WM Technology’s Growth Moderation and Capital Stability in Legal Cannabis Marketplace

The company faces revenue pressures amid regulatory constraints but maintains operational cash flow and a strong balance sheet.

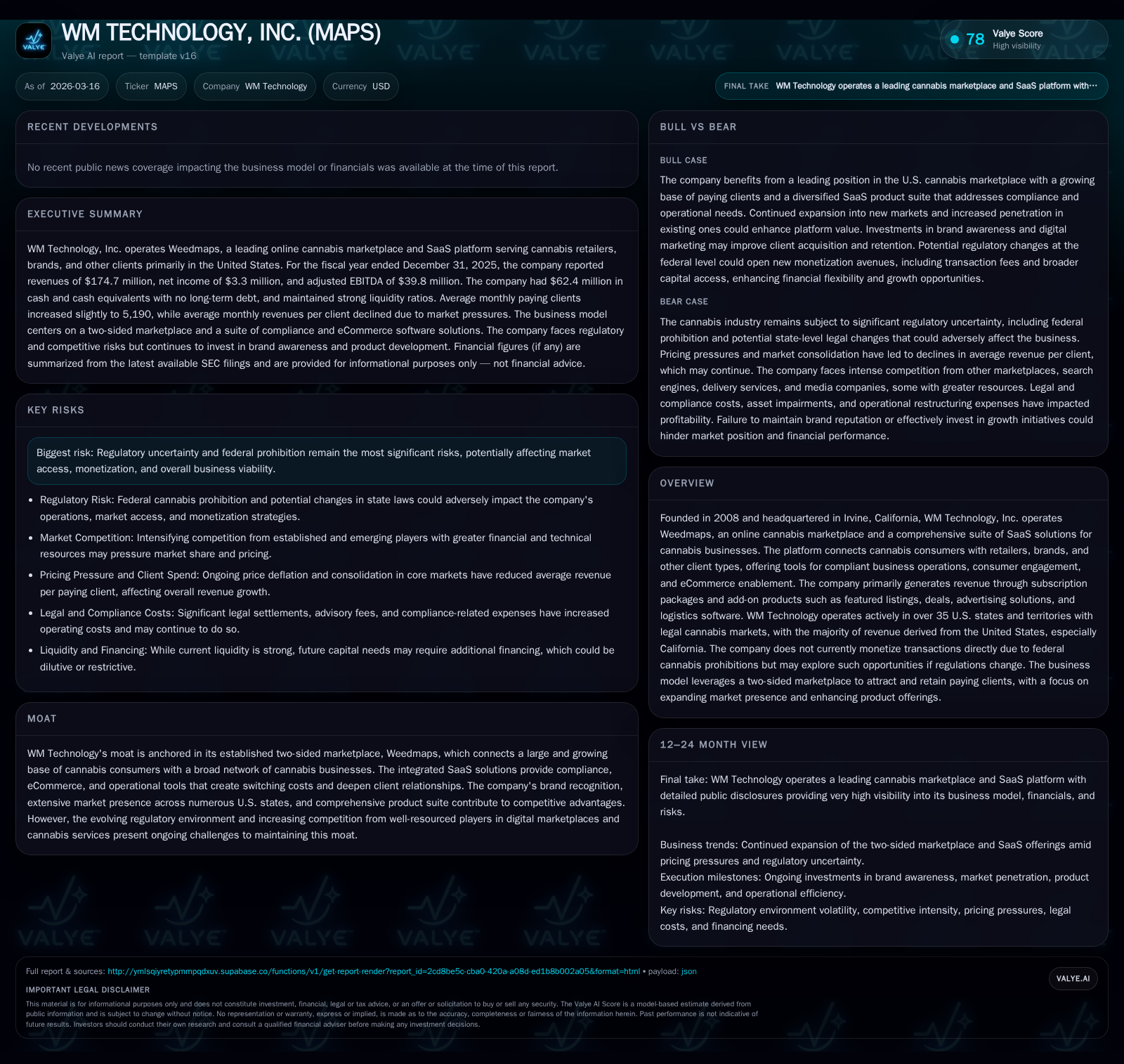

WM Technology, Inc. (MAPS) operates the Weedmaps platform, a leading cannabis marketplace coupled with SaaS solutions for retailers and brands, primarily in the U.S. Its revenue declined modestly year-over-year in 2025 driven by client monetization challenges. Profitability remains under pressure as net income and operating income contracted significantly from prior-year levels, reflecting margin headwinds and increased expenses including asset impairments. The company’s cash position remains healthy with no long-term debt, supporting ongoing investments in product development and market expansion. Regulatory uncertainty continues to cap upside potential but also preserves a moat through industry specialization.

Company Overview

Founded in 2008 and based in Irvine, California, WM Technology, Inc. operates Weedmaps — a commerce-driven online marketplace for cannabis consumers and a comprehensive suite of software-as-a-service (SaaS) solutions tailored to cannabis businesses including retailers and brands. The company’s platform facilitates compliance management, eCommerce enablement, consumer engagement, and operational efficiencies for its clients primarily located within the United States where over 35 states currently have legalized adult or medical cannabis usage [S1],[S10].

Historical Performance and Revenue Drivers

For fiscal year 2025, WM Technology reported revenues of $174.7 million compared to $184.5 million in 2024, reflecting a modest decline of approximately 5.3% [F1],[S1]. Despite this revenue reduction, the number of average monthly paying clients increased slightly from 5,077 to 5,190 during the same period. This divergence suggests either lower monetization per client or a shift towards smaller clients or lower-priced packages since average monthly revenue per paying client declined by about 7.4%, from $3,029 down to $2,805 [F1],[S1].

Net income compressed dramatically from $7.6 million to roughly $2.0 million (a decrease exceeding 74%), attributable principally to elevated operating expenses and non-recurring asset impairment charges totaling approximately $7.8 million in the year ended December 31, 2025 [F1],[S1],[S22]. Operating income fell even more steeply—by nearly 95%—from about $14.7 million in the prior year to less than $1 million in fiscal 2025 [F1]. These profitability pressures underline mounting margin headwinds possibly exacerbated by pricing competition or increased investment outlays.

The company’s cost structure is dominated by sales & marketing along with product development expenses: sales & marketing costs declined slightly by about 4%, whereas product development spending decreased more substantially (down nearly 23%) reflecting possible cost discipline or phasing of engineering projects [S22]. General and administrative costs increased by roughly 9%, contributing to overall operating expense growth despite reductions elsewhere.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 2 | 26 | 1 | -74.3% |

| 2024 | 8 | 37 | 15 | +177.2% |

| 2023 | -10 | 23 | -18 | +91.5% |

| 2022 | -116 | -12 | -70 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 3.4 |

| 2024 | 21.2 |

| 2023 | -60.4 |

| 2022 | -866.9 |

Source: SEC companyfacts cache [F1].

Cash Flow and Capital Allocation

Operating cash flow remained positive but declined roughly 28.6% from approximately $36.7 million in fiscal year 2024 to just over $26 million in fiscal year 2025 [F1],[S24],[S26]. Capital expenditures are maintained around the mid-teens million USD annually though recent exact figures are not fully disclosed due to reporting timing [F1],[S21].

WM Technology entered fiscal year-end with approximately $62.4 million of cash and equivalents on hand balanced against no outstanding long-term debt obligations [F1],[S7],[S13]. This conservative leverage profile supports ongoing investment into software platform enhancements and marketing initiatives required for competitive positioning.

No dividends have been declared or paid historically as WM continues focusing on reinvestment into growth-related initiatives rather than shareholder distributions at this stage [S1]. There is no evidence of share repurchases either.

Business Model Nuances and Market Positioning

WM Technology’s core value proposition lies in its two-sided marketplace "Weedmaps," coupling cannabis consumers seeking discovery information with licensed retailers and brands requiring compliant SaaS solutions that include inventory management integrations (POS connectors), consumer engagement tools (e.g., campaign management), order fulfillment systems, analytics dashboards (WM Insights), and premium advertising placements such as Featured Listings and promotional deals [S10],[S23].

Its revenue streams predominantly emanate from subscription fees for Weedmaps for Business SaaS packages plus additional fees tied to add-on products like advertising slots and CRM functionalities [S10],[S22]. The company does not presently monetize end consumer transactions directly due to U.S federal restrictions that preclude involvement in plant-touching activities; however, it acknowledges significant latent opportunity should federal legislation evolve permitting transaction fee capture or payment processing [S8],[S12].

Geographically concentrated within U.S regulated markets—with California alone generating nearly 56% of revenues—the company benefits deeply from regulatory complexity acting as a barrier-to-entry but also must contend with evolving legal landscapes that could either open growth doors or introduce new compliance costs [S4],[S12].

Future Growth Prospects and Constraints

WM Technology anticipates expanding its footprint aligned with broader legalization trends across U.S states as well as select international non-U.S jurisdictions where limited non-monetized listings exist such as Canada and parts of Europe [S10]. It aims to deepen market penetration by growing the average number of paying clients beyond current levels through enhanced marketing efforts as recently indicated [N1],[S9]. Product innovation focuses on improving integration capabilities (e.g., API enhancements), analytics sophistication via WM Insights enhancements, and enriched consumer-facing discovery experiences on Weedmaps.

Nonetheless, these growth prospects face material headwinds stemming primarily from regulatory uncertainty at the federal level that limits potential monetization levers—particularly direct transaction gains—and risks operational disruption should legal regimes tighten unexpectedly or enforcement actions increase [S8],[S16]. Competition is intensifying as large digital marketplaces eye cannabis services while incumbents jockey for dominant positioning using differentiated SaaS offerings creating pressure on pricing power.

Recent Developments

On March 16, 2026 WM Technology announced leadership strengthening moves alongside compliance updates regaining Nasdaq listing standards following earlier challenges due to stock price volatility [N1],[S27]. Separately the company resolved material class action shareholder litigation subject to court approval involving claims related to historical reporting practices of user metrics [S11],[S18]. These developments potentially clear operational distractions allowing refocus on core business execution.

Returns Analysis

Based on trailing twelve-month figures from FY2025 versus FY2024: Return on Equity (ROE), derived from net income divided by equity at year-end, stands at approximately 3.4%, reflecting constrained profitability amidst substantial equity base expansion likely fueled by prior years’ equity raises during loss recovery phases [F1]. The moderate positive free cash flow estimated near $10 million (operating cash flow minus approximate capex) indicates decent cash generation amid cautious spending discipline [F1],[S24].

Conclusion

WM Technology navigates an evolving legal cannabis ecosystem leveraging an entrenched marketplace plus connected SaaS suite fostering strong client relationships through compliance-centric value-adds that create switching costs. While top-line growth moderated modestly last year amid pricing pressures and slower monetization gains per client, resilient operating cash flows supported ongoing investments into product enhancement critical for future competitiveness. The absence of leverage coupled with ample liquidity provides financial runway though profitability compression highlights challenges around scaling margins under current regulatory structures. Potential federal reforms remain pivotal catalysts for unlocking new monetization avenues exposing latent upside but regulatory uncertainty imposes natural caps on immediate expansion scope. Market incumbency paired with comprehensive integrated offerings offers WM Technology a defensible moat against new entrants though pricing competition threatens margin stability necessitating disciplined cost control paired with innovation acceleration. Investors should watch legislative shifts around federal cannabis laws closely alongside changes in client acquisition dynamics as key indicators shaping medium-term trajectory.

This analysis utilizes publicly filed SEC financial statements effective December 31, 2025 [F1,S1–29], complemented by relevant news disclosures dated through March 16, 2026 [N1]. Figures reflect consolidated operations without speculative extrapolation beyond these sources. No investment recommendations are provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments