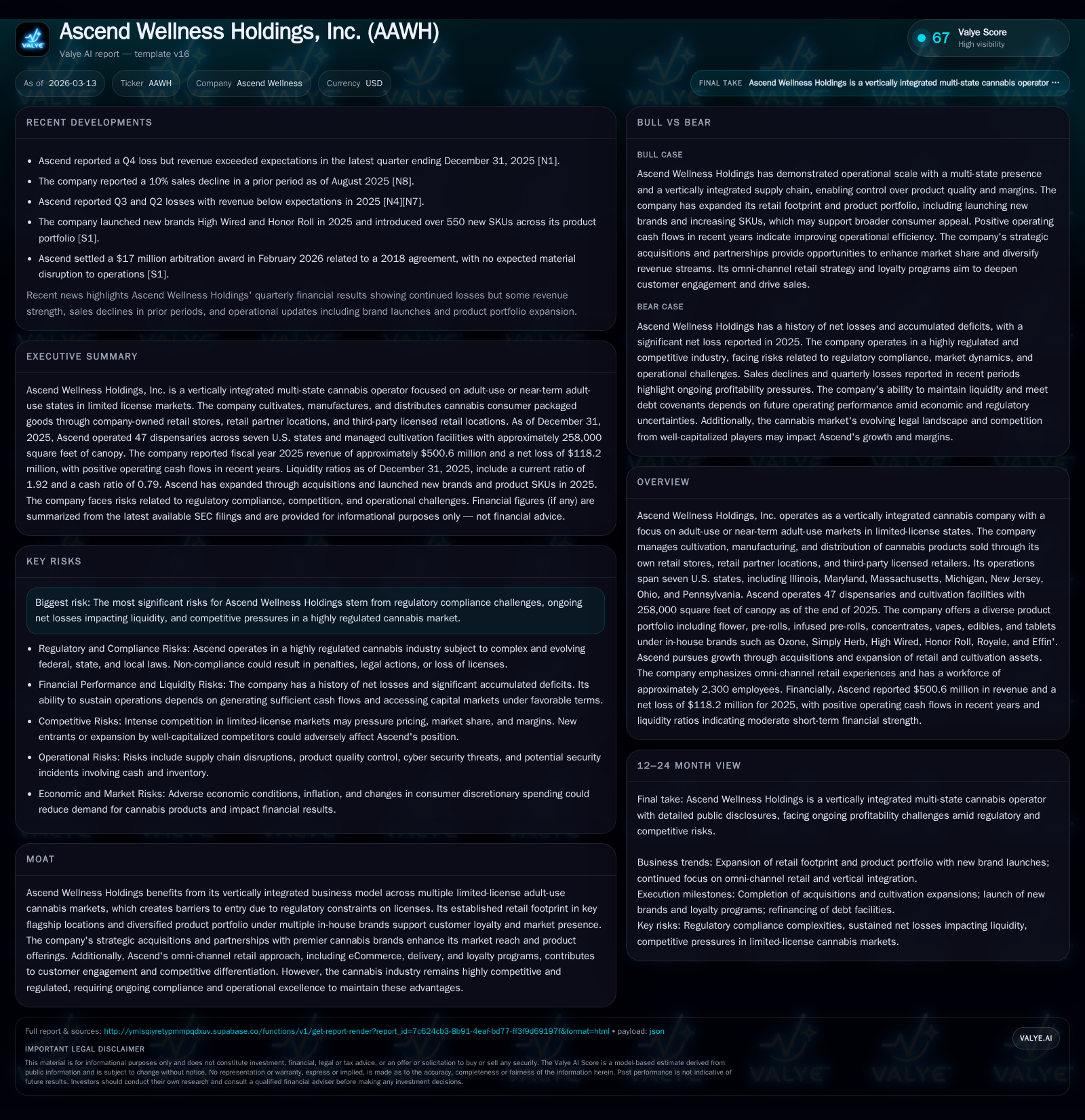

Ascend Wellness Holdings (AAWH) is a vertically integrated multi-state cannabis operator focused primarily on adult-use or near-term adult-use cannabis markets in limited-license states across the U.S. [S1][S8]. The company has a broad operating footprint spanning Illinois, Maryland, Massachusetts, Michigan, New Jersey, Ohio, and Pennsylvania, operating a total of 47 dispensaries and cultivation facilities by the end of 2025 with approximately 258,000 square feet of canopy space [S1][S16].

Founded in 2018 initially in Illinois, Ascend rapidly expanded through acquisitions and organic growth to establish significant presence in several key limited-license jurisdictions where market entry barriers reduce direct competition from new entrants [S1][S24].

The company's vertically integrated business model includes cultivation, manufacturing, and wholesale distribution of cannabis products sold through company-owned stores, retail partner locations, and third-party licensed retailers [S8][S16]. Its portfolio features multiple proprietary brands such as Ozone (core lifestyle brand), Simply Herb, High Wired, Honor Roll, Royale, and Effin', alongside partnerships with recognized brands like Miss Grass and Lowell Smokes which offer complementary consumer reach [S14][S25].

Historical Financial Performance

Ascend’s revenue trajectory peaked at $561.6 million in FY2024 before contracting by about 10.9% to $500.6 million in FY2025 [F1]. This decline reflects pressures related to market dynamics including competitive pricing stress and demand factors. Operating income similarly deteriorated from a modest profit of $4.7 million in FY2024 to an operating loss of $17.0 million in FY2025—a swing driven by increased operational costs or margin compression [F1]. Net income figures show sustained losses historically; the last reported net loss was -$80.9 million for FY2022 with no public net income figure for FY2025 disclosed yet [F1].

Operating cash flows present a more constructive picture with positive CFOs recorded over the last three years including $38.1 million generated in FY2025 despite net losses [F1]. Capex expenditure has steadily ranged between $22–26 million annually supporting facility expansions including cultivation canopy growth [F1]. This investment supports Ascend's strategy to increase scale and refine efficiencies.

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Rev YoY |

|---|---|---|---|---|---|

| 2025 | 501 | 38 | -17 | 26 | -10.9% |

| 2024 | 562 | 73 | 5 | 23 | +8.3% |

| 2023 | 519 | 75 | -4 | 24 | +27.8% |

| 2022 | 406 | -38 | -8 | 82 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | 12 |

| 2024 | 51 |

| 2023 | 51 |

| 2022 | -120 |

Source: SEC companyfacts cache [F1].

Growth Drivers and Limitations

Ascend’s strategy centers on leveraging its vertical integration within predominately limited-license markets—five of which cap the number of operational licenses—thus erecting substantial barriers against competitors [S24]. Its focus on flagship retail locations situated near major highways or high-traffic commercial nodes provides defensible positions that facilitate consumer access and brand prestige [S14][S24]. The company actively pursues partnerships with social equity license holders expanding retail footprints while also investing in omni-channel capabilities including a revamped eCommerce platform, robust loyalty programs ('Ascenders Club'), reserve-online-pickup-in-store options, delivery services across multiple states, curbside pickup as well as online consultations to create differentiated customer experiences [S8][S12].

Product innovation spans flower products through a wide array of vapes, infused pre-rolls, edibles (with recent emphasis on micro-dose formats), concentrates, tablets, and several new SKUs launched across established markets in recent years [S14][S25]. Strategic partnerships with premier brands broaden the assortment reaching diversified consumer segments.

The company targets growth through expansion of retail locations (aiming for around 60 by medium term), organic cultivation scale-ups (via adding canopy), wholesale distribution increases to third-party retailers mainly in Illinois, Massachusetts, New Jersey coupled with enhancing same-store sales productivity [S16][S25].

Key internal efforts include rationalizing supplier relationships for cost efficiencies and standardizing packaging procurement favoring recycled or biodegradable materials showing commitment to ESG principles [S12]. Cultivation operations emphasize controlled environmental conditions optimized via drip irrigation systems alongside LED lighting aimed at sustainable yield improvements while managing energy consumption effectively [S12][S14].

Growth Constraints

Despite these strategies, Ascend faces notable headwinds:

- Federal illegality under the Controlled Substances Act creates inherent regulatory uncertainty that can impact licensing renewals or enforcement approaches; federal legalization or interstate commerce reform may introduce large-scale entrants disrupting current market dynamics which currently favor well-capitalized license holders like Ascend but could compress margins through intensified competition from national players [S11][S19].

- Persistent inability to generate net profits despite positive operating cash flows suggests challenges balancing growth investments versus operational leverage; margin compression risk remains if wholesale or retail pricing pressure intensifies amid oversupply scenarios or economic slowdowns affecting discretionary consumer spending [F1][S10][S19].

- Compliance burdens are substantial given varied state-specific regulations governing marketing restrictions, product labeling requirements and quality controls increasing overhead costs while limiting traditional advertising avenues compared to other FMCG sectors [S23].

- Labor union activities covering roughly one-third workforce add wage cost pressures alongside potential operational constraints if negotiations falter or strike risks materialize [S17].

- Expansion into new states depends heavily on obtaining limited licenses amid uncertain timelines for regulatory approvals which can delay anticipated revenue contributions while elongating payback periods for invested capital [S22].

Forecasts and Milestones: What to Watch

The latest full-year reported revenue contraction accompanied by operating losses sets a cautious tone despite management’s commitment toward expanding retail outlets toward their medium-term target (~60 stores including partner-operated locations) and enhancing cultivation footprint beyond current ~258K sq.ft canopy as capital allocation allows [N1][S16][S25].

Investors should monitor quarterly updates for inflection points such as return to operating profitability stemming from efficiency gains or scaling benefits coupled with sustained top-line stabilization or recovery following recent declines reported in Q4/2025 [N1]. Additionally:

- Progression on social equity partnerships expanding reach into untapped demographics may drive longer-term volume growth.

- Scaling wholesale partnerships beyond existing strongholds could improve margin profiles if product mix tilts toward higher value-added SKUs.

- Regulatory developments at federal level especially around legalization frameworks will significantly affect market structure assumptions.

- Capital raises under the effective shelf registration allowing up to $100 million issuance capacity could be an indicator of funding runway extension or acquisition plans if announced.

Returns and Capital Allocation

As per the latest filings ending December 31, 2025:[F1] Ascend held cash and equivalents totaling approximately $85.7 million alongside current assets over twice current liabilities yielding a current ratio near 1.92 indicating manageable short-term liquidity.

Despite operating losses (-$17 million EBIT FY2025), the company generated positive operating cash flow approximately $38 million supporting reinvestment into capex totaling about $26 million maintaining development momentum across facilities.[F1]

Free cash flow approximates $12 million (CFO minus capex), signifying some cushion post-investment although tighter compared to prior years' higher CFO levels.[F1] The company maintains substantial debt loads including senior secured notes issued in July 2024 amounting over $250 million cumulatively subject to restrictive covenants impacting flexibility but has demonstrated capacity for refinancing prior credit facilities proactively.[S4][S26]

No dividends were declared reflecting management prioritization on growth reinvestment over shareholder payouts given prevailing business stage.[S6]

Return on equity is not meaningful due to negative equity position around -$47 million as of end-2025 resulting chiefly from accumulated deficits nearing half a billion dollars since inception plus sizable accumulated net losses.[F1]

Industry Context Analysis

The highly regulated nature of U.S. cannabis markets means operators like Ascend benefit substantially from license scarcity which limits new entrants but also requires ongoing operational excellence given evolving regulation layers ranging from local zoning constraints through tight product compliance mandates. Brands must differentiate not only by product quality but by enhanced experiential retail models using technology-powered omnichannel integration increasingly critical due to competitive saturation particularly within premier metropolitan areas.

Large national MSOs have signaled appetite for consolidation pushing valuations up yet threatening margin compression long term especially where supply-side expansions outpace demand growth amid macroeconomic uncertainties impacting discretionary dollar flows. Labor market pressures further impact unit economics given cannabis verticals' labor intensity spanning specialized cultivation workers through experienced budtenders essential for brand consistency.

Regulatory developments expected include FDA guidance potentially formalizing quality controls or usage recommendations which may restrict some formulations or potency levels affecting innovation pace. Simultaneously federal rescheduling or legalization could trigger industry-wide shifts enabling interstate commerce but inviting deep-pocketed competitors requiring adaptation from current regional-centric players like Ascend.

Summary

Ascend Wellness Holdings stands as a prominent vertically integrated cannabis operator leveraging substantial presence across multiple limited-license adult-use states complemented by deep retail footprints situated at strategic high traffic locations that create durable market advantages. However underlying financials reveal margin pressures evidenced by a recent top-line decline coupled with recurring operating losses though resilient positive cash flows suggest core operating traction supporting continuous investment. The company’s future prospects hinge critically upon navigating evolving regulatory landscapes domestically while executing disciplined expansion balancing organic store openings against partner engagements plus scaling newly launched product lines aimed at broadening consumer appeal. Persistent industry risks involving legal status uncertainties alongside intensifying competition warrant ongoing scrutiny pertinent to capital structure management given sizeable debt levels. Overall Ascend exemplifies a mid-tier MSO balancing promising scale benefits against intrinsic regulatory complexities characteristic of nascent U.S medical-adult use cannabis sector poised at inflection between fractured state-centric markets transitioning toward potential broader federal acceptance.

This analysis is based solely on information provided in public filings up to March 13, 2026 ([F1],[N1]-[N3],[S1]-[S29]) without any forward-looking price speculation or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments