ChoiceOne Financial Services' Revenue Surge Tests Balance Between Growth and Risk

The Michigan-focused regional bank reports notable top-line expansion alongside concentrated real estate lending risks and capital redeployment activity.

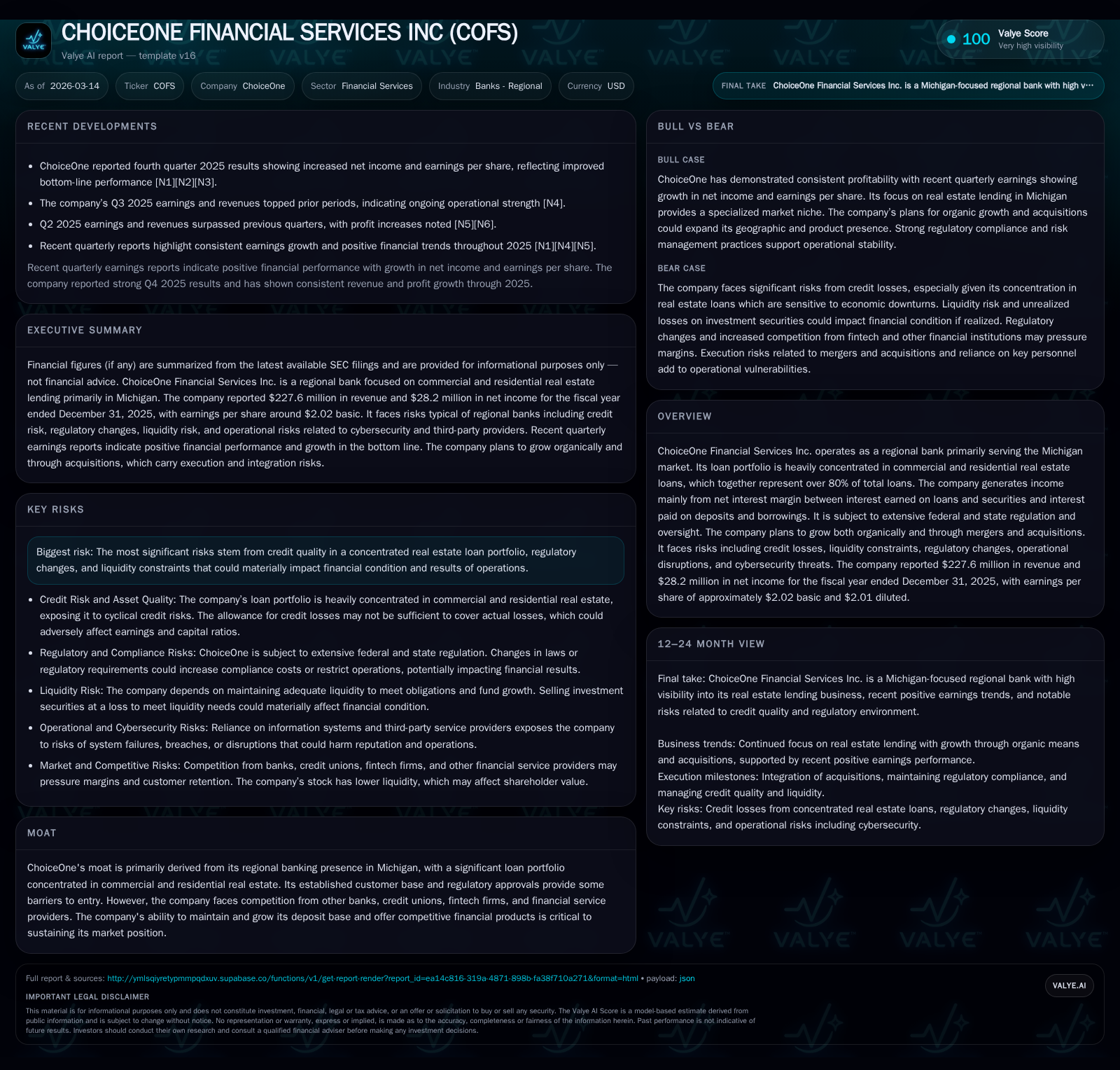

ChoiceOne Financial Services Inc. demonstrated a striking revenue increase of 63.6% in fiscal year 2025, reaching $227.6 million, primarily driven by the expansion of its commercial and residential real estate loan portfolio. However, net income growth was modest at 5.4%, reflecting margin pressure and rising expenses amid increased capital expenditures. The company’s concentrated exposure to Michigan real estate loans poses notable credit risk amid economic uncertainties, while management pursues both organic growth and acquisitions that introduce execution risk. Despite robust dividend increases and initial share buybacks, liquidity is challenged by substantial unrealized investment losses and contracting operating cash flow. Regulatory complexity, cybersecurity threats, and environmental liabilities linked to foreclosed properties remain key operational risks.

Strong Revenue Growth Backed by Expanding Loan Portfolio

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 228 | 28 | 32 | 7 | +63.6% | +5.4% |

| 2024 | 139 | 27 | 49 | 2 | +25.7% | |

| 2023 | 21 | 46 | 4 | -10.1% | ||

| 2022 | 24 | 45 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 17 | 3 | 25 |

| 2024 | 9 | 0 | 47 |

| 2023 | 8 | 0 | 42 |

| 2022 | 8 | 1 | 44 |

Source: SEC companyfacts cache [F1].

ChoiceOne Financial Services manifested a robust revenue leap in fiscal 2025, totaling approximately $227.6 million—an impressive year-over-year increase of 63.6% from $139.1 million in the prior year [F1]. This surge materially outpaced net income growth which rose only 5.4% to $28.2 million, suggesting compressing margins or rising expense components despite volume gains [F1]. Operating cash flow presented a contraction of 34.6% year-on-year to $31.8 million, highlighting working capital or earnings quality concerns notwithstanding top-line momentum [F1]. Capital expenditures expanded sharply by nearly threefold to $6.6 million, indicative of strategic reinvestment aimed at sustaining medium-term growth [F1]. This financial trajectory underscores management’s successful augmentation of its loan book as a core revenue driver.

Key Drivers Behind the FY2025 Financial Performance

The core driver remains the loan portfolio concentration with over 80% invested across commercial and residential real estate segments primarily within Michigan [S1][S6]. Commercial and construction real estate loans alone amount to approximately $1.8 billion representing nearly 60% of loans outstanding, complemented by approximately $728 million in residential loans [S13][F1]. This segmentation underpins net interest margin generation but also concentrates credit risk [S1][N3]. Despite strong revenue rises, regulatory cost pressures and allowances for credit losses have heightened expense lines curtailing net income expansion [S1][S8]. The company balances interest rate volatility impacts on asset yields against deposit funding costs under an environment shaped by Federal Reserve monetary policies [S7][S16].

Portfolio Concentration and Credit Risk in Michigan's Real Estate Market

The pronounced geographic focus on Michigan coupled with heavy reliance on real estate-secured lending exacerbates vulnerability to localized economic downturns [S13][S20]. Collateral values face downside risk from macroeconomic factors including interest rate fluctuations, inflationary pressures, trade uncertainties, and sector-specific dynamics [S1][S20]. The Company acknowledges that its allowance for credit losses might understate actual future loan impairments if borrower defaults spike or property values decline [S8][S14]. Furthermore, regulatory oversight periodically demands revisions to loss reserves that could negatively affect capitalization and earnings [S8]. In particular, commercial real estate exposures entail higher financial risk owing to larger loan size concentrations and cyclical market sensitivities [S13]. Environmental hazard liabilities associated with foreclosed properties add a unique layer of potential loss that could surpass property valuations [S5].

Growth Strategy Through Organic Expansion and M&A Ambitions

ChoiceOne intends to grow through both organic customer acquisition/deposit base expansion and selective mergers & acquisitions targeting complementary financial institutions within its core markets [S1][S6][S8]. While M&A offers geographic footprint enhancement and product diversification potential, it is acknowledged that these deals require significant capital deployment—potentially dilutive common stock issuances or debt instruments—and carry integration execution risk that could disrupt operational focus or strain resources [S6][S8]. Success depends heavily on expanding the deposit base efficiently to balance funding needs while realizing expected cost savings or revenue synergies post-transaction.

Liquidity Position and Capital Structure Amid Market Volatility

Liquidity remains challenged as ChoiceOne reported $90.4 million in unrealized losses within its investment securities portfolio at fiscal year-end—including $52.8 million classified as available-for-sale—which may restrain asset sales without crystallizing impairments detrimental to equity and net income levels [S7][S14][F1]. Operating cash flow reduction despite surging revenues further signals growing working capital demands or collection timing shifts possibly linked to loan book composition changes [F1]. Deposits constitute the principal liquidity source alongside interest receipts; however, market conditions could complicate timely access if pressure intensifies across financial institutions broadly (systemic risk) [S7][S13]. The capital adequacy ratios remain closely monitored due to potential impacts from increasing credit allowances or realized losses.

Capital Allocation: Dividends, Buybacks, and Investment Trends

In capital returns activity, ChoiceOne markedly increased dividends paid to shareholders by almost doubling from $9.0 million in FY2024 to $16.9 million in FY2025 reflecting confidence in earnings sustainability despite external pressures [F1][S19][S23]. Notably, the company initiated share repurchases totaling $2.67 million—the first buyback activity seen since two years ago—indicating renewed emphasis on shareholder value amidst improved free cash flow estimated at approximately $25.2 million (operating cash flow minus capex) [F1]. Concurrently, capex rose sharply (+288%) evidencing strategic reinvestments likely focused on technology upgrades or branch expansion critical for competitive positioning.

Risks Lurking in Regulatory Environment and Economic Conditions

The bank operates within an extensively regulated framework governed by federal/state regulators including the Federal Reserve Board, FDIC, and state authorities—the stringency of which can introduce cost burdens and tight operational constraints especially if new regulations impact capital requirements or procedural compliance across deposit-taking activities [S4][S12][S16]. Environmental risks emanate from ownership of foreclosed commercial real estate potentially containing hazardous substances resulting in costly remediation obligations beyond collateral values identified during recovery processes [S5]. Further vulnerability arises from cybersecurity threats targeting sensitive customer data—with failure here exposing the firm to reputational damage and costly litigation—and operational dependency on third-party service providers escalates risk of business interruption or suboptimal service delivery outcomes [S11][S17][S18]. Additionally, employee misconduct or inaccuracies in borrower financial disclosures present latent perils affecting loan asset quality assessments.

Outlook: Milestones to Monitor as Growth Meets Prudence

Stakeholders should closely track quarter-to-quarter earnings consistency following the Q4 earnings beat as reported early 2026 which validated recent performance improvements but also shed light on ongoing margin management challenges [N1][N2][N3]. Progress updates on any active acquisition discussions will be critical given their inherent execution risk combined with material capital requirements noted in filings [S23]. Evolution of allowance for credit losses bears attention as this will signal management’s view on emerging asset quality trends particularly within Michigan’s real estate market context [N2][S8]. Deposit base trajectories remain essential indicators of sustainable funding breadth required to underpin both organic growth ambitions as well as M&A financing capabilities.

This analysis is based solely on publicly available financial data and regulatory filings through March 2026 provided by ChoiceOne Financial Services Inc., supplemented by recent news releases reflecting its corporate disclosures. It does not constitute investment advice or recommendations but serves as an informational resource regarding company performance metrics, strategic posture, risks exposure, and prospective developments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments