Opus Genetics Charts Course in Gene Therapies for Inherited Retinal Diseases

Opus Genetics pursues advanced AAV-based gene therapy programs addressing rare inherited retinal diseases, balancing scientific innovation with financial and regulatory challenges.

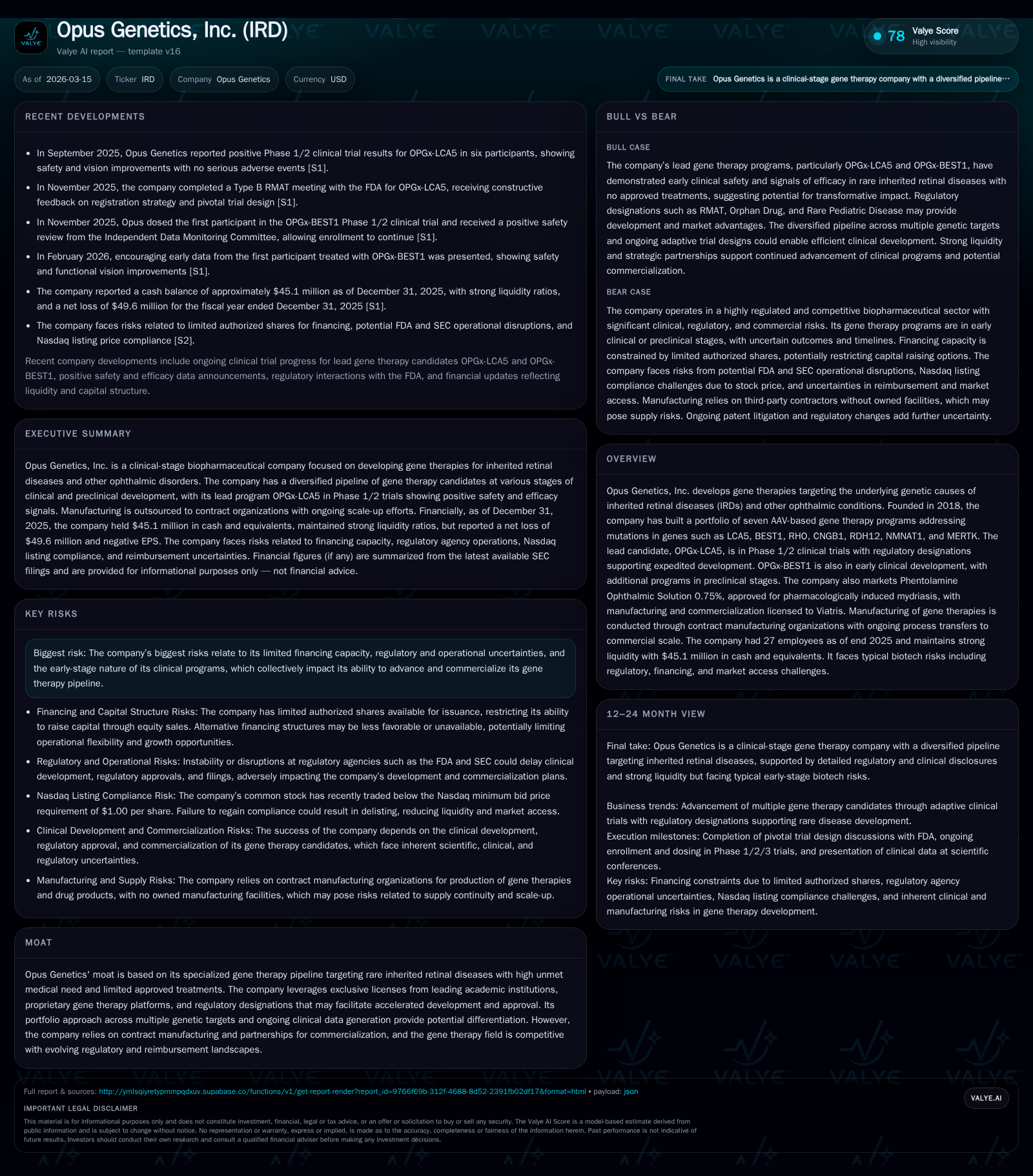

Founded in 2018 and evolving through strategic mergers, Opus Genetics focuses on developing gene therapies for inherited retinal diseases (IRDs) with a specialized portfolio of seven AAV-based programs. Financially, the company bears significant operating losses driven by pipeline progression but maintains robust liquidity with a current ratio above 6. Its lead candidate, OPGx-LCA5, benefits from expedited regulatory pathways while facing the inherent developmental risks typical of early-stage biotech. Limited equity financing capacity and ongoing patent litigation underscore notable operational risks. Observers should monitor clinical milestones, regulatory developments, and manufacturing scale-up as indicators of future progress.

Genesis and Growth: Evolution of Opus Genetics’ Focus Since Inception

Established in early 2018 as Ocuphire Pharma, Inc., the company originally pursued ophthalmic small-molecule therapies. Key corporate events reshaped its trajectory significantly: the April 2018 merger with Ocularis Pharma provided initial assets including Phentolamine Ophthalmic Solution; the reverse merger into Rexahn Pharmaceuticals (November 2020) offered public market access accompanied by a $21 million equity raise [S1]. The defining shift occurred on October 22, 2024, when Ocuphire acquired Private Opus Genetics Inc., integrating a deep pipeline of gene therapies targeting inherited retinal diseases (IRDs), thereby pivoting fully toward gene therapy specialization [S1]. This transition brought seven adeno-associated virus (AAV)-based gene therapy candidates targeting discrete genetic mutations underpinning IRDs.

Despite this strategic expansion, the company has yet to generate product revenues consistent with its clinical-stage status; top-line figures remain at zero throughout the last reported fiscal years [F1]. Growth thus largely reflects pipeline development and capital markets activity rather than commercial sales.

Financial Trajectory: Analyzing Operating and Cash Flow Trends through 2025

Opus Genetics has experienced growing operating losses concomitant with escalating research and development investments fundamental to advancing multiple clinical programs. Operating income deteriorated from -$10.6 million in FY2023 to -$62.1 million in FY2024 before moderating slightly to -$38.6 million in FY2025 [F1]. Similarly, net income turned deeply negative over this span: from approximately -$9.9 million in FY2023 to -$57.5 million in FY2024 and then to -$49.6 million in FY2025 [F1]. The steep rise in losses through 2024 corresponds with pipeline scale-up efforts post-acquisition; a partial easing in 2025 possibly reflects operational adjustments or timing effects.

Operating cash flow underscores similar stress points — positive $14.3 million in FY2022 reversed sharply to negative trends thereafter (-$1.1 million in 2023; -$25.6 million in 2024; -$35.3 million in 2025) [F1]. While free cash flow (CFO less capex) is not explicitly reported, the steep negative CFO strongly suggests sustained cash burn aligned with costly clinical advancement.

Liquidity remains robust due to conservative balance sheet management: at December 31, 2025, cash and equivalents stood at $45.1 million against current liabilities of $7.8 million yielding a high current ratio of approximately 6.43 [F1]. Such buffer provides runway though continued reliance on external financing appears inevitable.

Equity shrank noticeably from $49.9 million end-2023 down to $15.3 million by end-2025 demonstrating capital depletion against losses [F1]. The calculated approximate return on equity stands deeply negative at about -323%, indicative of unprofitable investment phases [F1]. There are no recent dividends or share repurchase activities reported—consistent with growth-phase strategies prioritizing internal capital use [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -50 | -35 | -39 | +13.8% |

| 2024 | -58 | -26 | -62 | -476.1% |

| 2023 | -10 | -1 | -11 | -155.8% |

| 2022 | 18 | 14 | 18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -323.1 |

| 2024 | -855.6 |

| 2023 | -20.0 |

| 2022 | 38.7 |

Source: SEC companyfacts cache [F1].

Table shows operating income (OpInc), net income (Net), operating cash flow (CFO), current ratio, and year-over-year percentage changes where calculable from SEC filings [F1].

Driving Innovation: Detailed Review of Opus Genetics’ Gene Therapy Pipeline

At its core, Opus Genetics operates within the specialized domain of one-time durable gene therapies for severe inherited retinal disorders—conditions characterized by mutations affecting photoreceptor function leading to progressive vision loss often manifesting early in life [S1]. The company's portfolio encompasses seven adeno-associated virus (AAV)-based candidates engineered primarily using vector technologies pioneered at the University of Pennsylvania laboratories known for foundational contributions to ocular gene therapy science.

The lead asset, OPGx-LCA5, targets Leber congenital amaurosis associated with LCA5 mutations and has advanced into Phase 1/2 clinical studies supported by orphan drug designation and other expedited regulatory pathways designed to facilitate faster review cycles [S1]. Another program targeting BEST1-related bestrophinopathy underpins early clinical efforts.

Additional preclinical assets address diverse genotypes including RHO-associated retinitis pigmentosa, CNGB1 mutation forms, RDH12 deficiency, NMNAT1-related disease manifestations, and MERTK-linked degeneration syndromes [S1]. The heterogeneity of targets underscores a platform strategy addressing genetically distinct subsets within IRDs.

Beyond gene therapies, Opus markets Phentolamine Ophthalmic Solution 0.75%, an FDA-approved pharmacological aid for induced mydriasis marketed under license allowing Viatris commercialization rights [S1]. Manufacturing functions for gene therapies rely entirely on contract manufacturing organizations (CMOs) with ongoing process transfers aiming for commercial-scale readiness—a common practice given complexity and cost of GMP-compliant viral vector production workflows.

Regulatory Landscape and Developmental Hurdles Impacting Progress

The company's advancement depends critically on navigating an increasingly complex regulatory environment both domestically at the FDA and internationally through bodies such as EMA [S14], which enforce stringent guidelines related to preclinical validation, investigational new drug applications (INDs), clinical trial conduct adhering to good clinical practices (GCP), manufacturing oversight under cGMP standards, and eventual marketing authorization submissions [S16].

Operational vulnerabilities stem from federal government funding instability affecting agency capacity for timely review—budget cuts or shutdowns can delay IND approvals or new drug applications hurting pipeline timelines [S2]. Regulatory reforms targeting pharmaceutical pricing transparency and reimbursement models introduce further uncertainty regarding commercial viability post-approval amid evolving U.S. healthcare policy debates impacting Medicare Part D coverage rules and Medicaid Drug Rebate Programs [S8][S9][S12][S22].

Compliance obligations extend into anti-kickback laws (AKS), False Claims Act provisions enforcing accurate government billing practices, HIPAA data security mandates, promotional restrictions limiting off-label marketing risk exposure—all mapped into corporate risk frameworks governed actively by senior management teams reporting periodically to audit committees [S4][S5][S6][S7][S9].

Capital Resources, Shareholder Returns, and Financing Constraints

From a capital structure perspective, Opus confronts meaningful constraints rooted chiefly in its authorized shares limit capped around 125 million common shares issued plus reserved per latest reports preventing facile equity equity raises without shareholder approval or charter amendments [S2]. Approximately 69 million shares have been issued with ~54 million reserved for options/warrants limiting headroom for dilution-free funding upon increased R&D demands [S2].

The absence of dividends or stock repurchases aligns with standard biotech growth-phase profiles where reinvestment into pipeline supersedes cash returns; however, persistent negative free cash flow driven by clinical expenditures necessitates disciplined capital stewardship.

Governance extends beyond finance into operational integrity with cybersecurity risk management program overseen jointly by COO and VP Accounting ensuring IT threats are mitigated under external consultant advisories feeding risk reviews directly into Audit Committee updates—a noteworthy linkage accentuating comprehensive risk governance amid sensitive data environments typical for clinical biopharma firms [S1].

Litigation and Intellectual Property: Risks Around Patent Enforcements

Intellectual property protection is crucial given the competitive landscape among ophthalmic therapies including generics encroaching on proprietary formulations such as Phentolamine solution branded as RYZUMVI®. Following Sandoz's filing of an abbreviated new drug application seeking generic entry prior to patent expiration on eight patents covering RYZUMVI®, Opus alongside its commercialization partner initiated patent infringement litigation filed March 2025 in New Jersey District Court aiming for injunctive relief against launch ahead of patent term expiry [S10][S14][S18].

Currently mid-way through fact discovery stages with trial scheduled January 2027 timeline places material uncertainty on prolonged exclusivity window for this small-molecule franchise that supplements Opus’s chiefly experimental gene therapy portfolio revenue base.

The trial’s outcome could impact revenue potential indirectly influencing capital allocation priorities depending on settlement or adjudication results given litigation cost burdens and resource diversions inherent to such legal contests.

Looking Forward: Key Milestones and Market Readiness Indicators to Watch

Explicit financial guidance or forecasted milestones are not disclosed; hence monitoring centers on anticipated data readouts from ongoing Phase 1/2 studies primarily involving OPGx-LCA5 will be pivotal for validating safety signals and preliminary efficacy endpoints underpinning accelerated development claims.

Regulatory submissions linked to orphan drug expansions or rare pediatric disease designations could materially shift timelines favorably if granted multiples times over.

Manufacturing scale-up progresses remain critical since commercial production readiness hinges heavily on successful CMO transfers ensuring quality compliance without supply interruptions particularly amid the complex manufacturing requirements intrinsic to AAV vectors.

Given constrained share issuance capability curtailing simple equity fundraises future liquidity undertakings around alternative financing structures will warrant close scrutiny if pipeline advancement accelerates post-positive clinical signals.

Overall risk adjusted outlook balances technological promise rooted in exclusive academic platforms delivering differentiated genotypic targeting within a high unmet medical need space versus daunting operational realities entailing regulatory complexity, reimbursement volatility, IP litigations risks plus capital resource tightness typical among pre-revenue gene therapy developers.

This analysis relies solely on information sourced from publicly filed SEC documents as well as primary company disclosures without speculative projections beyond stated facts or metrics [F1]–[S29]. Investors should evaluate developments above while considering broader sector dynamics impacting advanced gene therapy commercialization prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments