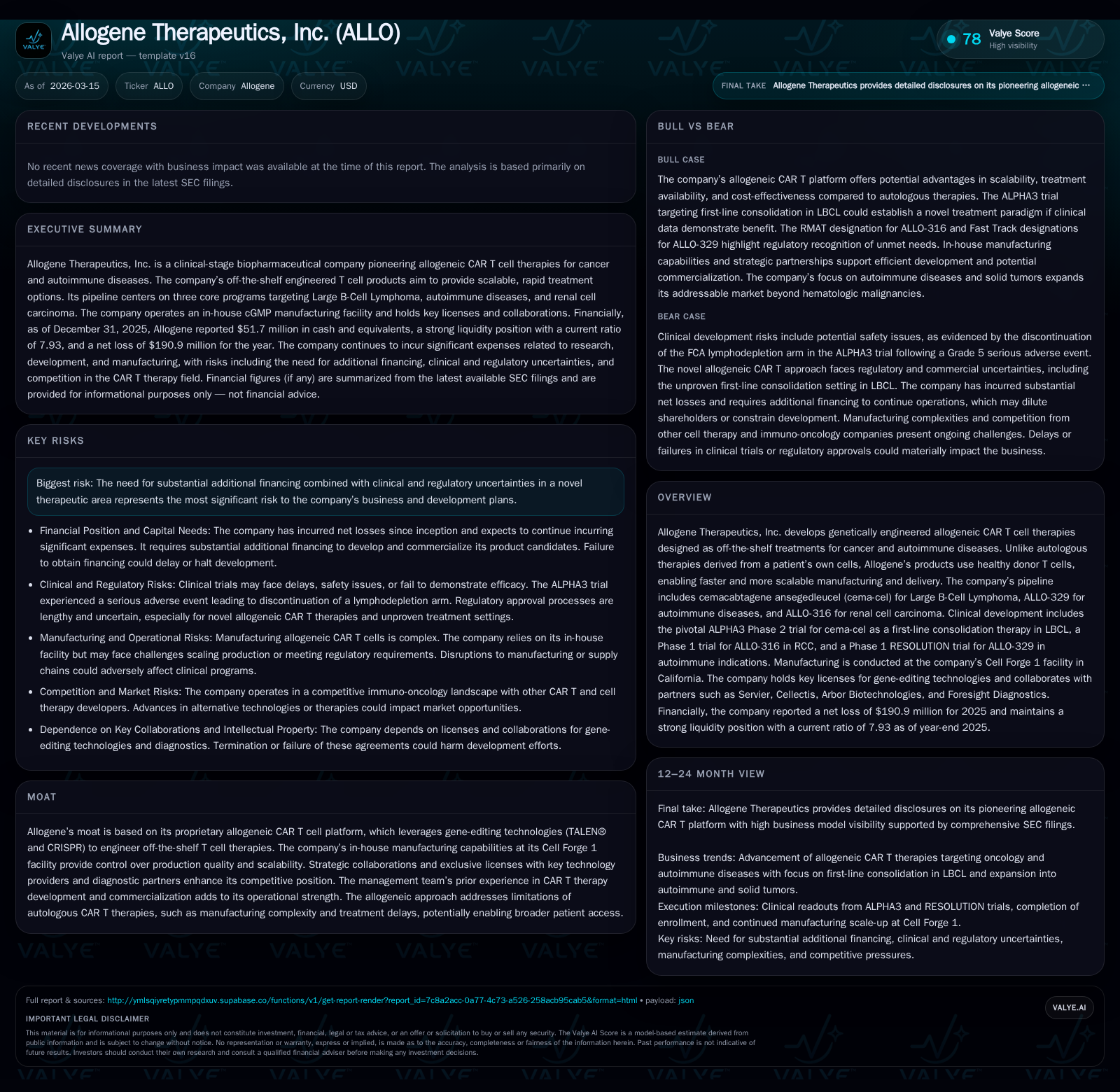

Allogene Therapeutics Charts Progress and Challenges in Allogeneic CAR T Development

Allogene Therapeutics is pioneering off-the-shelf allogeneic CAR T therapies while continuing to manage significant operational losses and regulatory complexities.

Allogene Therapeutics advances its proprietary allogeneic CAR T platform targeting oncology and autoimmune diseases, with pivotal readouts expected in Q2 2026. The ALPHA3 Phase 2 trial for cema-cel in first-line large B-cell lymphoma represents a potential inflection point, while other pipeline candidates explore autoimmune and solid tumor indications. The company remains in a developmental stage with ongoing net losses but improving financial metrics, supported by its in-house Cell Forge 1 manufacturing facility. Investors should monitor clinical safety signals, regulatory developments, and capital allocation as the company approaches key milestones.

Historic Financial Performance and Improvement Trends

Allogene Therapeutics has consistently reported net losses throughout its development stage but shows steady improvement over recent years. Operating income losses decreased from approximately -$335.5 million in FY2022 to -$209.3 million in FY2025—a 23.4% year-over-year improvement as of the latest fiscal year [F1]. This suggests enhanced operational efficiency amid continued investment in research and manufacturing scale-up.

Net income losses narrowed from -$340.4 million in FY2022 to -$190.9 million in FY2025, a 25.9% improvement reflecting better cost management against elevated expenses [F1]. Operating cash flow improved from -$220.5 million in FY2022 to -$149.2 million in FY2025, a 25.5% year-over-year enhancement [F1]. Capital expenditures declined notably from $5.19 million in FY2022 to $386 thousand in FY2025 (-44.4%), indicating a maturing manufacturing capex cycle [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -191 | -149 | -209 | 0 | +25.9% |

| 2024 | -258 | -200 | -273 | 1 | +21.3% |

| 2023 | -327 | -238 | -328 | 2 | +3.9% |

| 2022 | -340 | -221 | -336 | 5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -150 | -65.3 |

| 2024 | -201 | -61.0 |

| 2023 | -239 | -63.9 |

| 2022 | -226 | -51.0 |

Source: SEC companyfacts cache [F1].

Table: Allogene's financial performance shows steady narrowing of operating losses alongside improvements in cash flow though free cash flow remains negative.

Innovative Platform and Clinical Development Progression

Allogene’s proprietary allogeneic CAR T platform uses gene-edited healthy donor T cells rather than patient-derived cells, enabling "off-the-shelf" therapies with immediate availability without multi-week manufacturing delays typical of autologous products [S1]. TALEN® and CRISPR gene editing technologies underpin this approach.

This platform aims to address limitations of autologous CAR T therapies such as variable product consistency and treatment delays that can adversely affect patient outcomes. Leadership experience from Kite Pharma supports advancement of this novel immuno-oncology modality.

Clinical efforts focus on optimizing lymphodepletion regimens critical for CAR T expansion and persistence post-infusion; notably exploring reduced-intensity or chemotherapy-free conditioning relevant especially for autoimmune indications [S1][N1]. The ALPHA3 Phase 2 trial evaluates cemacabtagene ansegedleucel (cema-cel) as first-line consolidation therapy in large B-cell lymphoma (LBCL), representing an untested regulatory pathway with inherent risks [S1][S4].

Pipeline Programs: Leading Candidates and Trial Implications

Key candidates include:

cemacabtagene ansegedleucel (cema-cel): Under evaluation in the ALPHA3 trial for first-line consolidation treatment of LBCL post-chemotherapy [S1]. This represents a novel indication with no currently approved CAR T therapies worldwide for this use case [S4].

ALLO-329: A next-generation CD19 Dagger® program targeting autoimmune diseases that aims to improve scalability through less toxic lymphodepletion protocols potentially eliminating chemotherapy agents [S1][N1].

ALLO-316: Investigated under the TRAVERSE Phase 1 study for renal cell carcinoma solid tumors where durable CAR T expansion/persistence remains challenging [S1][N1].

Safety monitoring remains critical given serious adverse events (SAEs). The discontinuation of the fludarabine, cyclophosphamide, ALLO-647 (FCA) arm after a Grade 5 SAE highlights developmental risks inherent to these novel therapies [S26][N3]. Patient enrollment challenges also pose risks amid competitive oncology trial landscapes.

Endpoints emphasize clinical response rates alongside biomarkers indicating CAR T persistence—a key factor for long-term durability especially relevant for solid tumor indications like ALLO-316.

Manufacturing Capacity and Strategic Importance

Allogene's Cell Forge 1 facility in California operates under cGMP standards and is pivotal to its manufacturing strategy ensuring quality control essential for live cell therapy production [S1].

Vertical integration enables rapid scale-up necessary for off-the-shelf inventory buildout to serve broad patient populations without reliance on external manufacturers or autologous supply chains.

Gene-editing licenses provide exclusive access to TALEN® technology through Cellectis; however, related licensing disputes between Cellectis and Servier introduce potential legal uncertainties that could indirectly impact Allogene's operations [S16][S26].

Regulatory approval requires demonstrating both product efficacy and consistent manufacturing quality—a notable challenge unique to living drug products compared to traditional pharmaceuticals [S25]. Manufacturing readiness thus constitutes a strategic barrier reducing competitor encroachment.

Capital Structure, Cash Flow Dynamics, and Returns

Despite improved financials, Allogene continues as a developmental-stage biotech with significant operating losses totaling nearly $210 million in FY2025 alone [F1]. Net losses were approximately $191 million with operating cash flow negative $149 million net of minimal capex—indicating ongoing substantial cash burn.[F1]

Liquidity includes $51.7 million cash & equivalents against $32.5 million current liabilities yielding a healthy current ratio near 7.93x providing runway amidst market uncertainties [F1]. Equity declined from about $667 million at end-FY2022 to roughly $293 million at end-FY2025 reflecting dilution from financing activities [F1].

No dividends or share repurchases are planned; return on equity approximates negative 65%, consistent with pre-commercial biotechs investing heavily without revenue-generating products.[F1]

SEC disclosures underscore the need for additional financing or partnerships to support ongoing development beyond existing cash reserves amid reimbursement challenges affecting commercial prospects.[S2][S10][S18]

Near-Term Catalysts and Monitoring Points

Upcoming pivotal data readouts expected Q2 2026 from the ALPHA3 trial will be critical inflection points potentially validating off-the-shelf CAR T therapy as frontline LBCL consolidation treatment or highlighting operational risks tied to safety concerns [N1][S1][N3].

Post-readout regulatory interactions will be closely watched especially regarding safety management plans following FCA arm discontinuations and any emerging adverse event profiles affecting benefit-risk assessments.[S4]

Enrollment pace amid competitive oncology trials may influence timelines; delays could impact operational execution.[S2]

Capital raise plans or strategic collaborations extending runway will affect financial stability perceptions alongside progress toward commercialization leveraging Cell Forge capacity.[N3][S10]

Intellectual property developments related to Cellectis-Servier licensing disputes remain mid-term risks influencing exclusivity or royalty obligations potentially complicating commercial rollout.[S16][S26]

In summary, Allogene demonstrates scientific innovation paired with improving financial discipline but remains dependent on successful clinical validation before commercialization prospects can be realized sustainably.

Disclaimer: This analysis synthesizes publicly available SEC filings ([F1], [S#]) and verified news reports ([N#]). It does not constitute investment advice or stock performance prediction but aims to inform on Allogene Therapeutics’ business fundamentals as of March 15, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments