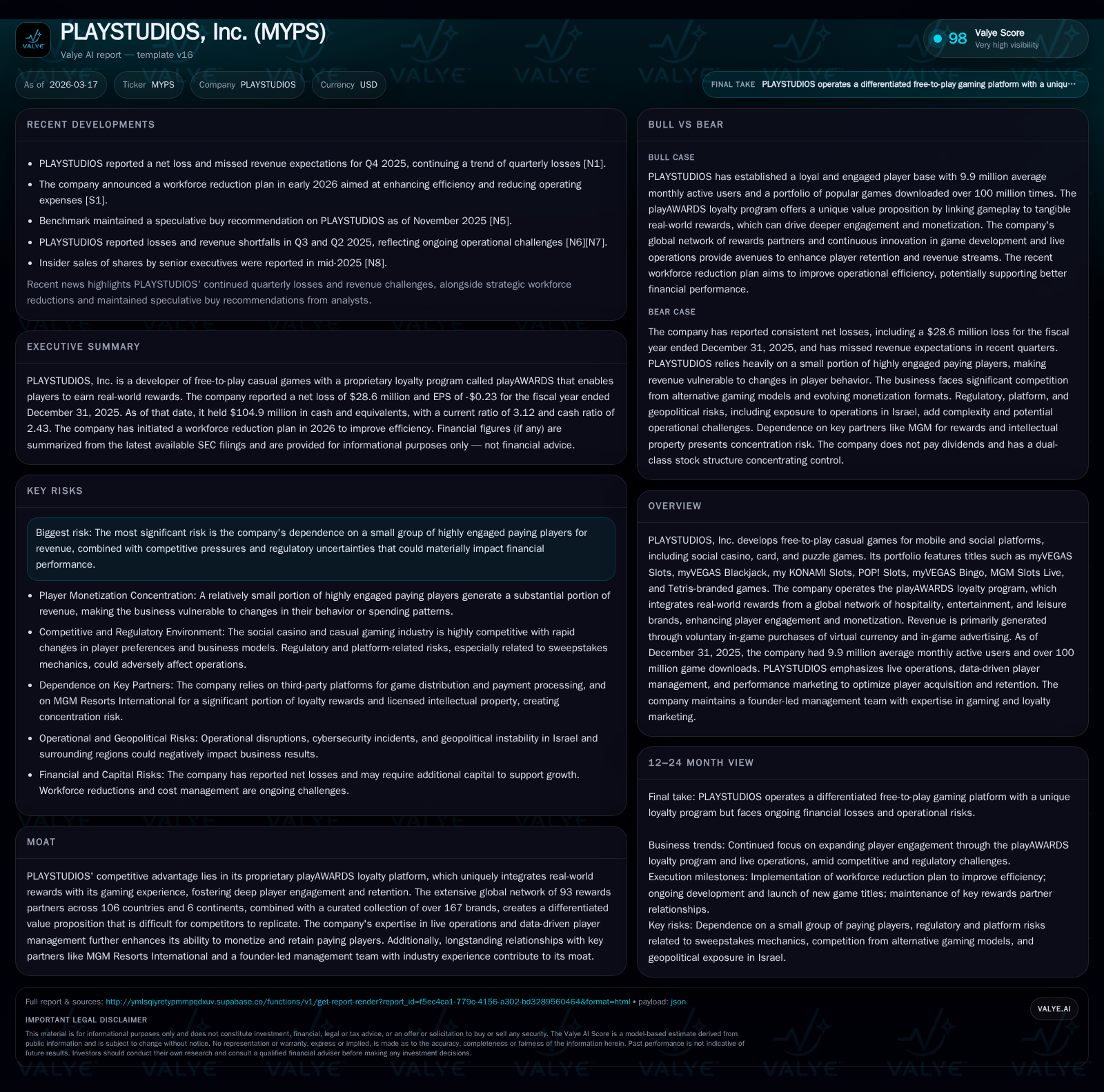

PLAYSTUDIOS’ Loyalty Edge Tested by Q4 Miss and Regulatory Hurdles

PLAYSTUDIOS’ unique playAWARDS loyalty platform supports engagement amid recent financial challenges and regulatory scrutiny.

PLAYSTUDIOS continues to leverage its proprietary playAWARDS loyalty program, which integrates extensive real-world rewards to drive player retention in its free-to-play social casino games. Despite this moat, the company reported a Q4 loss with revenue missing estimates, underscoring persistent monetization pressures exacerbated by intensifying regulatory uncertainties around sweepstakes-based mechanics. With rising competition from alternative gaming models and evolving compliance demands, PLAYSTUDIOS faces headwinds that may constrain near-term growth, although ample liquidity and data-driven live operations provide some operational resilience.

Historical Financial Performance: Growth Patterns and Profitability Trends

PLAYSTUDIOS’ financial trajectory through FY2025 reveals incremental progress in mitigating losses amid a challenging market backdrop [F1]. Operating income losses decreased by 27.2% from -$32.9 million in FY2024 to -$23.9 million in FY2025, signaling improved cost management or revenue stabilization efforts. Net income remained nearly unchanged YoY at approximately -$28.6 million, reflecting ongoing pressure despite operational improvements.

Operating cash flow declined markedly by 42.4%, from $45.7 million in FY2024 to $26.3 million in FY2025, suggesting headwinds impacting conversion of revenues into liquid funds or increased working capital needs. Capital expenditures sharply reduced by nearly three-quarters YoY ($968k vs $4 million), likely reflecting a cautious investment posture amidst uncertain growth prospects.

Despite continued losses at the bottom line, PLAYSTUDIOS maintained consistent share repurchases ($3.5 million in FY2025) indicative of management’s intent to support shareholder value within constrained profitability contexts [F1]. The company’s balance sheet remains robust with cash & equivalents at $105 million and a strong current ratio of roughly 3.12, providing operational liquidity buffers.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -29 | 26 | -24 | 1 | +0.2% |

| 2024 | -29 | 46 | -33 | 4 | -47.9% |

| 2023 | -19 | 52 | -10 | 6 | -9.1% |

| 2022 | -18 | 33 | -28 | 12 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 3 | 25 | -12.6 |

| 2024 | 31 | 42 | -11.7 |

| 2023 | 15 | 45 | -6.7 |

| 2022 | 4 | 21 | -5.9 |

Source: SEC companyfacts cache [F1].

In sum, while PLAYSTUDIOS has made progress reducing operating losses and managing expenditures efficiently, the contraction in cash flow signals ongoing monetization challenges requiring continued operational focus.

The playAWARDS Platform: Core Moat Driving User Engagement and Monetization

At the heart of PLAYSTUDIOS’ competitive differentiation lies its proprietary playAWARDS loyalty platform [S1][F1]. This system uniquely ties virtual currency accumulations within games like myVEGAS Slots and MGM Slots Live to tangible real-world rewards redeemable across an expansive network of hospitality and leisure brands.

The program boasts partnerships with over 93 rewards partners spanning six continents and more than 167 brands globally—an exceptionally broad affiliation rare among social casino peers [S1]. This international reach not only boosts player engagement but also diversifies consumption touchpoints that underpin monetization dynamics.

From an industry perspective, integrating offline rewards creates stickiness beyond typical virtual currency models by delivering perceived enhanced value propositions combining gameplay with real tangible benefits [S1]. This approach supports the retention of high-yield players who contribute the bulk of revenue—a critical factor as only a small subset of users monetize meaningfully [S1].

Furthermore, PLAYSTUDIOS emphasizes live operations expertise including continuous player behavior analytics and performance marketing optimization to refine acquisition efficiency and maximize lifetime value [S1]. Their data-driven methodologies target player yield optimization which maximizes returns on advertising spend despite competitive pressures.

Overall, playAWARDS establishes a substantial moat not easily replicated due to the complex global reward partnerships infrastructure coupled with deep integration into user experience flows.

Regulatory Landscape: Sweepstakes Mechanics Under Intensified Scrutiny

The regulatory environment emerges as a significant constraint for PLAYSTUDIOS given its reliance on sweepstakes-based promotional mechanics embedded in many social casino titles . Sweepstakes regulations are jurisdictionally fragmented across U.S. states creating legal ambiguities around what constitutes gambling versus lawful promotional activities [S7][S8].

Compliance now requires stringent age verification, geo-fencing controls, anti-money laundering protocols, and tailored state-specific variations—measures that increase operating costs and challenge real-time game functionality modifications [S7]. The company acknowledges potential impacts on player experience if required alterations reduce smoothness or appeal of these features [S7].

Third-party dependencies amplify risk: app platforms, payment processors, and service providers impose their policies independently—sometimes classifying sweepstakes mechanics as gambling-adjacent requiring restrictive measures or outright service withdrawal even absent legal mandates [S15]. Such unilateral actions could abruptly limit game availability or payment processing capabilities.

Further complicating matters are evolving consumer protection laws governing transparent marketing disclosures for in-game purchases targeting vulnerable groups including minors [S6][S24]. COPPA considerations add complexity given regulatory sensitivity towards children’s privacy even if primary audiences exceed age thresholds [S24].

Internationally, data privacy laws like GDPR impose additional constraints affecting personalized offers tied to loyalty points or virtual currency redemption features within playAWARDS [S16][S26][S27].

Collectively, these factors represent an uncertain legal landscape requiring continuous compliance vigilance that could hinder agility in product development or market expansion.

Competitive Pressures: Market Position Amid Alternative Gaming Models

PLAYSTUDIOS operates amid intensifying competition as the traditional social casino sector experiences revenue erosion linked partly to emergence of alternative gaming formats employing sweepstakes structures [S1][S23]. These newer entrants attract players through a combination of familiar gameplay replication merged with chances at real-world prizes delivered via promotional sweepstakes models.

This shift diverts paying player attention away from classic social casino offerings toward hybrid products promising perceived higher-value incentives [S23]. Marketing investments increasingly favor sweepstakes-based products resulting in rising user acquisition costs for PLAYSTUDIOS’ traditional portfolio.

Given that a small proportion of highly engaged paying users drives revenue significantly, migration risks among this group threaten gross monetization substantially [S1][S23]. Maintaining relevance thus demands nimble live operations capable of rapid iteration on content update cadence, incentive designs, and personalization strategies.

While PLAYSTUDIOS leverages its loyalty ecosystem advantageously to combat churn pressures, the broader market tide appears inclined towards evolving business models that blur lines between gaming and prize-linked incentives [S23]. Sustaining growth entails both innovation within their existing game suite plus exploration of adjacent formats compliant with evolving regulations.

Liquidity & Capital Allocation: Debt, Cash Flow & Shareholder Returns

Solid liquidity underpins PLAYSTUDIOS’ capacity to navigate current headwinds—$105 million cash reserves pair with strong short-term asset positioning generating a current ratio around 3.12 by end-FY2025 [F1][S4]. Importantly the firm’s revolving credit facility remains undrawn but faces expiration mid-2026 introducing refinancing risk or need for alternate funding sources if capital needs arise [S4].

Operating cash flow contraction juxtaposed against sharply reduced capital expenditure drives modestly positive free cash flow estimated at $25.4 million (CFO minus capex), indicating more efficient capital deployment [F1]. This suggests deliberate restraint on investing spending possibly focused on sustaining core product lines rather than expansionary initiatives.

Equity base declined slightly but remains strong at approximately $228 million while calculated ROE hovers near -12.6%, reflective of ongoing net losses offsetting equity levels [F1]. Despite unprofitability metrics persisting management executed share repurchases totaling about $3.5 million signaling confidence or opportunistic valuation stance amidst constrained earnings capacity.

No dividends were declared consistent with company policy acknowledging reinvestment priorities amid structural market challenges [S1]. Future capital allocation likely balances defensive liquidity preservation against selective buybacks aligned with share price dynamics.

Future Growth Opportunities & Structural Challenges

Company disclosures convey guarded optimism recognizing growth levers tied primarily to leveraging their proprietary loyalty program’s expanding brand partner network underpinning enhanced player engagement globally [N1][S1]. Expansion beyond existing geographies or verticals within hospitality-recreation sectors affiliated with playAWARDS could deepen reward attractiveness thus positive monetization impacts.

However growth assumptions remain tempered by prominent caveats: regulatory complexities described earlier impose uncertainty on feature availability or geographic scope affecting addressable market sizes particularly given variable legal interpretations per region [S5][N1]. Further competitive encroachment mandates continuous agility deploying data-driven player management tools refined via live operations capabilities emphasizing retention yield improvements rather than pure user base volume gains alone.

Thus while product innovation is ongoing alongside strategic marketing investments targeting optimal return on spend metrics for a concise paying cohort; underlying sectoral shifts toward dual currency/reward schemes outside classical playAWARDS design represent execution risk vectors needing monitored alignment with evolving legislation backdrop.

Key Milestones to Monitor: What Investors Should Watch Next

PLAYSTUDIOS’ trajectory warrants careful observation of several near-term indicators:

- Upcoming quarterly earnings releases will be pivotal for assessing evidence of stabilization or renewed deterioration in monetization trends following FY2025 disappointments reported recently including Q4 misses [N1][S3].

- Decisions surrounding renewal or replacement terms for their revolving credit facility expiring June 24th 2026 will bear strongly on balance sheet flexibility especially if external capital markets conditions remain volatile [S4][N1].

- Regulatory developments especially any new rulings related to sweepstakes structures from U.S states or changes adopted by major digital distribution platforms could materially impact product availability or require costly compliance overhauls potentially disrupting player retention patterns [N1][S5][S8].

- Updates on expansion progress within the playAWARDS partner ecosystem could signal bolstered long-term moat strength through diversified rewards underlying future player lifetime value enhancement.[N1]

- Observations of industry-wide shifts influenced by competitor innovations incorporating broader sweepstakes-like incentivization elements will be essential contextually assessing strategic positioning relative to emergent formats.[S23]

These events collectively shape critical near-to-medium term performance benchmarks informing operational resilience and strategic execution effectiveness beyond raw headline financials.

This analysis reflects information available as of March 17th 2026 based on publicly filed documents and press releases without investment recommendations or forecasts beyond documented guidance. It is intended as an objective assessment incorporating sector-specific insights relevant for internal stakeholders evaluating PLAYSTUDIOS’ fundamental performance drivers balanced against legal-regulatory constraints impacting business durability.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments