Stagwell Inc’s Growth Through Digital Integration Faces Leverage and Market Risks

A global marketing services firm leveraging AI and digital platforms to disrupt legacy models while managing significant debt exposure.

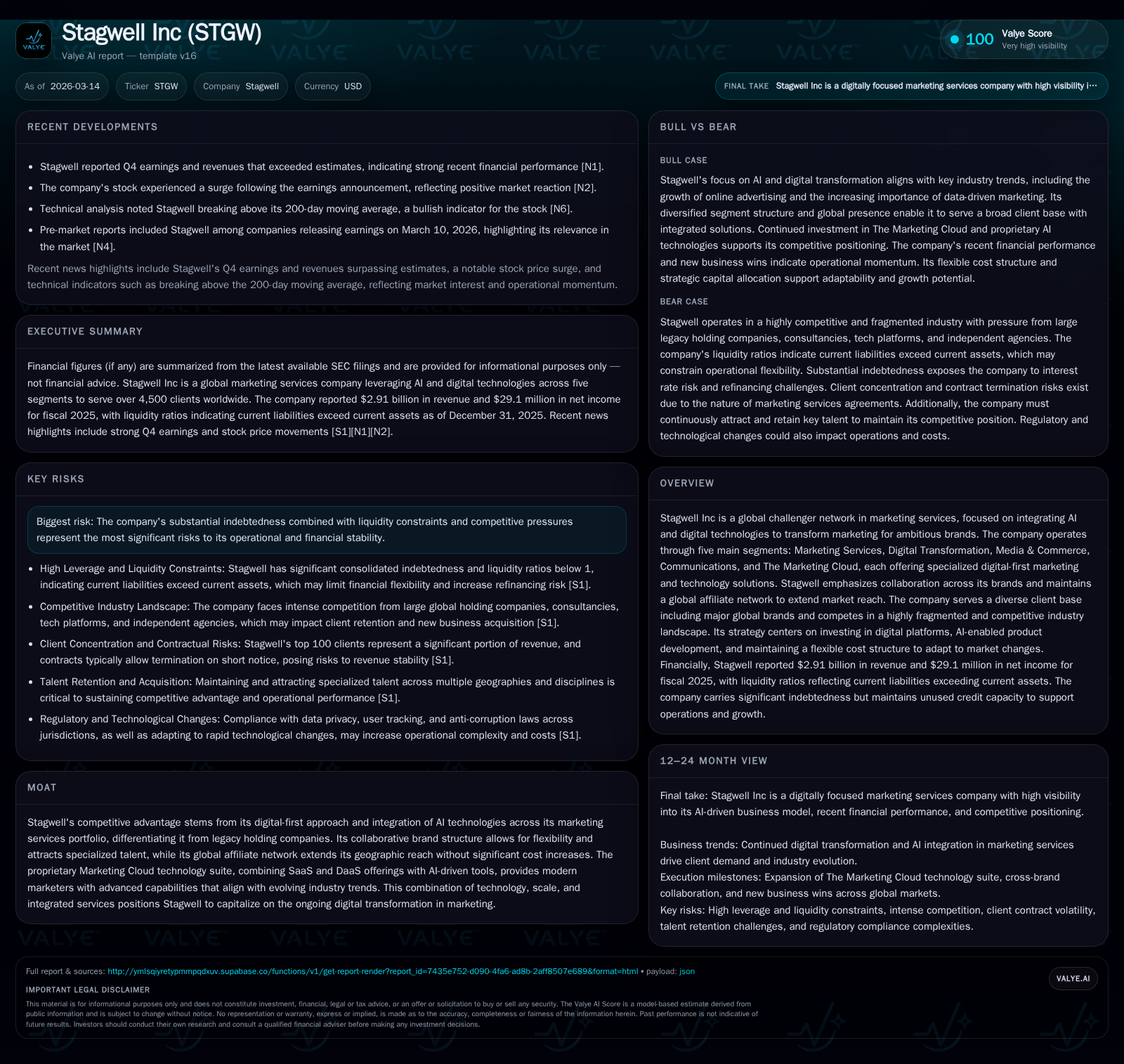

Stagwell Inc has evolved into a formidable challenger in the marketing services industry by emphasizing digital-first strategies and AI-driven product innovation. The company reported $2.91 billion in revenue for 2025, growing modestly amid ongoing investments in its Marketing Cloud and global Brand network. While profitable on an operating basis with expanding cash flows, Stagwell’s net income remains slim relative to leverage constraints. Future growth hinges on scaling proprietary technologies, expanding global client engagement, and navigating a competitive landscape marked by rapid technological change and regulatory complexity. Financially, capital allocation favors targeted acquisitions and share repurchases, but liquidity management remains critical due to substantial indebtedness and exposure to economic cycles.

Historical Performance and Growth Drivers

Stagwell Inc reported total revenues of $2.91 billion for fiscal year 2025 [F1]. This represented a modest increase of approximately 2.4% compared to 2024's $2.84 billion revenue base, continuing a steady upward trajectory over the past four years as the company expanded beyond legacy marketing services into digital transformation initiatives [F1][S1]. Operating income improved materially by 19.5% from $133 million in 2024 to $159 million in 2025, highlighting enhanced operational efficiency amidst rising revenues [F1]. Net income saw a marked rebound, rising from roughly $2.3 million in 2024 to $29.1 million in 2025—an over elevenfold increase—reflecting improved profitability despite investment activity [F1].

Operating cash flow more than doubled year-over-year to $291 million while capital expenditures increased significantly to $43.7 million from $18.9 million the prior year [F1], evidencing aggressive reinvestment into proprietary technology platforms such as The Marketing Cloud—a suite of AI-enabled SaaS and DaaS products aimed at transforming marketing operations [S12][S18]. Throughout this period, Stagwell has pursued a blend of organic growth coupled with accretive acquisitions enhancing scale across its five reporting segments: Marketing Services, Digital Transformation, Media & Commerce, Communications, and The Marketing Cloud [S7][S12].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.9 | 29 | 291 | 159 | +2.4% | +1188.2% |

| 2024 | 2.8 | 2 | 143 | 133 | +333.8% | +75.7% |

| 2023 | 0.7 | 1 | 81 | 91 | -75.6% | -95.3% |

| 2022 | 2.7 | 27 | 348 | 159 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 134 | 247 | 3.8 |

| 2024 | 108 | 124 | 0.7 |

| 2023 | 224 | 67 | 0.4 |

| 2022 | 19 | 325 | 5.7 |

Source: SEC companyfacts cache [F1].

*Revenue reported smaller for FY2023 likely due to differences in consolidation or business scope [F1].

Business Model and Industry Positioning

Born digital and structured as a global challenger network led by entrepreneurial agency brands across more than 34 countries [S7], Stagwell’s competitive advantage rests in its ability to harmonize creative expertise with cutting-edge technology including AI-led marketing automation and analytics tools embedded within The Marketing Cloud [S7][S12]. This tech-centric approach differentiates it from traditional advertising holding companies which often rely more heavily on legacy full-service agencies.

The company's integrated model spans:

- Marketing Services: Focused on creative development supported by consumer insights via AI-powered analytics.

- Digital Transformation: Delivering digital architectures including platforms enhanced with AI-native strategies for clients’ evolving customer engagement needs.

- Media & Commerce: Utilizing advanced data analytics for media planning across emerging channels including connected TV and retail media networks.

- Communications: Offering public relations plus advocacy services leveraging AI-driven targeting.

- The Marketing Cloud: Proprietary software tools combining SaaS/DaaS solutions enabling real-time market research via generative AI surveys plus communication tech aggregating extensive data sources for actionable insights [S7][S12][S18].

This segmentation is designed to cover the entire marketing value chain addressing sophisticated demands from blue-chip clients such as Google, Amazon, Nike, Apple among over 4,500 global customers [S17]. Stagwell’s emphasis on collaboration rather than brand consolidation acts as a magnet for niche talent while facilitating bespoke multi-disciplinary campaigns that span geographies seamlessly [S14].

Future Growth Prospects

Looking forward, key growth drivers include expanding adoption of The Marketing Cloud products which represent scalable digital revenue streams aligned with industry migration toward SaaS-driven marketing efficiency tools [N1][S12]. The continued shift toward addressable digital media platforms presents opportunities particularly through augmented reality (AR), quick response (QR) codes for consumer engagement tracking within commerce ecosystems [S19][S26]. Furthermore, investments in cross-brand integration aim to capture large multi-region mandates that deliver premium contract value exceeding $10 million annually per deal [S7].

Risks constraining growth are macroeconomic sensitivities—advertising budgets being discretionary items vulnerable during inflationary or recessionary environments—as well as intensifying competition from other holding companies like WPP or Publicis Groupe alongside tech platform entrants delivering marketing-as-a-service offerings directly [S10][N8][N9]. Regulatory headwinds related to data privacy laws globally plus emerging compliance obligations under the EU’s Artificial Intelligence Act create added operational complexity requiring ongoing governance investment [S24][S11]. High client concentration implies particular account losses can disproportionately harm revenues since top ten clients constituted about 18% of total revenue in 2025 [S20].

Financial Forecasts and Key Milestones to Monitor

Stagwell has not provided public multi-year guidance but flagged priorities toward increasing organic top-line growth above low-single digits annually by accelerating digital revenue mix expansion through The Marketing Cloud investments [N1][S27]. Milestones worth monitoring include:

- Quarterly revenue growth acceleration driven by new SaaS product launches.

- Expansion into new geographic markets via Global Affiliate Network adding regional capabilities without high fixed costs.

- Progress in cross-brand collaboration resulting in larger integrated contract wins.

- Improvements in margin profiles through operating leverage despite rising input costs.

- Reduction of leverage ratios following sustained free cash flow generation amid selective acquisition activity.

Analysts should also watch incremental details about product adoption rates of AI-powered research instruments within The Marketing Cloud as a bellwether for deepening customer entrenchment.

Capital Allocation and Financial Returns

Despite improvements in profitability metrics during FY2025 [F1], Stagwell’s return on equity remains modest at approximately 3.8%, reflecting the capital-intensive nature of its buy-and-build strategy combined with elevated debt levels that impinge net earnings retention capacity [F1][S6]. Operating cash flow grew robustly by over 100% year-over-year reaching nearly $291 million in absolute terms—the highest recorded—with capital expenditures ramping up accordingly as part of strategic platform development efforts [F1][S5]. Free cash flow after capex stood near $247 million for the same period.

The company actively manages shareholder dilution through consistent share repurchases totaling roughly $134 million in FY2025 alongside funding significant acquisitions aimed at expanding expertise or geographic reach [F1][S17]. Dividend payouts historically have been negligible or non-existent post-SPAC merger era focusing instead on reinvestment into growth verticals.

Leverage remains the central challenge whereby floating-rate debt exposes Stagwell to interest cost variability amid prevailing inflationary monetary policy environments complicating net income predictability [S6][S16]. Management acknowledges ongoing efforts to prudently reduce debt where possible without compromising opportunistic investments targeted at sustainable margin expansion [N1][S6].

Risks Summary

Key operational risks stem from:

- Cyclicality: Client spend reduction during economic downturns could shorten contract duration or decrease project scale leading to volatility [S1][S20].

- Competition: Battles for large multi-national mandates against entrenched legacy groups as well as nimble independent agencies able to poach talent or pricing power erosion through discounting tactics.[S10]

- Regulatory: Compliance requirements surrounding privacy laws (e.g., GDPR), AI regulation enforcement impacting certain cloud offerings causing potential redesign or costly litigation risks around IP rights associated with AI use.[S11][S21]

- Credit Risk: Substantial indebtedness raises refinancing risk compounded by floating interest expense exposure affecting liquidity/capacity especially if credit ratings deteriorate further.[S6]

- Client Concentration: Loss or downsizing of any top-tier client could materially impact results given reliance on major accounts contributing nearly one-fifth of revenue.[S20]

Conclusion

Stagwell Inc stands out in the increasingly complex marketing ecosystem by combining entrepreneurial agency brands united under an innovative technology-driven platform emphasizing Artificial Intelligence integration. It has demonstrated disciplined growth yielding stronger operational profitability supported by significant free cash flow generation allowing measured capital returns through buybacks while simultaneously investing heavily into scalable digital platforms characteristic of next-gen marketing solutions.

However,the business operates within a highly fragmented competitive environment marked by rapid technological change complemented by challenging macroeconomic headwinds creating revenue cyclicality risk; compounded further by elevated debt burdens constraining financial flexibility. Close attention should be paid going forward to execution progress on The Marketing Cloud innovations alongside prudent liquidity management ensuring resilience amid industry transformations.

Disclaimer: This report is for informational purposes only; it does not constitute investment advice or an offer to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments