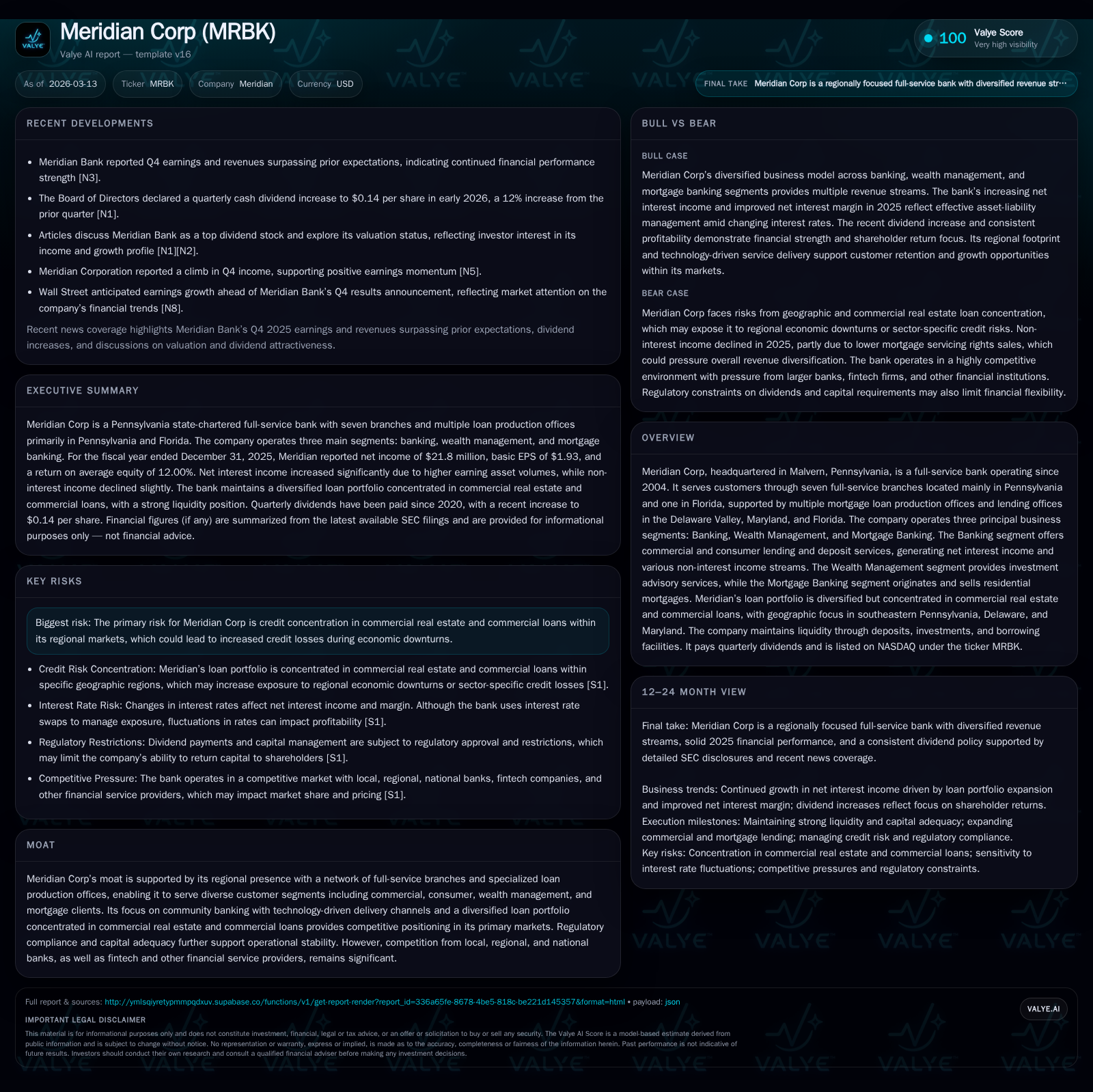

Meridian Corp Leverages Branch Network and Conservative Credit to Drive Investor Value

Meridian Corp’s regional banking approach and disciplined capital management underpin strong 2025 earnings and cash flow growth.

Meridian Corp reported a 33.6% increase in net income for FY2025, alongside a more than 150% surge in operating cash flow, driven by its diversified loan portfolio and efficient branch operations concentrated in the Delaware Valley and Florida markets. The bank’s commercial real estate and commercial loan concentration presents credit risk but also supports yield stability amid competitive pressures. Strong liquidity, a well-capitalized balance sheet, and steady dividend payments illustrate prudent capital allocation, though share repurchases remain suspended since 2023. Monitoring loan quality trends and mortgage banking performance will be pivotal in assessing the bank’s 2026 trajectory.

A Track Record of Income Growth and Efficiency Gains

Meridian Corp demonstrated robust profitability improvement in fiscal year 2025, with net income increasing by 33.6% year over year to $21.8 million from $16.3 million reported in FY2024 [F1]. This surge was complemented by an even sharper rise in operating cash flow (CFO), which more than doubled from approximately $9.6 million in FY2024 to nearly $24.3 million in FY2025, reflecting stronger cash generation from core banking operations [F1]. Capital expenditures increased significantly to $1.7 million in FY2025 compared to just $568,000 the prior year [F1], signaling elevated investments likely related to expansion or upgrading of branch infrastructure or digital platforms.

Equity rose to nearly $200 million by end-2025 from $171.5 million at end-2024 [F1], supporting an estimated return on equity (ROE) of approximately 10.9% for FY2025 based on net income relative to equity [F1]. Efficiency gains likely stemmed from optimized deposit-gathering activities and expanding lending margins across its segments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 22 | 24 | 2 | +33.6% |

| 2024 | 16 | 10 | 1 | +23.4% |

| 2023 | 13 | 19 | 2 | -39.3% |

| 2022 | 22 | 85 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 6 | 23 | |

| 2024 | 6 | 0 | 9 |

| 2023 | 6 | 4 | 17 |

| 2022 | 11 | 13 | 82 |

Source: SEC companyfacts cache [F1].

The data illustrates Meridian's recovery and growth post-2023 with sustained earnings momentum into 2025.

Commercial Real Estate Concentration: Risk and Reward Dynamics

Meridian’s loan portfolio is notably concentrated in commercial real estate (CRE) loans representing approximately 41% of total loans held for investment as of December 31, 2025—a level consistent with the prior year [S16][S19]. This portfolio is concentrated primarily across southeastern Pennsylvania, Delaware Valley tri-state areas, Maryland markets, and Florida [S1][S5]. While CRE concentrations heighten credit risk during economic downturns due to local market sensitivity [S15], they also support yield stability compared with more traditional consumer lending products.

The company manages credit risk through collateralized lending practices and underwriting diligence [S15][S19]. Non-performing loans have increased modestly—particularly within small business loans and residential mortgages—lifting the non-performing assets ratio from approximately 1.90% in December 2024 to about 2.38% as of December 31, 2025 [S17]. Correspondingly, the allowance for credit losses rose to $21.6 million reflecting heightened provisioning [S17]. Sector expertise combined with geographic familiarity helps Meridian navigate these risks while maintaining competitive yields.

Branch Footprint and Mortgage Operations as Growth Engines

Meridian operates seven full-service branches predominantly across Pennsylvania’s Main Line suburbs—including Wayne (headquarters), West Chester, Media—and extends presence to Florida with a branch in Bonita Springs [S1]. Complementing branches are multiple mortgage loan production offices throughout the Delaware Valley region plus Maryland lending offices facilitating residential mortgage origination and sales activity [S1][S5].

This structure separates deposit gathering via branches from mortgage-driven fee income generated by loan production offices that sell nearly all residential loans to third-party investors [S5]. Mortgage banking revenue arises from net interest on held loans plus gains on sales and servicing fees; although recent reductions in residential mortgages held reflect portfolio adjustments compared with prior periods [S18], this segment remains an important contributor to non-interest income diversification.

Wealth Management’s Role in Diversifying Revenue Streams

Meridian Wealth Partners LLC operates as a registered investment advisor providing wealth management services generating recurring advisory fees that add non-interest income stability less sensitive to credit cycles or interest rate fluctuations [S5]. This complements traditional banking revenues and aligns with Meridian’s community-focused strategy across its regional footprint.

Operating expenses related to marketing and payroll are managed efficiently relative to segment income before taxes indicating scalability potential within this division [S5].

Liquidity and Debt Structure Supporting Robust Operations

Meridian maintained strong liquidity totaling approximately $346 million at December 31, 2025—up from about $316 million one year earlier—including cash equivalents and marketable securities valued near $193 million dominated by agency securities [S6][S8][S17].

Borrowing capacity with the Federal Home Loan Bank (FHLB) reached a maximum of roughly $751 million available against pledged collateral such as mortgages and commercial loans [S4][S6]. Outstanding borrowings include long-term fixed-rate repos at coupons around mid-4%, alongside short-term borrowings supported by unsecured revolving lines totaling $56 million across correspondent banks [S6][S20].

Subordinated debentures totaling just under $50 million carry fixed interest rates above 6%, classified mostly within Tier 2 capital supporting regulatory compliance while providing cost-effective funding instruments [S6][S18].

Deposits grew by about +7.6%, exceeding $2 billion at year-end primarily through money market/savings accounts ($1 billion+) plus brokered time deposits (~$500 million), reflecting diversified funding sources offsetting wholesale borrowing risks [S20]. This mix supports operational flexibility and regulatory mandates including prompt corrective action requirements.

Capital Deployment: Dividends, Buybacks, and Regulatory Compliance

Meridian emphasizes prudent capital management balancing dividends with conservative share repurchase activity that ceased after plan expiration in late 2023 following cumulative repurchases near $20 million since inception [F1][S23]. Despite rising earnings (+33%) in FY25 dividends remained stable at approximately $5.7 million annually illustrating retention priorities toward organic growth or balance sheet strengthening rather than aggressive payout hikes [F1][S23].

Regulatory capital ratios reinforce confidence with Meridian classified as "well capitalized" holding Tier 1 leverage ratios comfortably above minimums along with adoption of the Community Bank Leverage Ratio (CBLR) framework reporting capital buffers exceeding the elected threshold of 9%, specifically posting a ratio of about 9.50% at year-end 2025 up from prior years [S4][S26].

This status ensures cost-effective compliance amid evolving supervisory scrutiny while benefiting from Basel III simplifications granted for community banks under asset thresholds below $10 billion.

Outlook: Key Milestones and Market Factors to Monitor

Q4 earnings releases early January revealed results surpassing consensus expectations indicating continuing positive momentum into fiscal year end [N1][N8]. Dividend yield attractiveness has been highlighted by market commentary emphasizing Meridian's stable distributions amid industry headwinds posed by fintech competition and evolving CRE conditions [N5][N6][N7].

Key watch points include potential pressures from rising non-performing credits within CRE versus opportunities from wealth management expansion which may partially insulate earnings volatility [S15][N7]. Regulatory developments impacting capital requirements could necessitate strategic adjustments especially if asset growth accelerates beyond community bank classifications.

Mortgage banking performance tied closely to interest rate trajectories also requires monitoring given origination volumes affect fee income potential amid shifting housing demand dynamics.

This analysis incorporates information derived solely from company disclosures including SEC filings,[F1] recognized financial data sources, market reports without any speculative assertions or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments