Tavia Acquisition Corp’s Growth Hinges on Successful Business Combination Execution by Mid-2026 Deadline

A Cayman Islands blank check company emphasizing sustainability sectors holds $120M in trust post-IPO but faces execution and liquidity risks.

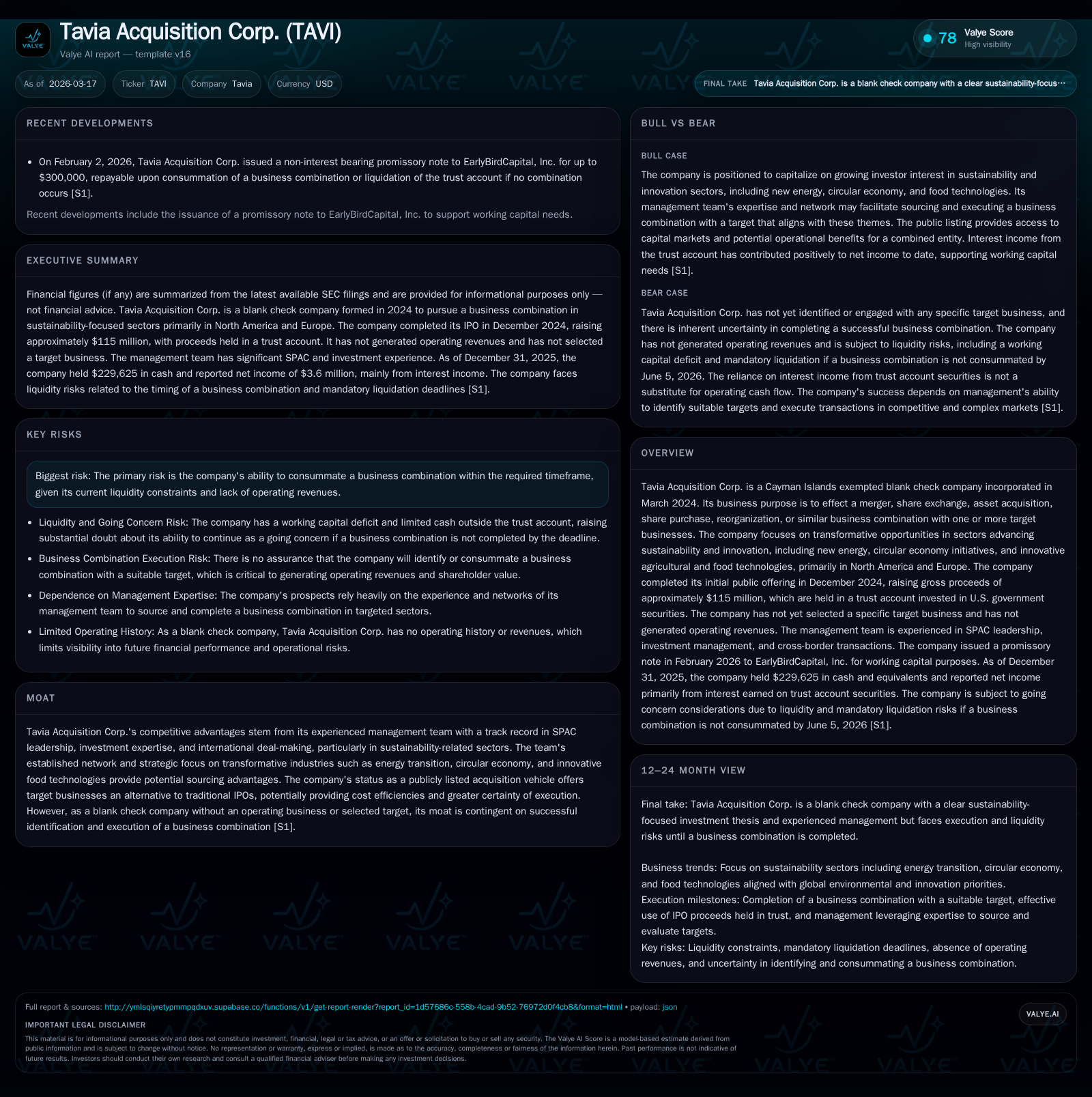

Tavia Acquisition Corp., incorporated in early 2024, completed its IPO in December 2024 raising approximately $115M, which is held in a trust account invested in U.S. government securities. The firm has yet to identify or engage with any target business but aims to focus on transformative industries such as new energy, circular economy, and innovative food technologies primarily across North America and Europe. While the management team's SPAC experience provides some competitive advantage, Tavia operates with no revenues and is under pressure to consummate a business combination within an 18-month window ending mid-2026. The company anticipates continuing cash burn from operating costs while relying on trust account funds and potential sponsor loans for operations and acquisition efforts.

Company Overview and Historical Performance

Tavia Acquisition Corp. (TAVI) was established as a Cayman Islands exempted blank check company on March 7, 2024. Its sole purpose is to consummate a business combination with one or more target entities primarily within transformative sectors that contribute to sustainability and innovation. The geographic focus centers on North America and Europe with thematic interests including new energy solutions, circular economy initiatives, and innovative agricultural/food technologies [S1].

The company completed its Initial Public Offering (IPO) on December 5, 2024, issuing 10 million units at $10 each, plus subsequent over-allotments and private placement units to the Sponsor and EarlyBirdCapital (EBC), aggregating roughly $115 million gross proceeds [S1][S9]. Proceeds from the public units and part of private placement proceeds were placed into a Trust Account invested largely in U.S. Treasury securities with short maturities (up to 185 days) preserving capital until the consummation of a business combination or refund at liquidation [S6][S8].

From inception through December 31, 2025, Tavia has not operated any businesses that generate revenue. Instead, it has earned interest income derived from investments of IPO proceeds held in the Trust Account: approximately $351,937 in the initial period through end-2024 and $4.83 million in calendar year 2025 [F1][S1][S6]. These interest earnings drove net income reported at $79,518 for the partial first year (March-December 2024) and $3.61 million for full-year 2025 despite underlying operating losses arising from administrative costs [F1].

Operating expenses include expenses related to being a public company—legal fees, accounting services, compliance costs—as well as due diligence expenditures connected with pursuing potential acquisition targets. Operating loss increased markedly from roughly $272K in 2024 to $1.22 million in 2025 reflecting scaling activity around transaction preparation [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 4 | -674034 | -1221951 | +4434.1% |

| 2024 | 0 | -74275 | -272419 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -342.3 |

| 2024 | 19.4 |

Source: SEC companyfacts cache [F1].

Note: Net income growth is predominantly due to increased interest income on trust assets rather than operating improvements.

Growth Prospects

Tavia’s growth trajectory fundamentally depends on successfully identifying and closing its inaugural business combination by June 5, 2026—that date marking the end of its mandated combination period under its IPO terms [S1][S14]. To date, management reports no selected targets nor substantive discussions related to mergers or acquisitions [S1].

The management team leverages extensive SPAC leadership experience alongside networks spanning private equity investors, industry executives, bankers, legal advisors, and strategic partners focused on ESG-aligned sectors. This positioning may afford preferential access to deals within new energy technologies (e.g., hydrogen infrastructure), circular economy models (material recycling innovations), and agri-food tech startups pushing sustainable food systems [S13][S27]. However, these opportunities remain contingent upon market conditions and deal pipeline quality.

Potential growth drivers include:

- Completing one or several acquisitions that fit Tavia’s strategic thematic focus,

- Utilizing IPO trust assets possibly combined with debt or equity financing structures,

- Exploiting cost advantages relative to traditional IPOs for private companies seeking public listing,

- Leveraging management's cross-border deal-making expertise between North American and European markets.

Constraints comprise:

- Approaching expiration of the combination window creating time pressure,

- Liquidity limitations outside the Trust Account requiring sponsor loans or financing,

- Competition from other investment vehicles for high-demand sustainability sector targets,

- Potential dilution effects if shareholder redemptions are significant post-deal announcement.

Forecasts and Milestones

Explicit forward guidance is absent given the early-stage status without active operations or targets [N#][S#]. Key milestones investors should monitor include:

- Announcement of target(s) selection triggering proxy filings,

- Shareholder approval vote outcomes for proposed business combination(s),

- Redemption election volumes impacting available working capital post-combination,

- Final consummation of transaction(s) before June 5, 2026 deadline,

- Any extensions granted under SPAC rules or amendments modifying redemption mechanics.

Capital Allocation and Returns

As a blank check company prior to deal completion, Tavia’s capital allocation focuses solely on preserving IPO proceeds within the Trust Account while funding operational expenses externally. No dividends or share repurchases have been enacted given lack of operating cash flow generation or distributable earnings [F1][S9].

As of December 31, 2025, total assets were approximately $121 million primarily comprising marketable securities held in the Trust Account ($120.75 million) alongside nominal cash balances ($229K). Liabilities included accrued offering costs and related party promissory notes totaling about $1.41 million [F1][S4].

The company reported a working capital deficit outside the Trust Account of roughly $1.05 million underscoring constrained operational liquidity beyond acquisition activities [F1][S14]. Sponsor-related loans exist—such as a non-interest-bearing promissory note up to $300K issued early 2026—to provide interim funding but repayment depends fully on transaction outcomes [S13][S18].

Return metrics are not yet meaningful given absence of operating earnings; calculated return on equity is negative due to accumulated deficit against minimal shareholder equity excluding Trust assets [F1]. Future returns hinge critically on the quality and success of acquired businesses.

Risks Summary

Key risks include execution risk tied to completing a qualifying business combination within prescribed deadlines; failure would trigger liquidation returning shareholders’ pro-rata funds less expenses—a likely suboptimal outcome compared with ongoing operations value creation [S23][S14]. Other risks encompass limited liquidity outside Trust accounts requiring sponsor advances; rising administrative expenses; shareholder redemption rates potentially limiting deal funding capacity; competition for suitable acquisition targets; regulatory compliance burdens associated with public company status; and concentration risk based on geographic/thematic investment focus.

Conclusion

Tavia Acquisition Corp remains an early-stage blank check entity holding substantial trust-accounted proceeds following a successful late-2024 IPO but without an identified acquisition target over a year later approaching its mid-2026 deadline. Management’s sector expertise theoretically positions it well for sustainable thematic investments spanning new energy transition through circular economy innovations into agri-food technologies across key western markets.

Nevertheless substantial uncertainties persist regarding timing feasibility amid growing external operating costs and tight liquidity buffers reliant on sponsor financing support. Stakeholders should monitor forthcoming announcements regarding target selection timelines and shareholder approvals as critical indicators shaping whether value creation opportunities materialize or if liquidation becomes necessary.

This analysis is based solely on publicly filed documentation without speculative forecasts beyond noted facts. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments