Alzamend Neuro’s Development Stage Challenges and Funding Maneuvers Define Near-Term Trajectory

Clinical progress with AL001 underpins Alzamend Neuro’s growth outlook amid persistent operating losses and reliance on capital markets.

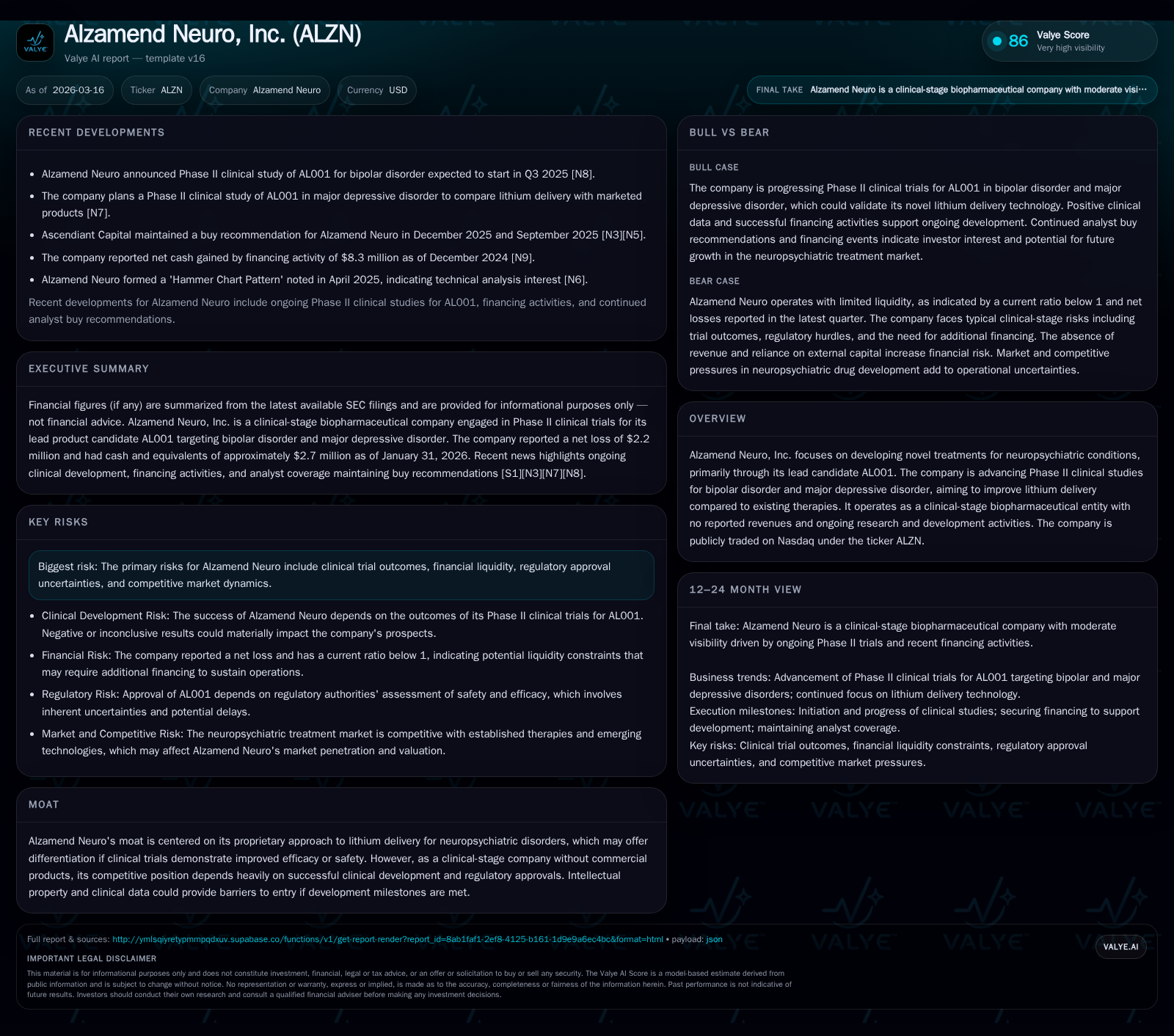

Alzamend Neuro, a clinical-stage biopharmaceutical company advancing a novel lithium delivery candidate AL001 for bipolar and major depressive disorders, remains pre-revenue with ongoing R&D expenses driving deep operating losses. Over the past four years, net losses have trended downward but remain substantial reflecting investment in Phase II trials. Recent issuance of equity through at-the-market (ATM) offerings signals continuing financing needs to fund clinical development. Key growth drivers hinge on successful trial outcomes and regulatory approval, but capital constraints and execution risks weigh heavily on near-term prospects.

Company Overview

Alzamend Neuro, Inc. operates as a clinical-stage biopharmaceutical company focused on neuropsychiatric disorder treatment innovation. Its lead candidate, AL001, is designed as a proprietary lithium delivery therapy aimed at managing bipolar disorder and major depressive disorder more effectively than currently available formulations. The intent is to enhance therapeutic benefit while mitigating conventional lithium’s narrow therapeutic window and side effects.

As of early 2026, Alzamend remains pre-commercial with no reported revenues and depends entirely on external financing to sustain R&D operations. The company's Nasdaq-listed Common Stock trades under the ticker ALZN.

Historical Financial Performance

Operating at an intensive research and development phase, Alzamend has endured multi-year losses typical for biotech firms without marketed products. From FY2022 through FY2025 (periods ending April 30), operating income losses registered:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -5 | -7 | -4 | +54.6% |

| 2024 | -10 | -8 | -10 | +33.1% |

| 2023 | -15 | -9 | -15 | -20.4% |

| 2022 | -12 | -7 | -12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -113.8 |

| 2024 | 383.5 |

| 2023 | -488.5 |

| 2022 | -92.6 |

Source: SEC companyfacts cache [F1].

Note: Operating income and net income figures represent full fiscal years ending April each year.

The stepwise reduction in losses from FY2023 to FY2025 may reflect cost rationalizations or shifting R&D focus. However, cash flow from operations continues firmly negative ($-6.57M in FY2025), underscoring ongoing burn tied to costly clinical trials.

Equity positions fluctuated significantly—turning negative in FY2024 before recovering in FY2025—which likely illustrate capital raises offsetting prior deficit erosion.

Capital Structure and Funding Activities

Alzamend has actively managed its capital structure to facilitate liquidity needs:

- In October 2025 and September 2025 filings [S18][S19], the company eliminated Series B and C convertible preferred stocks via Certificates of Elimination filed with Delaware authorities. This streamlines the equity base by removing preferred classes that previously complicated ownership.

- On March 6, 2026 [S13][S15], Alzamend executed an ATM equity sales agreement with Ascendiant Capital Markets enabling flexible sales of up to $3 million in common shares over time under Nasdaq-compliant offering protocols.

- The company issued common stock upon conversion of preferred stock during Fall 2025 quarter-end periods indicating continued reliance on equity issuances for funding rather than debt instruments.

Notably absent are any dividend distributions or share repurchase programs consistent with early development stage priorities where capital preservation is paramount.

Future Growth Prospects

Growth prospects for Alzamend hinge explicitly on its AL001 candidate's clinical progress. Positive top-line data from Phase II studies targeting bipolar disorder and major depressive disorder could unlock value by validating the company's novel lithium delivery mechanism.

Success here would enable progression toward pivotal Phase III trials and eventual regulatory submissions potentially culminating in commercialization—representing a fundamental shift from expense-heavy R&D into revenue generation.

However:

- Clinical trial outcomes pose substantial binary risk given the historically high failure rates in psychiatric drug development.

- Market competition includes both generic lithium salts long entrenched as standard of care and emergent neuropsychiatric platforms targeting overlapping indications.

- Regulatory timelines remain subject to FDA discretion impacting launch pacing.

- Financing capacity is critical since further trials will require sustained capital infusions; dilution concerns could impact share valuation adversely if frequent financings recur.

Forecasts and Milestones To Monitor (Analysis)

No explicit company guidance or financial forecasts are disclosed within the latest SEC filings or news documents.

Investors should monitor:

- Announcement dates for interim or final Phase II data readouts;

- Updates on patient enrollment status in ongoing studies;

- Additional equity offering filings signaling liquidity runways;

- Regulatory feedback or Fast Track designation developments;

- Strategic partnerships which might bolster resources or expedite commercialization pathways.

Such milestones could materially affect operational visibility beyond day-to-day funding matters.

Returns and Capital Allocation

Return metrics remain suppressed given lack of profitability:

- Estimated ROE based on latest net income relative to equity is approximately -114%, reflecting the expected substantial loss profile for a firm investing heavily ahead of revenues [F1].

- Absence of positive cash flows chastens near-term return prospects; however gradual improvement in operating cash flow signals controlled burning trends consistent with focused pipeline advancement strategies.

- No capital returned via dividends or share repurchases has been documented [S17][S18][S19], appropriate for current development stage priorities where reinvestment dominates allocation choices.

Industry Context (Analysis)

The neuropsychiatric drug space represents a complex blend of sizable unmet medical need alongside intricate therapeutic challenges including subjective symptom assessment and patient heterogeneity complicating trial endpoints. Lithium remains a mainstay treatment but suffers poor tolerability profiles leading to adherence issues that innovative delivery systems like AL001 aim to improve.

Successful differentiation through improved pharmacokinetic profiles or safety could help carve defensible market niches amidst competitive pipelines employing alternative mood stabilizers or digital therapeutics.

Risk Considerations

Key risks disclosed underscore:

- Clinical trial uncertainties potentially yielding inconclusive or unfavorable results,

- Persistent liquidity management challenges necessitating recurring access to capital markets,

- Regulatory hurdles given complex CNS disease indication approvals,

- Competitive dynamics including off-patent drug incumbents,

- Loss of key personnel as noted by recent director passing affecting governance [S20].

These factors collectively frame a high-risk/high-reward profile typical for innovation-stage biotechnology firms.

Conclusion

Alzamend Neuro continues advancing its lead AL001 compound in neuropsychiatric indications while navigating steep financial burdens characteristic of clinical-stage entities lacking revenue streams. While historical financials reveal significant though improving operating losses funded through equity raises—including recent ATM arrangements—the company's future hinges mainly on successful execution of ongoing Phase II studies validating its proprietary lithium delivery technology.

Investors should keep close watch on developmental milestones alongside liquidity management updates which will substantially influence operational runway and strategic optionality going forward.

This report draws exclusively from publicly available SEC filings up to March 16, 2026 ([F1], [S2]–[S20]) and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments