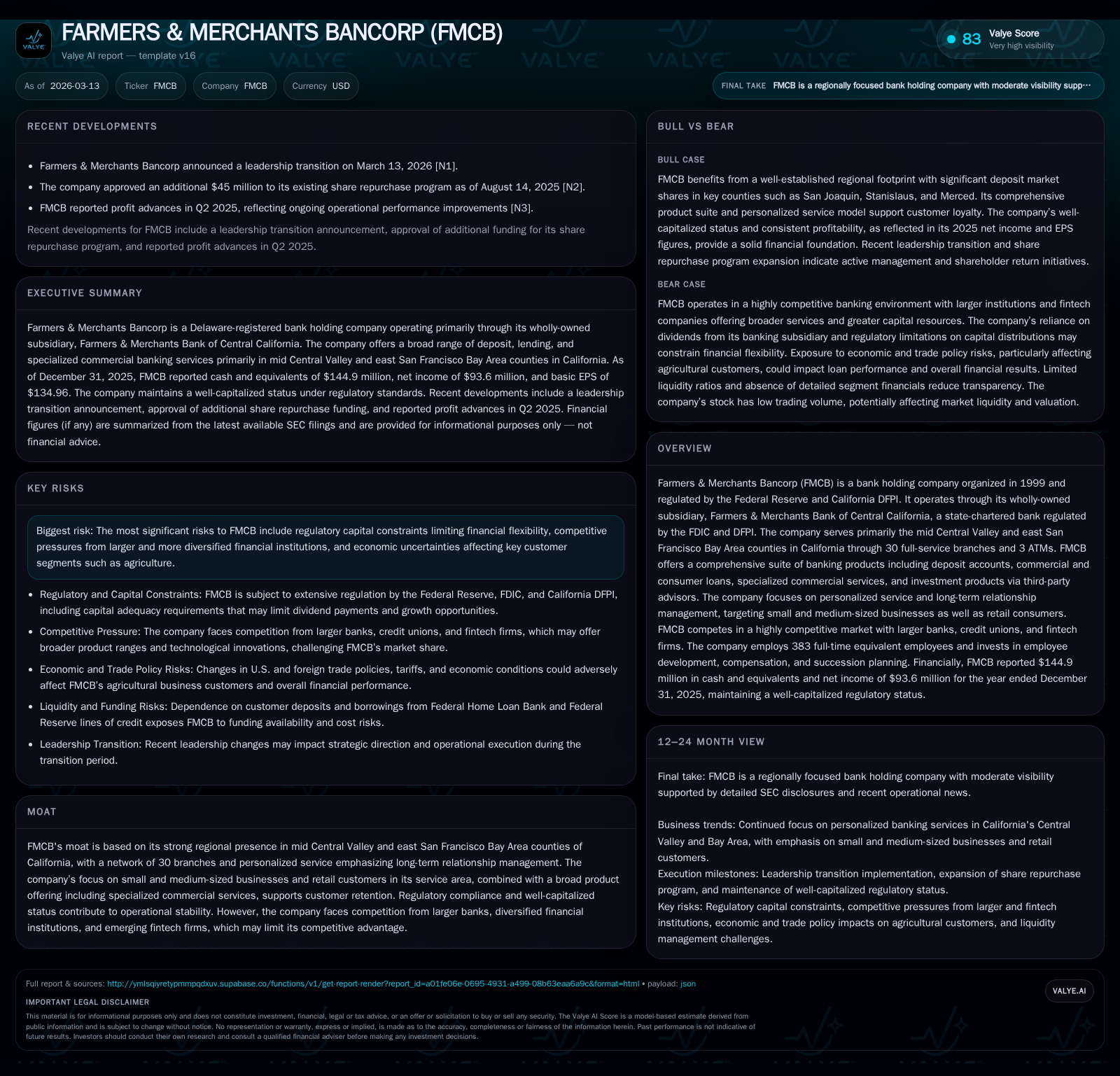

Farmers & Merchants Bancorp Sustains Regional Banking Strength Through Conservative Growth and Capital Management

FMCB leverages deep regional ties and a broad product suite to sustain steady income growth and robust capital buffers amid competitive pressures.

Farmers & Merchants Bancorp (FMCB), a California-focused bank holding company, has demonstrated consistent profitability with net income increasing nearly 6% year-over-year through 2025. The company’s historical growth has been driven largely by targeted lending to small- and medium-sized businesses in its mid Central Valley and East Bay markets. FMCB maintains a well-capitalized balance sheet, supporting dividend payouts and modest share repurchases. Looking ahead, growth hinges on navigating regulatory capital constraints, economic headwinds impacting local agriculture and real estate sectors, and intensifying competition from larger banks and fintech entrants. Monitoring deposit trends and regulatory developments will be critical to assessing FMCB’s future performance trajectory.

Company Background and Regional Niche

Farmers & Merchants Bancorp (FMCB) operates principally through Farmers & Merchants Bank of Central California, a state-chartered FDIC-insured institution with roots dating back to 1916. As a Delaware-registered bank holding company since 1999, FMCB is regulated under both Federal Reserve and California DFPI oversight [S1, S8]. Its footprint centers on mid Central Valley counties including San Joaquin and Stanislaus as well as parts of the East Bay in California, leveraging a network of 30 branches and three ATMs.

The company’s moat derives from its localized presence focusing on small- to medium-sized commercial clients alongside retail consumers within this region. Complementing deposit products with commercial loans, real estate financing, agribusiness exposure, specialized treasury services, and access to third-party investment advisors constitutes a comprehensive offering designed around relationship banking principles [S8]. Despite its community orientation, FMCB competes against much larger financial institutions alongside an expanding cadre of credit unions and less regulated fintech firms [S10].

Historical Performance Drivers

Between fiscal years 2022 and 2025, FMCB recorded net income growth from approximately $75M to $94M—a compound improvement driven by modest expansion of loan portfolios tailored for local business sectors plus stable deposit base evolution [F1]. The approximate return on equity for FY2025 stood at 14.5%, indicating effective capital utilization within risk constraints common among community banks [F1]. Operating cash flows have remained strong over the same period at around $100M annually, supporting the liquidity necessary for operational needs and planned capital expenditures.

Capital investments notably increased by over 200% year-over-year in 2025 to $7.58M, reflecting investments likely focused on technology upgrades or branch improvements—a trend consistent with regional banks modernizing their infrastructure to meet competitive pressures [F1]. While buybacks declined sharply in dollar terms in FY2025 versus prior years ($2.93M vs >$20M), dividends maintained continuity with quarterly payments funded through subsidiary dividend flows [F1, S26].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 94 | 104 | 8 | +5.8% |

| 2024 | 88 | 104 | 2 | +0.2% |

| 2023 | 88 | 93 | 5 | +17.6% |

| 2022 | 75 | 102 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 97 | 14.5 |

| 2024 | 45 | 101 | 15.4 |

| 2023 | 20 | 88 | 16.1 |

| 2022 | 20 | 98 | 15.5 |

Source: SEC companyfacts cache [F1].

Net income growth reflects steady regional credit demand; elevated capex in FY25 may signal technology modernization.

Regulatory Capital Status and Liquidity Profile

FMCB maintains a solid capital posture consistent with regulatory well-capitalized categorizations under Basel III frameworks as reflected in its Tier 1 leverage ratio above prescribed minimums [S11,S12]. The bank has not utilized Federal Home Loan Bank advances or Federal Reserve borrowings as of year-end reporting periods—demonstrating internal liquidity strength despite volatile broader credit conditions impacting regional banks nationally since early-2023 banking sector turmoil [S4,S6,S7].

The Company’s ability to pay dividends is limited only by regulator-defined capital preservation rules which FMCB comfortably meets given the subsidiary Bank’s retained earnings capacity estimated at $131.8 million available for upstream transfers at December 31, 2025 [S26]. However, evolving regulatory risks including potential tightening capital requirements and consumer protection regulations pose ongoing challenges that may hedge future operational flexibility [S13,S14,S16].

Competitive Environment and Sector Pressures

California's banking landscape is inherently competitive: FMCB contends against major national banks serving broader markets with more diversified loan portfolios while also facing community-based competitors such as credit unions specialized fintech entities offering innovative digital products outside standard regulatory regimes [S10,S22]. Declining relative deposit market share near ~2% across key counties (San Joaquin:13%, Stanislaus:9%, Merced:9%) illustrates competitive encroachment especially in consumer deposits where scale drives pricing advantages [S9].

Nationally chartered trust banks endeavoring into digital asset custody and related services challenge traditional deposit-taking models by delivering banking-like products lacking FDIC insurance but appealing due to innovation speed [S10]. For FMCB, this necessitates ongoing investment in technology infrastructure expansion evidenced by capex uptick as well as emphasis on personalized relationship management—a traditional defensive stance still relevant given loyal commercial client relationships.

Economic Exposure and Risk Considerations

Regional economic drivers heavily influence FMCB's portfolio quality and loan demand profiles; the company's client base encompasses significant agricultural businesses sensitive to U.S.-China trade tariff disruptions enacted since mid-2024 affecting commodity exports [S2]. Real estate market downturn risks remain palpable given commercial real estate concentration within service counties prone to cyclical fluctuations [S13,S19].

Monetary policy uncertainty—including interest rate stabilization at tighter levels despite recent Fed rate cuts—and geopolitical tensions add volatility layers influencing credit costs and asset valuations [S13]. Such externalities amplify inherent risks in managing uninsured deposits estimated at $2.6 billion as of end-2025 plus dependence on regional economic health.

Cybersecurity threats represent an operational risk vector increasingly prioritized amid complex data privacy legislations such as GLBA amendments or California Consumer Privacy Act implications—missteps here could trigger significant legal penalties or reputational loss [S17,S19].

Leadership Shift and Strategic Outlook

A leadership transition announced in early March 2026 introduces potential strategic inflections for FMCB’s near-term direction though specifics remain undisclosed [N1]. Given the company’s steady historical trajectory emphasizing conservative growth via niche client servicing backed by robust capital buffers, strategic continuity balanced with selective modernization investments appears probable.

Looking ahead without explicit accompanying company guidance, it is prudent to watch three main indicators: deposit base trends amid rising competition; regulatory developments especially surrounding community bank capital frameworks like the CBLR proposal though FMCB has not opted in yet [S15]; and loan portfolio performance particularly in agri-business sectors exposed to tariffs.

Capital Allocation Discipline

FMCB has shown prudence combining shareholder returns through quarterly dividends funded by substantial operating cash flows while ramping up capital expenditures cautiously without overly aggressive buyback programs—the latter reduced noticeably in FY25 compared to prior years signaling a more conservative cash deployment stance amidst uncertain macro backdrop [F1,S26]. Capital adequacy ratios underpin safe dividend payout capacity but constrain errant leverage increases.

Conclusion

Farmers & Merchants Bancorp remains emblematic of a traditional Californian community bank undertaking measured growth strategies rooted in regional economic linkage rather than rapid expansion or product diversification beyond core competencies. Its financial results exhibit resilience with solid profitability accompanied by strong cash generation and equity reinforcement. Challenges persist primarily from regulatory dynamics governing capital allocation flexibility alongside intensifying competition born from technological innovation disrupting traditional banking models. For stakeholders monitoring community banking effectiveness within concentrated geographies like Central Valley California, FMCB offers insight into balancing steady-state operations while navigating sector-wide transformation impulses.

This analysis is based on information available as of March 13, 2026, including recent SEC filings , news releases [N1], and detailed financial data from public disclosures [F1]. It is intended solely for informational purposes without making any investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments