Impact BioMedical’s Strategic Merger and Share Exchange Amid Persistent Losses and Liquidity Challenges

Impact BioMedical is navigating a major reverse merger with Dr Ashleys Limited while managing ongoing financial strains.

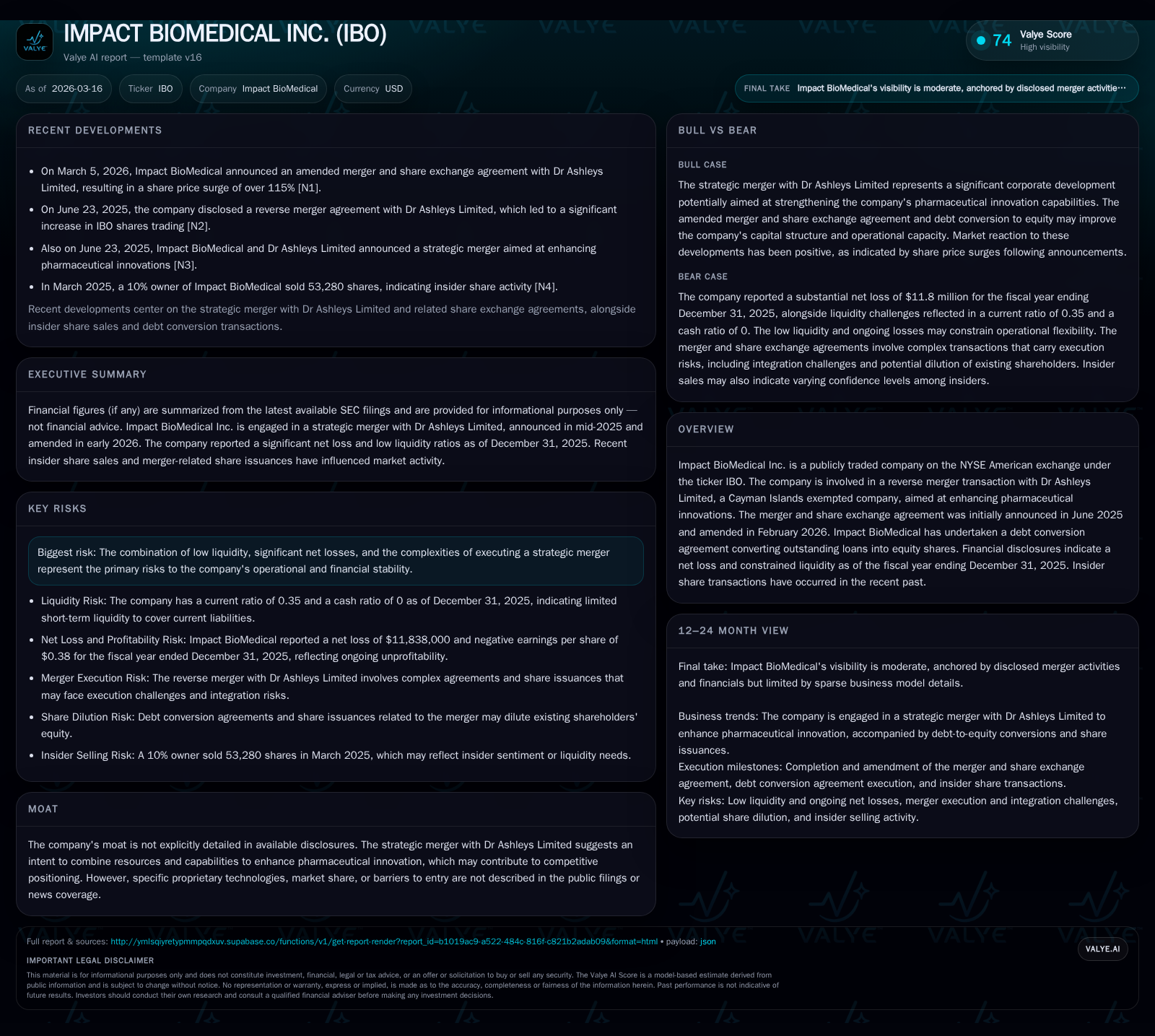

Impact BioMedical Inc. (IBO), listed on NYSE American, has undertaken a significant merger and share exchange agreement with Dr Ashleys Limited, aiming to refocus its pharmaceutical innovation efforts. Despite this strategic maneuver, the company has reported sustained net losses and limited liquidity as of the fiscal year ending 2025, reflecting operational challenges and capital constraints. The completed debt-to-equity conversion and recent amendments to merger terms highlight attempts to stabilize financing, yet the outcome hinges on successful execution amid heightened risk factors.

Company Overview and Strategic Initiatives

Impact BioMedical Inc. (ticker: IBO) operates as a nascent entity on the NYSE American exchange with an emphasis on pharmaceutical-related innovations. The company recently engaged in a reverse merger transaction with Dr Ashleys Limited, a Cayman Islands exempted company, initiating this transformational deal in June 2025. An amendment was ratified in February 2026 to clarify share issuances, extend closing deadlines, and refine governance arrangements [S1][S3][S17][N1]. This merger envisions renaming Impact as "Dr Ashleys USA Inc." post-close and restructuring its board and management under the new controlling shareholder umbrella [S25].

Alongside the merger, Impact undertook a critical Debt Conversion Agreement with DSS, Inc., converting revolving loan obligations dating back to 2023 (originally $12 million) into approximately 31.9 million common shares. This maneuver was designed to alleviate immediate debt servicing pressures during strained liquidity conditions [S10][S16][S28].

Historical Financial Performance

While limited revenue details are disclosed due to the company’s early-stage profile and transformative state, financial statements reveal persistent operational losses over recent years:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -12 | -2 | -4 | +52.1% |

| 2024 | -25 | -4 | -29 | -460.7% |

| 2023 | -4 | -3 | -4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -93.9 |

| 2024 | -580.1 |

| 2023 | -17.5 |

Source: SEC companyfacts cache [F1].

(Source: [F1])

Key observations:

- Operating loss narrowed substantially in FY2025 versus prior year (-$4.3M vs -$28.8M), reflecting either cost controls or scale changes.

- Net loss also improved by over 50% year-on-year but remains at a material deficit of nearly $12 million.

- Operating cash flow deficits persist but show some recovery.

- The current ratio is severely depressed (~0.35), signaling acute liquidity constraints as current liabilities far exceed current assets.

- Equity fluctuated dramatically from $25.2M in 2023 down to $4.3M in 2024 before recovering to $12.6M in 2025 following equity infusion activities.

This volatile financial trajectory reflects the company's transitional status during restructuring and capital infusions linked to its merger plan.

Growth Prospects and Strategic Drivers

The centerpiece growth catalyst is the forthcoming completed reverse merger with Dr Ashleys Limited which will position Impact BioMedical under a combined pharmaceutical innovation platform intended to leverage complementary resources and capabilities [N1][S1][S25]. However, company disclosures prudently note that competitive advantages or moat elements have not yet crystallized publicly; proprietary technologies and market positioning remain opaque .

Future scaling depends on several factors:

- Successful regulatory approvals including NYSE American's listing approvals for the merged entity's stock issuance [S19].

- Effective integration of Dr Ashleys’ assets, capabilities, and pipeline into Impact’s structure.

- Enhanced financing enabled by equity conversion deals to sustain operations beyond merger close.

- Ability to maintain or attract specialized talent amid transition disruptions.

Conversely, growth may be capped by ongoing operational losses demanding continuous capital injections [F1], uncertainties around timing or outcome of merger closing conditions [S19], and potential dilution effects from extensive share issuances.

Forecasts, Milestones, and What to Monitor

While explicit future guidance is not provided by Impact BioMedical in filings or news reports, key upcoming milestones include:

- Finalization of the reverse merger expected before an extended deadline of July 1, 2026 (with possible mutual extensions) [N1][S17].

- Completion of share exchanges involving management compensation shares and DSS milestone-linked shares precipitating further dilution [S17][S27].

- NYSE American’s final approval for listing of new shares issued as part of the merger consideration [S19].

- Monitoring liquidity trajectories post-merger given extremely low cash at end FY2025 ($3K) against high near-term liabilities [F1].

- Tracking legal proceedings or regulatory risks linked to merger uncertainties outlined in risk disclosures [S4][S5].

In analysis, investors should watch for proxy statement releases tied to stockholder votes approving these corporate actions that will conclusively shape control structure and capital composition.

Capital Returns and Allocation Analysis

Impact BioMedical currently shows negligible capacity for traditional capital returns such as dividends or buybacks given persistent negative net income [-$11.8M] and negative operating income [-$4.3M] despite some margin improvement in 2025 [F1]. There is no record of dividend distribution or share repurchase programs within available disclosures; recent capital allocation efforts emphasize deleveraging through debt-for-equity swaps rather than cash returns [S10][S16].

The company's ROE stands at approximately -93.9%, underscoring deep unprofitability relative to equity base amid restructuring phases [F1]. Cash flows from operations remain negative (-$1.89M in FY2025), indicating cash burn without immediate internal financing offset.

Overall capital strategy appears focused on stabilizing balance sheet via equity injection—chiefly through share exchange linked to the merger—and managing financial liabilities rather than external return of capital.

Risks Assessment

Material risks highlighted comprehensively encompass:

- Execution risk for completing complex merger transactions involving cross-border entities (Nevada corporation merging with Cayman Islands entity).

- Regulatory timing uncertainty including stock exchange approvals required for new share issuances associated with merger consideration.

- Financial distress signals owing to minimal liquidity cushion (current ratio .35), reliance on equity conversions amid sustaining operations.

- Ongoing net operating losses limiting traditional funding avenues or credit access.

- Potential adverse impacts on business continuity from management transitions or operational disruption during integration phase.

- Dependency on key stakeholders like DSS Inc., whose cooperation influences funding agreements tied to share issuances under Amendment structures [S17][S26].

These factors collectively form substantial headwinds necessitating close stakeholder vigilance as strategic restructuring unfolds.

Summary Table: Annual Financial Highlights (USD Millions)

| Year | Operating Income | Net Income | Operating Cash Flow | Current Assets | Current Liabilities |

|---|---|---|---|---|---|

| 2025 | -4.28 | -11.84 | -1.89 | 0.41 | 1.16 |

| 2024 | -28.75 | -24.71 | -3.92 | N/A | N/A |

| 2023 | -4.03 | -4.41 | -2.85 | N/A | N/A |

Note: All figures sourced exclusively from official SEC filings [F1], reflecting full fiscal year data.

Conclusion

Impact BioMedical stands at a pivotal juncture defined by an ambitious reverse merger aimed at reshaping its pharmaceutical innovation prospects via strategic combination with Dr Ashleys Limited. While such corporate actions could unlock synergies or growth platforms not currently visible given limited moat data, the company's historical financial performance illustrates significant operational losses compounded by tight liquidity constraints.

Recent agreements converting debt into equity offer near-term relief but also raise dilution concerns that shareholders must weigh carefully against potential upside from merged capabilities once fully realized post-closing expected mid-2026 or later extensions if necessary.

The unfolding situation demands monitoring regulatory approvals, execution progress on transaction milestones, evolving liquidity positions post-merger consummation, and broader integration outcomes impacting long-term viability beyond contemporary disruptions dominating historical results.

This report synthesizes exclusively sourced public filings and news disclosures without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments