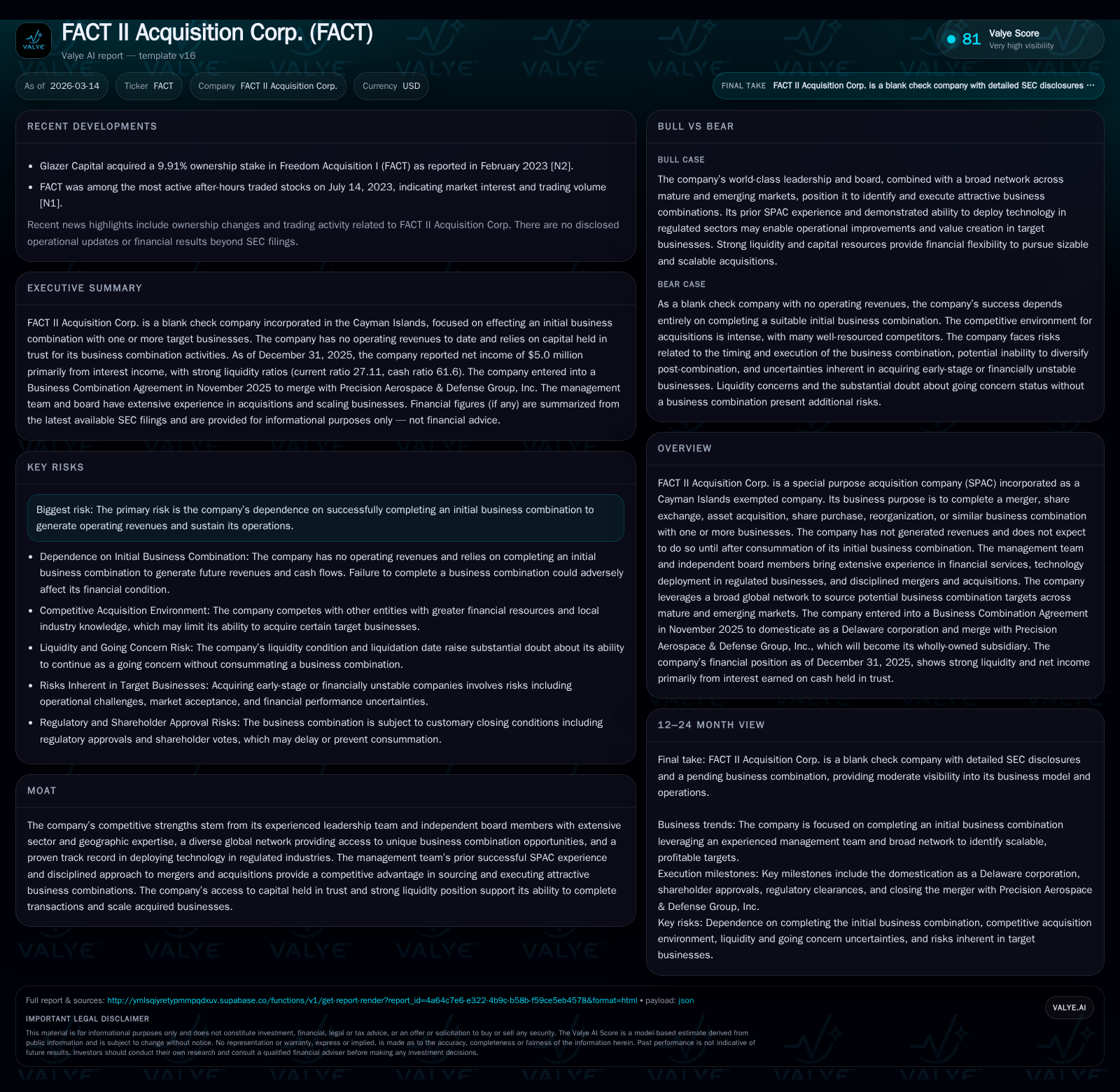

FACT II Acquisition Corp’s Transition to Precision Aerospace & Defense Hinge on Timely Business Combination

SPAC FACT II Acquisition Corp. is positioned for growth through a pending merger but remains reliant on completing its initial business combination.

FACT II Acquisition Corp., a Cayman Islands-based special purpose acquisition company (SPAC), was formed in mid-2024 with the goal of merging or acquiring businesses to generate operating revenues. As of 2025, the company had no operations or revenue, maintaining capital primarily in a trust account. The management team focuses on leveraging extensive financial and operational expertise to identify targets, recently entering an agreement to merge with Precision Aerospace & Defense Group, Inc. Success hinges on completing this business combination by mid-2026 to avoid liquidation. Financial results reflect typical pre-combination SPAC attributes: negative operating income, negative cash flow from operations, but positive net income due to accounting recognition of warrant-related items.

Background and Corporate Structure

FACT II Acquisition Corp. was established as a Cayman Islands exempted company on June 19, 2024 as a special purpose acquisition company (SPAC) focused on completing an initial business combination that will generate operating revenues [S1][S5]. The company’s strategy concentrates on leveraging capital combined with the extensive experience of its leadership team—which has deep expertise in financial services, regulated technology deployment, and complex global operations—to identify attractive targets across mature and emerging markets [S5][S19].

The SPAC raised net proceeds of approximately $175 million through an initial public offering (IPO) and associated private placements conducted simultaneously in late November 2024. These funds have been held primarily in a trust account invested mainly in U.S. government securities or cash equivalents per regulatory requirements until the consummation of its business combination or liquidation if not completed within prescribed time limits [S3][S6][S12][S13].

Historical Financial Performance

As typical for SPACs pre-business combination, FACT II has no operating revenues since inception. Its financial results principally reflect costs associated with general administrative expenses related to formation, IPO activities, advisory fees, and legal services.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 5 | -903130 | -2 | +7079.4% |

| 2024 | 0 | -305103 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -58.9 |

| 2024 | 1.1 |

Source: SEC companyfacts cache [F1].

Operating income declined by over 100% year-over-year reflecting increased costs ahead of the planned merger [F1]. The notable swing to positive net income in 2025 is attributable primarily to non-cash gains such as remeasurement of warrant liabilities rather than core operations [F1][S10]. Cash used in operations increased roughly threefold as the company prepared for its upcoming combination while maintaining minimal capital expenditures typical for companies without active operations [F1].

Capital Structure and Liquidity

The company’s capital structure comprises Class A Ordinary Shares issued publicly (subject to redemption rights priced around $10 per share held in trust), founder shares held by Sponsor HoldCo with lock-ups post-combination, and private placement units. No debt was outstanding at fiscal year-end though provisions exist for potential loans from Sponsor HoldCo or affiliates up to $2 million convertible into equity at $10 per share upon consummation of the initial business combination [S4][S8][S11].

Cash declined from $1.45 million at December 31, 2024 to approximately $544 thousand at year-end 2025 as operational expenditures continued prior to closing any transaction [F1][S10]. However, the Trust Account balance increased modestly reflecting investment returns at year-end: $183.7 million versus $176.6 million previously [S3]. This reinforces strong liquidity essentially collateralizing public shareholders’ redemption rights.

Nasdaq listing requirements ensure a majority independent board with three independent directors identified providing oversight over management conflicts inherent in SPAC structures where sponsor interests may conflict with public shareholders’ interests regarding deal selection and timing [S1][S14].

Initial Business Combination Outlook

In November 2025 FACT II Acquisition Corp.'s management entered into a definitive Business Combination Agreement with Precision Aerospace & Defense Group Inc. (PAD), an aerospace defense sector entity incorporated as a Florida corporation [S16]. The agreement anticipates the domestication of FACT II as a Delaware corporation concurrent with the merger completion.

The merger is projected to commence operations generating revenue streams aligned with PAD’s aerospace capabilities once completed successfully. The management emphasizes selecting businesses demonstrating scalable operations, favorable sector tailwinds such as aerospace defense amid steady government spending, substantive growth potential both organically and via M&A opportunities plus disciplined cost control resulting in positive free cash flow down the line [S19][S22].

This proposed transaction comes against pressing timing constraints — the SPAC must effectuate the combination by May 27, 2026 (with possible short extension under defined conditions) or face mandatory liquidation distributing trust account proceeds pro rata to holders of redeemable shares effectively ending prospects for ongoing operations or upside appreciation [S25]. This deadline imposes material execution risk.

Return Profile and Capital Allocation Plan

Until closing the initial business combination FACT II Acquisition Corp does not operate an enterprise generating recurring cash flows or profits; hence return metrics such as ROE are limited by accumulated deficits and accounting treatments [F1]. The year-end equity reported was negative at approximately -$8.52 million due mainly to accumulated deficits from operating expenses exceeding non-operational gains alongside treatment of redeemable shares classified outside permanent equity [F1][S20].

No dividends or share repurchases have been declared or made given the absence of operating cash flow and because fund deployment strategies focus on closing the combination transaction first [S7][S12][S13][S18]. Post-merger capital allocation policies will depend heavily on PAD’s operational cash flows and growth trajectory.

Competitive Advantages and Risks

FACT II Acquisition Corp asserts competitive strengths rooted mostly in its senior leadership's track record executing prior SPAC transactions successfully combined with broad networks accessing unique deal flow globally especially targeting regulated sectors where technological innovation creates opportunities for operational improvements [S19]. This positioning suggests some differentiation relative to other blank check companies competing intensely for attractive targets.

Risks are primarily execution-oriented: inability to close the PAD transaction on time risks mandated liquidation limiting shareholder recuperation predominantly anchored around trust assets available for redemption [S24]. Conflicts of interest inherent in SPAC governance structures between sponsors holding founder shares with waived redemption rights versus public shareholders who may redeem add complexity requiring trustee oversight and regulatory compliance measures documented extensively by management [S1]. Moreover,a concentration risk exists given dependence upon a single combination target chosen from potentially numerous alternatives.

Monitoring Points Ahead

- Progress updates regarding satisfaction of closing conditions under the Business Combination Agreement including regulatory approvals, legal clearances, and shareholder communications.

- Volume and nature of shareholder redemptions exercised either via tender offer or vote-mediated processes impacting net proceeds available post-merger.

- Any amendments/extensions filed relating to timing constraints approaching May/June 2026 deadline.

- Details about integration plans for Precision Aerospace & Defense including management retention schemes outlined during proxy disclosures.

- Post-merger financial policy around dividends/buybacks grounded fundamentally on PAD operational earnings generation profile once standalone status concludes.

Summary

FACT II Acquisition Corp operates at typical early-stage SPAC profile characterized by zero revenues pre-combination but bolstered by robust sponsor capital commitments secured within a trust account framework protecting public investors’ principal amounts when combined with favorable governance practices. Its leadership’s previous transaction experience affords potential competitive advantage sourcing deals like Precision Aerospace & Defense Group seek tangible growth prospects via strategic combinations targeted toward scaleable aerospace defense markets showing generally resilient demand patterns despite cyclical macroeconomic conditions.

However,the tight timeline imposed by mandatory liquidation deadline remains an acute constraining factor potentially truncating upside if deal execution delays occur while ongoing administrative expense burn despite positive accounting net income reduces net equity further creating pressure points ahead.

Investors should closely watch milestones tied directly both economically and procedurally around completion of business combination efforts signaling transition from SPAC vehicle status toward an operating company generating actual sustainable free cash flows.

This report is prepared solely for informational purposes reflecting reported facts as per regulatory filings without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments