Omega Flex, Inc.: Resilience Tested by Shifting Market Dynamics

Omega Flex leverages patented manufacturing and steady capital returns while facing pressures from housing market softness and intense competition.

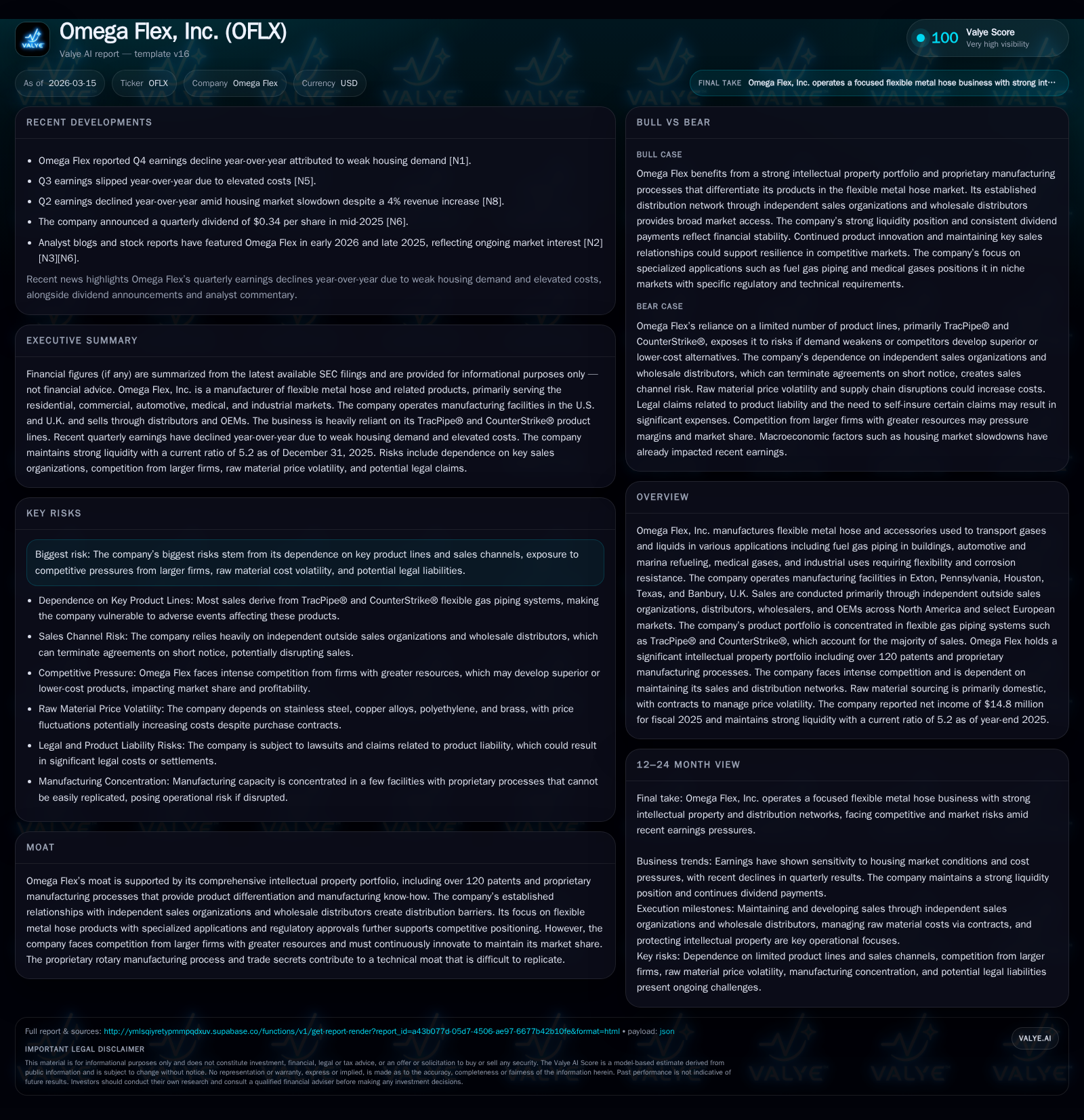

Omega Flex, Inc. operates with a strong moat underpinned by an extensive intellectual property portfolio exceeding 120 patents and proprietary rotary manufacturing processes for flexible metal hose products. Despite a 7.1% revenue increase in FY2025, operating and net income declined by over 17%, reflecting margin compression amid weakening housing demand and concentrated reliance on its TracPipe® and CounterStrike® product lines. The company maintains robust liquidity and funds consistent dividends but faces risks including raw material cost volatility, distribution network dependencies, and ongoing legal exposures. Forward growth hinges on innovation within core product offerings and monitoring end-market housing recovery.

Historical Performance and Revenue Drivers

Omega Flex’s financial trajectory through FY2025 illustrates steady revenue growth juxtaposed with compressing profitability margins. Revenue increased by 7.1% year-over-year to $27.4 million in FY2025 [F1], signaling sustained demand despite broader macroeconomic headwinds in end markets such as residential construction. However, operating income declined from $21.6 million to $16.9 million (-21.5% YoY), paralleled by net income slipping approximately 17.7% to $14.8 million [F1]. This divergence points toward margin pressures likely incurred due to increased raw material costs or heightened competitive pricing dynamics.

Operating cash flow also receded by nearly 17.7% to around $17.2 million in FY2025 [F1], though it remains sufficient to cover capital expenditures which slightly declined by about 9.2% year-over-year to roughly $1.8 million [F1]. The company’s investment level reflects measured reinvestment aligned with stable manufacturing operations primarily focused on flexible metal hose production.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 15 | 17 | 17 | 2 | -17.7% |

| 2024 | 18 | 21 | 22 | 2 | -13.2% |

| 2023 | 21 | 23 | 26 | 2 | -12.1% |

| 2022 | 24 | 15 | 31 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 14 | 15 | 17.6 |

| 2024 | 14 | 19 | 21.7 |

| 2023 | 13 | 22 | 26.4 |

| 2022 | 9 | 14 | 33.3 |

Source: SEC companyfacts cache [F1].

Note: Operating income figures for years prior to 2024 are incomplete.

Market Challenges and Product Line Concentration Risks

Omega Flex derives the majority of its revenue from a narrow product set dominated by its proprietary TracPipe® and CounterStrike® flexible gas piping systems including AutoFlare® fittings integral to their system architecture [S1]. This concentration exposes the company to channel risks exacerbated by recent softness in U.S housing markets [N1]. Sales are primarily routed through independent outside sales organizations and wholesale distributors who stock product warehouses for resale; any disruption or shift in distributor preferences could swiftly impact top-line results [S27]. Management has acknowledged vulnerability inherent in dependence on third-party distributors who may elect to carry competitors’ products instead [S1].

Competitive Moat: Intellectual Property and Manufacturing Secrets

Omega Flex sustains its moat with an expansive intellectual property portfolio encompassing over 120 patents worldwide covering product designs and innovative processes such as its proprietary rotary manufacturing method for flexible metal hoses [S1]. This trade-secret manufacturing know-how affords protection from direct replication as well as operational efficiencies supporting competitive differentiation.

The company also holds trademarks including OmegaFlex®, MediTrac®, DoubleTrac®, among others, further solidifying brand recognition alongside regulatory approvals that serve as barriers given stringent safety standards for fuel gas piping installations [S1].

Future Growth Catalysts and Industry Constraints

Growth constraints are tied principally to cyclical weakness in residential construction dampening demand for flexible gas piping products like TracPipe® [N1; S1]. Pending patent applications seek enhancements around CounterStrike® and MediTrac® lines but no explicit near-term volume guidance was provided; investors should monitor housing starts data as a proxy for demand recovery potential.

Raw material commodity volatility—particularly stainless steel and copper—remains an ongoing headwind amid global trade tariffs impacting input costs [S15]. Distributor channel attrition risk continues given wholesalers’ influence over downstream market penetration [S27], while competition is intensified by larger firms with broader resource pools enabling aggressive pricing or R&D investments [S15].

Capital Allocation Strategy: Dividends, Buybacks, and Cash Flow

Omega Flex demonstrates consistent capital return discipline, paying dividends totaling approximately $13.7 million in FY2025 supported by operating cash flow generation of about $17.2 million annually [F1; S2]. This payout reflects a robust dividend coverage ratio underscored by stable free cash flow after CAPEX investments roughly at $15 million annually—indicating prudent reinvestment relative to cash generation.

There have been no recent significant share repurchases; the last reported buybacks occurred several years ago at modest levels well below dividend outlays [F1], signaling management's prioritization of steady dividends over aggressive buybacks.

Financial Health: Liquidity and Debt Overview

As of December 31, 2025, Omega Flex maintained ample liquidity with cash and equivalents exceeding $53 million against current liabilities around $16 million—yielding a strong current ratio of approximately 5.2x indicating conservative short-term balance sheet management [F1]. The company holds no outstanding borrowings on an unsecured revolving credit facility capped at $15 million expiring mid-2028, providing financial flexibility without leverage burden [S4; S6].

Committed operating leases span key facilities including Exton PA headquarters, Houston TX manufacturing site, plus Banbury UK operations with payments moderately structured over multiple years providing predictable occupancy costs [S6; S25; S28].

Key Milestones to Track in Coming Quarters

Investors should monitor developments around patent applications related to CounterStrike® system improvements potentially offering incremental product differentiation advantages [S1]. Quarterly earnings releases will serve as barometers for demand shifts tied closely to housing market performance—the principal variable given recent Q4 earnings showed decline largely due to weaker residential construction activity [N1; S3].

Changes or renewals in distributor agreements merit attention given their outsized contribution via wholesale stocking distributors susceptible to competitor incursions or consolidation effects [S27].

Risk Factors Including Raw Material Costs and Legal Exposure

Raw material price volatility involving stainless steel, copper prices alongside polyethylene tariff uncertainties presents ongoing cost risks impacting margins despite efforts toward cost pass-throughs where feasible [S1; S15]. Concentrated revenue reliance on key product lines amplifies susceptibility if regulatory or competitive disruptions occur within these segments.

Legal exposures center on litigation concerning claims primarily related to alleged lightning or electrical damage linked to the company's flexible gas piping products—claims vigorously defended but incurring ongoing defense costs with aggregate exposure capped under commercial liability policies mostly ranging from $250K up to $3 million per claim with some self-insurance on claims post-September 2025 [S7; S10; S11; S18; S22]. These contingencies require active management attention given potential episodic impacts on earnings volatility.

Intellectual property infringement risks remain pertinent given the strategic importance of multiple patents and trade secrets defending core technology against larger rivals seeking market share through alternative designs or processes [S11].

This report synthesizes publicly available information from SEC filings, earnings releases, recent news articles, and structured financial data without making any investment recommendations or price projections regarding Omega Flex, Inc.. It aims solely to provide an informed perspective grounded in documented company disclosures as of March 15, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments