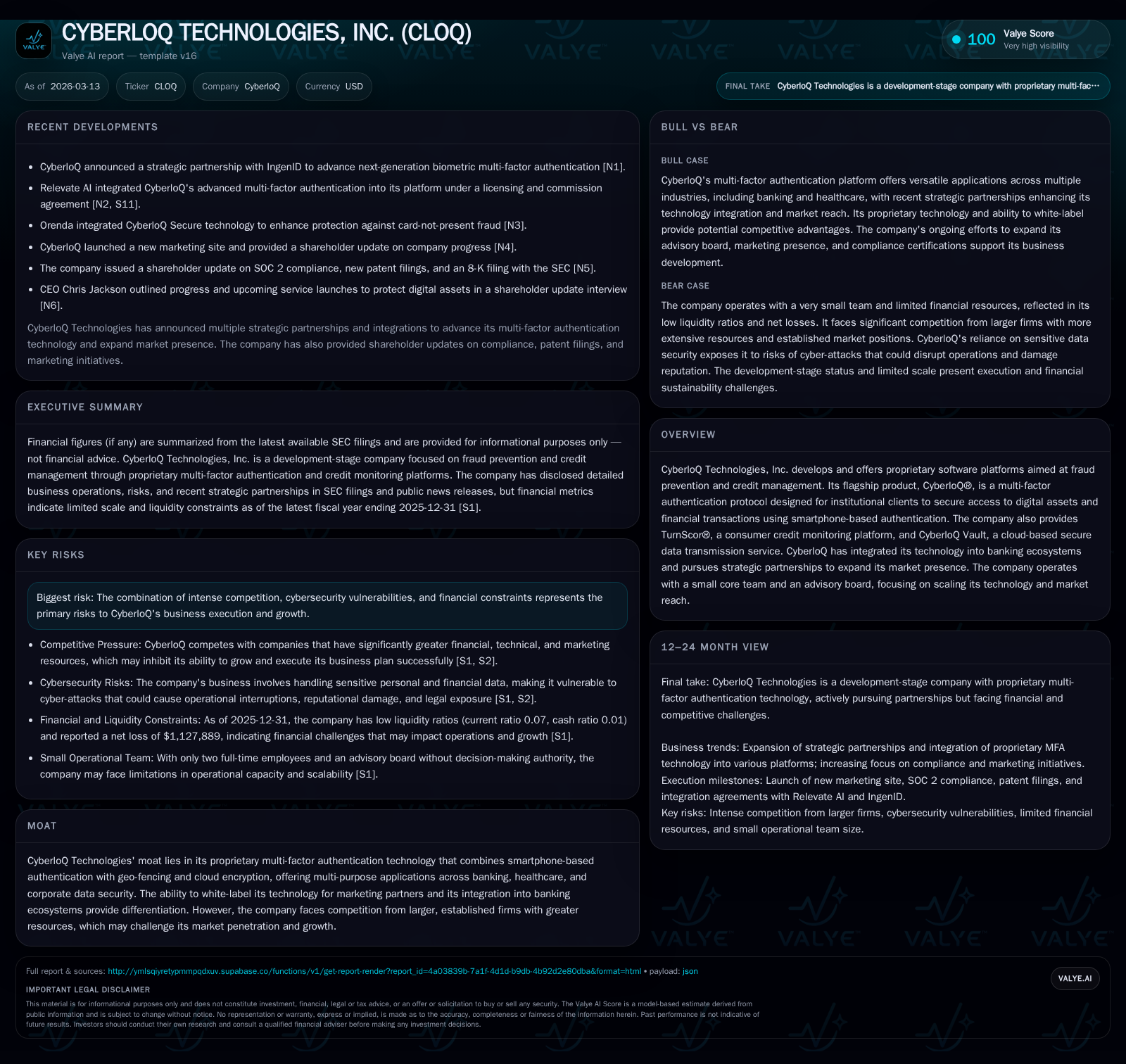

CyberloQ Technologies Battles Resource Constraints and Market Competition with Multi-Purpose Authentication Platform

CyberloQ's proprietary multi-factor authentication and secure data solutions target fraud prevention in financial and healthcare sectors.

CyberloQ Technologies, Inc. offers a multi-factor authentication (MFA) platform alongside credit monitoring and secure data transmission services. Despite technological differentiation through geo-fencing and cloud encryption, CyberloQ faces substantial challenges from better-resourced competitors. Its financials reveal ongoing operating and net losses with razor-thin liquidity, highlighting the capital constraints weighing on scalability. Strategic partnerships and patent pursuits provide potential avenues for growth, though market penetration remains an uphill battle.

Company Overview and Business Model

CyberloQ Technologies, Inc., incorporated initially as Advanced Credit Technologies in 2008 and rebranded in 2019, is a development-stage software firm specializing in fraud prevention through multi-factor authentication (MFA) protocols. Its flagship product, CyberloQ®, leverages smartphone-based MFA combined with geo-fencing and cloud encryption to secure institutional clients against unauthorized access to digital assets—primarily targeting banking ecosystems but also applicable across healthcare for protecting personal identifying information (PII) and corporate databases.

Besides CyberloQ®, the company offers TurnScor®, a consumer credit monitoring platform designed for individual users but also marketed as a value-added benefit via institutional clients. Additionally, CyberloQ Vault provides cloud-based secure data transmission using authenticated geo-coordinates and device verification to mitigate risks inherent to traditional email communication.

Historical Financial Performance

CyberloQ’s top-line has dramatically contracted from previous highs of over $10 million in revenues back in 2018 to just $197 reported in FY2021 (latest available revenue figure) [F1]. This steep decline underscores difficulties transitioning from development-stage status into commercial success. Operating losses have been recurring and expanding, increasing from approximately -$367K in FY2023 to -$772K by FY2025 [F1]. The net income trend mirrors this trajectory, deepening losses to over -$1.12 million by FY2025.

The company continues to burn cash meaningfully with operating cash flows turning more negative each year (-$775K in FY2025). Limited capital inflows are evident given negative equity standing of roughly -$1.67 million as of FY2025-end alongside a precarious liquidity position; current liabilities exceed current assets by over tenfold at year-end 2025, resulting in a critically low current ratio of approximately 0.07 [F1].

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -1127889 | -775051 | -771616 | -14.0% |

| 2024 | -989452 | -715123 | -752929 | +3.6% |

| 2023 | -1026530 | -340780 | -367250 | -4.8% |

| 2022 | -979048 | -371963 | -682337 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | ROE% |

|---|---|---|

| 2025 | 67.7 | |

| 2024 | 100.1 | |

| 2023 | 50000 | -234.8 |

| 2022 | 50000 | -5763.9 |

Source: SEC companyfacts cache [F1].

Table: Selected financial metrics from filings; amounts in USD

Growth Prospects and Market Positioning

CyberloQ’s core competitive edge lies in its proprietary MFA technology that synergistically combines smartphone authentication with geo-fencing enforcement and cloud-based encryption. This layered security approach enables multi-purpose applications:

- Banking: Secures debit/credit card usage thresholds and transaction legitimacy.

- Healthcare: Protects digitized medical records containing PII.

- Corporate Data Security: Guards databases against unauthorized external intrusion.

Further differentiation stems from the platform’s ability to be white-labeled for partners, enabling integration flexibility into diverse client offerings across industries—a noticeable advantage given incumbent competitors’ more siloed approaches.

Nonetheless, CyberloQ contends with entrenched rivals holding far greater financial muscle and market penetration such as Wells Fargo’s "on/off" card feature or Discover Card's "Freeze It" functionality alongside Ondot Systems’ established mobile card security presence [S1/S2]. The challenge remains translating technological uniqueness into wide-scale client adoption amid these incumbents’ brand trust and capital advantages.

In early 2026, CyberloQ announced a strategic partnership with IngenID aiming to enhance its biometric multi-factor authentication capabilities—signaling an effort to integrate advanced biometric modalities beyond smartphone tokens into the platform [N1]. Concurrently, it entered a licensing agreement with Relevate AI whereby CyberloQ’s MFA is integrated into Relevate’s platform as an authentication option generating modest license fees plus user-based commissions starting February 2026 [S17]. These deals exemplify tactical moves towards recurring revenue streams leveraging partnerships rather than direct sales alone.

Another promising avenue is the patent protection pursued specifically aimed at combating fraud within Medicare/Medicaid sectors—an area rife with digital identity challenges representing potentially lucrative vertical expansion beyond traditional banking targets [S18].

Future Outlook and Key Milestones to Monitor

While explicit future guidance has not been disclosed by management per filings available up to Q4’25 [S1/S2], critical indicators for progression include:

- Expansion of institutional client base utilizing the CyberloQ platform or TurnScor bundled offerings.

- Commercial scaling of cybersecurity protocols validated by SOC 2 Type II certification following the Type I certification obtained in April 2025 providing third-party validation of internal controls and security posture [S18].

- Progression on patent grants defining intellectual property moat effectiveness especially within healthcare fraud prevention.

- Renewal or expansion of collaboration agreements such as IngenID or Relevate AI beyond initial terms impacting recurring revenue growth potential.

- Improvements in capital structure enabling increased staffing or marketing spend vital for customer acquisition given current two-person full-time employee count limits internal bandwidth severely [S10].

Capital Allocation & Returns Analysis

CyberloQ currently operates under significant financial constraints reflected in persistent operating losses surpassing $750K annually and net losses exceeding $1 million recently without any reported dividend issuance or meaningful share buybacks aside from minor repurchases totaling $50K previously around FY2022/23 periods [F1][S15]. Cash reserves remain thin with about $45K cash equivalents last reported (September 2023), vastly overshadowed by current liabilities upward of $4.16 million at end-2025 suggesting heavy reliance on external financing cycles or restructuring events for operational continuity [F1][S7][S10].

The return on equity appears anomalously positive at approximately +67.7% for FY2025 based on simple net income-to-equity ratio calculation—but this figure is misleading given negative shareholders' equity reflecting balance sheet deficits rather than earnings strength; thus no true earning power can be inferred from ROE here absent normalized equity levels [F1].

Overall capital strategy seems weighted towards technology development investments funded via equity issuances or debt instruments rather than shareholder distributions indicating focus remains on business survival and growth phase funding rather than return maximization priorities presently.

Industry Context & Competitive Dynamics (Analysis)

Multi-factor authentication stands as a foundational pillar for enterprise-grade cybersecurity frameworks globally amid escalating fraud sophistication. Integration of geo-fencing is less common yet growing as firms seek context-aware access controls enhancing perimeter defenses especially relevant for mobile transactions. White-label SaaS-oriented MFA platforms cater well to banks wary of replacing legacy systems outright but willing to bolt-on advanced security modules collaboratively. However, scale economics dominated by large incumbents possessing extensive sales channels remain formidable barriers for emerging players like CyberloQ attempting broad adoption.

Additionally, regulatory drivers such as tightening data privacy laws interplay heavily with demand for encrypted secure data transmission solutions akin to CyberloQ Vault systems—another vector toward differentiated market penetration if execution succeeds.

Risks Summary

Key risks epitomize competition from resource-rich incumbents that could outpace product development or leverage existing customer relationships more effectively. Economic pressures compounded by ongoing operating losses emphasize risk relating to sustaining operations absent capital infusion or profitable contracts. Furthermore cybersecurity companies face intrinsic vulnerability threats wherein breaches could inflict reputational setbacks damaging client trust significantly—potentially crippling for a small vendor reliant on proving security efficacy continuously [S4/S5/S6/S12].

Conclusion

CyberloQ Technologies finds itself at a crossroads emblematic of many niche cybersecurity developers attempting scale without adequate financial backing or operational heft relative to entrenched competitors. Its technologically sophisticated offering with multi-factor smartphone integration augmented by geo-fencing positions it uniquely across multiple verticals including finance and healthcare data security domains. Nevertheless persistent revenue declines alongside mounting losses underscore fundamental commercial execution challenges intertwined with limited employee resources.

Successful navigation toward sustainable growth likely hinges on leveraging strategic partnerships like those formed recently with IngenID and Relevate AI while securing meaningful institutional client wins tied explicitly to patented technology advantages—particularly within specialized sectors such as Medicare/Medicaid fraud deterrence. Vigilance regarding quarterly operational milestones including license fee uptakes or contract renewals will be crucial barometers watching forward progress beyond development-stage profile toward scalable commercial viability.

This analysis is based solely on publicly available regulatory filings and press releases up to March 13, 2026. It is intended informationally without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments