Vuzix Corp's Revenue Rebound and Persistent Profitability Challenges in AR Innovation

Vuzix leverages its proprietary waveguide optics and in-house manufacturing as it expands smart glasses sales, yet continues to face significant operating losses.

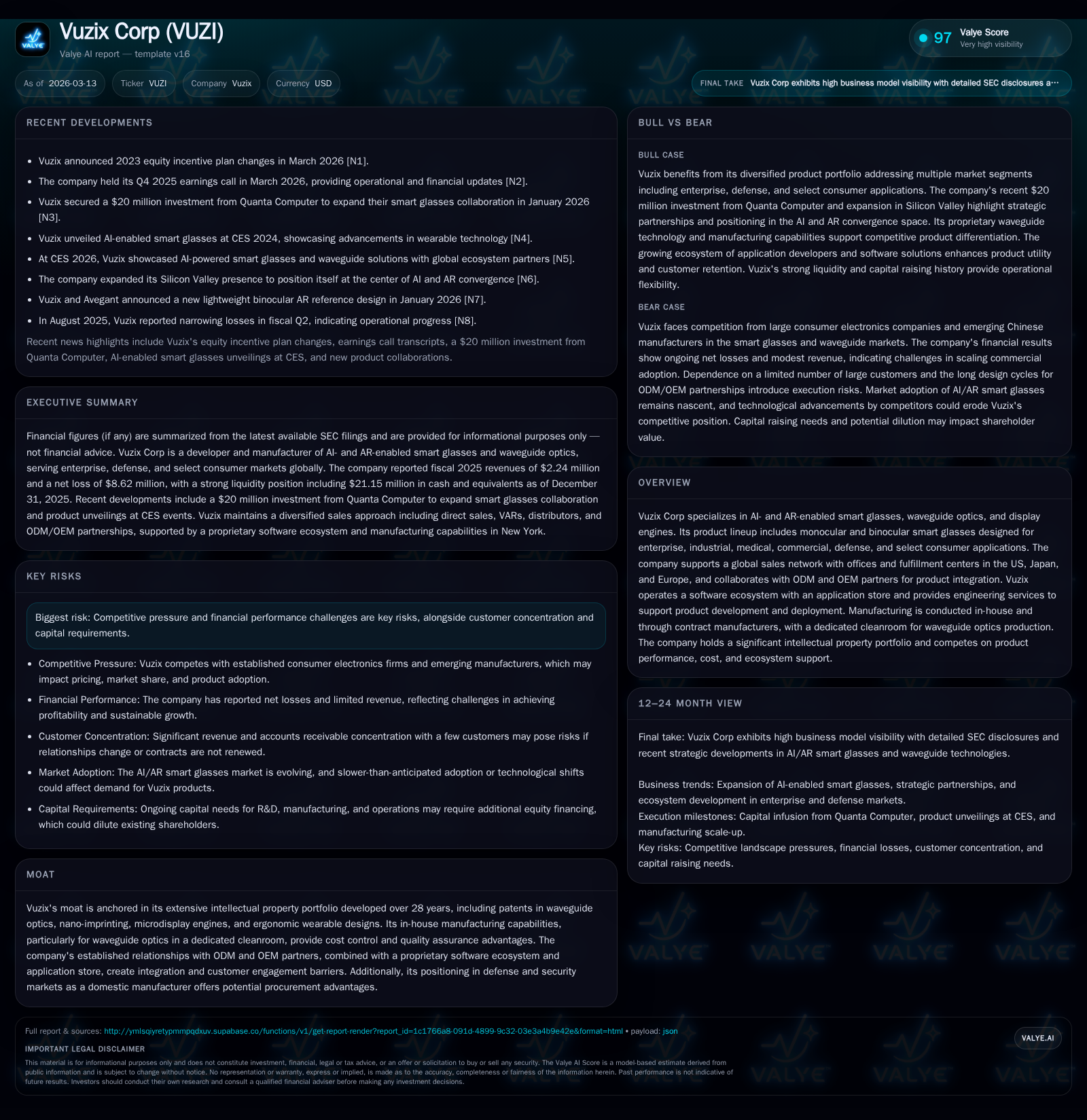

Vuzix Corp demonstrated a robust revenue recovery in 2025, growing top-line by over 76% after a dip in 2024, driven by enterprise and defense demand for its AI- and AR-enabled smart glasses. The company’s competitive edge stems from an extensive IP portfolio and dedicated cleanroom waveguide manufacturing, positioning it well against peers. Despite improving operating losses, Vuzix remains unprofitable with negative return on equity and substantial cash outflows, reflecting investment-intensive scaling of emerging wearable technology. Key risks include customer concentration, competition from established electronics giants, and capital requirements to fund R&D and production capacity expansion. Monitoring product adoption milestones, customer diversification, and cash flow trends will be critical.

Revenue Recovery: Analysis of Vuzix’s Historical Growth Trajectory

Vuzix Corp’s top-line performance over the past four years reveals both volatility and signs of recovery critical to understanding its ongoing commercial development. After peaking at approximately $2.9 million in revenue during fiscal year 2022, the company experienced a pronounced decline through 2023 ($1.07 million) and a modest increase in 2024 ($1.27 million). However, fiscal 2025 saw a strong rebound with revenue surging by 76.3% year-over-year to reach $2.24 million [F1]. This resurgence reflects increased demand across enterprise-focused product lines.

Despite top-line growth momentum, operating income remains under pressure with sizeable losses that shrunk by over half in magnitude from -$74 million in 2024 to -$32.5 million in 2025—improvements driven partly by operational efficiencies but still highlighting underlying profitability challenges. Net income followed a similar improvement trajectory narrowing losses to -$8.6 million [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -9 | -19 | -33 | +76.3% | +36.9% |

| 2024 | 1 | -14 | -24 | -74 | +19.2% | +31.3% |

| 2023 | 1 | -20 | -26 | -52 | -63.2% | -84.8% |

| 2022 | 3 | -11 | -25 | -42 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 470757 | -21 | -34.9 |

| 2024 | 470757 | -25 | -36.6 |

| 2023 | -32 | -24.6 | |

| 2022 | -26 | -9.2 |

Source: SEC companyfacts cache [F1].

Operating cash flows remained negative across the period albeit showing improvement with a lessening outflow of nearly $18.8 million in 2025 versus $23.7 million in the prior year; capital expenditures increased moderately reflecting investments to boost waveguide manufacturing capacity [F1].

Core Drivers Behind Smart Glasses Demand Expansion

Vuzix’s product suite centers on AI- and AR-enabled smart glasses available in monocular and binocular configurations tailored primarily toward enterprise markets such as logistics warehousing, field service operations, healthcare applications including medical imaging support and diagnostics guidance as well as defense-related uses requiring secure domestic manufactured components [N1][S28].

The company’s positioning leverages niche needs within these segments where ruggedness combined with high display clarity and lightweight form factor make significant operational contributions over smartphone or tablet alternatives. Market drivers fueling demand include heightened digital transformation goals within industrial clients seeking hands-free information delivery paired with augmented reality overlays for enhanced worker efficiency.

In defense procurement specifically—where supply chain integrity is paramount—Vuzix benefits from being a domestic manufacturer of critical waveguide optics technology positioning them favorably amid U.S.-centric sourcing policies [N1]. Custom engineering services support integration into mission-critical headsets further adding commercial stickiness.

The Role of Intellectual Property and In-House Manufacturing in Competitive Positioning

A cornerstone of Vuzix’s moat resides in its intellectual property amassed over nearly three decades encompassing sophisticated waveguide optics designs utilizing nano-imprinting patents coupled with proprietary microdisplay engines enabling superior brightness-to-weight ratios important for wearable comfort [S10].

Manufacturing control granted through their dedicated cleanroom facility allows Vuzix cost-effective mass replication while ensuring quality standards difficult for competitors relying solely on external suppliers or licensing models to meet [S12]. Their optics exhibit advantageous features such as minimal forward light glow termed "Incognito technology," providing clearer immersive visuals essential for extended wear scenarios.

This integrated approach combining patented high-performance optics with custom design adaptability for ODM/OEM clients creates barriers that larger consumer electronics firms find challenging to surmount without comparable vertical integration [S10].

Enterprise and Defense Markets: Growth Prospects and Strategic Advantages

Vuzix’s focus on key verticals supported by value-added reseller networks fosters tailored solutions addressing complex requirements from warehousing logistics workflows to healthcare providers deploying smart glasses for telemedicine applications [N1][S28]. Incremental sales traction stems from multi-year client engagements emphasizing software-hardware ecosystems enriched by their hosted application store facilitating developer innovation.

In defense sectors—due to stringent domestic content rules—the company stands strategically advantaged providing bespoke waveguide displays integrated into customized headsets with long development lead times ranging six months to two years typical for military programs [S12]. Such contracts can yield sustained revenue streams once transitioned beyond prototyping phases although timing remains uncertain.

The ongoing expansion into medical technologies provides another lever given the growing acceptance of wearable AR tools assisting surgeons or field medics necessitating device robustness alongside data fidelity provided by Vuzix optical elements.

Financial Performance Under Pressure: Operating Losses Amid Scaling Efforts

Though operating losses have narrowed significantly from mid-70 million levels in 2024 to just above $32 million in fiscal year-end 2025—this still highlights material negative margins inherent within emerging hardware-intensive businesses where upfront R&D costs combined with supply chain investments outpace early-stage revenue inflows [F1][N1].

The operating cash flow deficit improved only modestly reflecting continued working capital consumption consistent with inventory build-up ahead of anticipated order growth plus negative net income influence on non-cash adjustments [F1]. Capital expenditures climbed near $2 million marking strategic spend focused on enhancing volume manufacturing capabilities—a core enabler for scale economics yet dilutive short term.

The roughly negative -35% return on equity calculated from net loss relative to diminished equity base signifies that despite progressive top-line engagement scale internal profitability remains challenged until product margin leverage or product mix shifts materially improve [F1].

Capital Allocation Strategies: Navigating Cash Flows, Buybacks, and Investments

Vuzix allocates capital predominantly toward research & development activities aimed at sustaining technological edge alongside incremental investments expanding facilities for their proprietary waveguide optics production via contracted manufacturers complemented by internal cleanroom expansions [F1][S12][S26].

Equity incentive plan changes disclosed recently hint at efforts to align employee retention amid competitive talent markets within AR engineering sectors [N2]. While share buybacks remain modest (~$470K historically), they reflect constrained discretionary cash flow availability amid ongoing operational deficits rather than aggressive capital returns.

Liquidity management includes proactive capital raises via at-the-market offerings supporting day-to-day operations while balancing curtailment of non-essential expenditures—a standard practice for young tech hardware plays requiring patient capital infusion until sustainable cash generation emerges [S11][S13][S20].[F1]

Key Milestones to Monitor: Product Development, Customer Diversification, and Market Penetration

Key inflection points include validation milestones tied to delivery schedules from ODM/OEM partners negotiating complex design cycles lasting up to two years depending on product complexity impacting backlog visibility [N1][S23]. Notable progress or order size increases would signal broadening adoption beyond concentrated customer groups characteristic today.

Customer concentration remains significant—with few customers representing major proportions of receivables—thus diversification initiatives through expanded VAR networks or targeting new verticals will be crucial to reduce order volatility risk embedded within short-notice discretionary purchase orders constituting majority revenue sources rather than long-term contractual arrangements [S3][S6]. Monitoring gross margin progression especially as volume scales can indicate operational leverage achievement.

Risk Factors: Competitive Intensity, Customer Concentration, and Capital Needs

Substantial risks stem from fierce competition both by entrenched consumer electronics giants entering AR-enabled devices as well as emerging Asian manufacturers ramping similar display technologies potentially pressuring pricing or segment share gains; ecosystem depth around software applications serves as vital differentiation but faces constant threat given rapid innovation cycles in wearables tech space [S10][S16].

Customer dependency is acute given that orders may be reduced or canceled without penalty impairing near-term revenue forecast reliability—compounded by absence of binding purchase commitments leading management planning challenges around inventory levels or operating resource allocations [S23][S3].

Capital market dependence persists as ongoing losses require further financings until self-sustaining operations materialize—a balance hampered if macroeconomic conditions restrict access—or if strategic initiatives delay anticipated margin gains forcing expense cuts impacting growth trajectories.[S11][S20]

Outlook Considerations Based on Recent Earnings Commentary and SEC Filings

Management commentary accompanying the Q4 2025 earnings noted cautious optimism anchored on improving demand trends fueled by strengthened enterprise solutions penetration along with early volume contributions from new waveguide manufacturing outputs targeted at OEM collaborations [N1][S23]. However uncertainties linger given limited order backlog transparency exacerbated by short notice purchasing patterns limiting visibility beyond next quarter.

Investment focus remains fixed on advancing product development pipelines addressing both industrial use cases as well as expanding footprint within defense contracts where domestic manufacturing advantages remain compelling leverage points.[N1]

Close attention should be paid to quarterly revenue run rates signaling sustainable enterprise uptake pace; progress toward reducing operating losses delivering structural expense efficiencies; evolving customer composition metrics indicating successful diversification efforts; alongside cash-burn trends relative to capital market access prospects.

Due diligence concludes this analysis reflects publicly available data up through Q4 fiscal year ending December 31st 2025 without extrapolations or speculative forecasts beyond stated company disclosures and regulatory filings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments